With stock market soaring high, fund houses leave no stone unturned in mobilising money from the investors. They keep pouring in new funds during these bull phases and the style of these NFOs depends upon the prevailing industry regulations. Here is a brief account of different impetus that new fund offers have seen over the last 15 years and how that led Securities and Exchange Board of India (SEBI) to implement new rules in investors' interest. We also bust some myths that investors have regarding NFOs.

The journey of new fund offers (NFOs)

There were some industry practices in the past that gave fund houses the convenience to collect more and more money. Earlier, mutual fund investors had to pay a 2-2.5 per cent entry load (fee while entering a scheme) if they used the services of an advisor/distributor. So, they were made to buy and sell frequently, which would directly reduce their return and cripple their long-term investing goals. Thus, SEBI scrapped entry loads in August 2009.

For a very long time, distributors used to get two types of commissions - upfront and trail. Upfront commission, typically ranging between 1 and 1.75 per cent was paid at the time of garnering money from investors, while trail commission of about 50 basis points was paid every year for as long as the investor stayed invested. This pushed a lot of closed-end equity schemes into the market where investors have to stay invested till maturity because that allowed fund houses to bunch later-year commissions at the very start itself, making them pay 4-6 per cent upfront commission to the distributors. It was the AMCs that paid these high commissions from their own pockets with the recovery being made from expense ratio charged from unitholders. This was a double whammy for investors. Firstly, a closed-end equity scheme was not a suitable product for them and secondly a lot of their money was lost in distributor's commissions. To curb all such malpractices, SEBI abolished upfronting of commissions in September 2018 and introduced revised capping for the total expense ratio basis the scheme type and AUM of the fund.

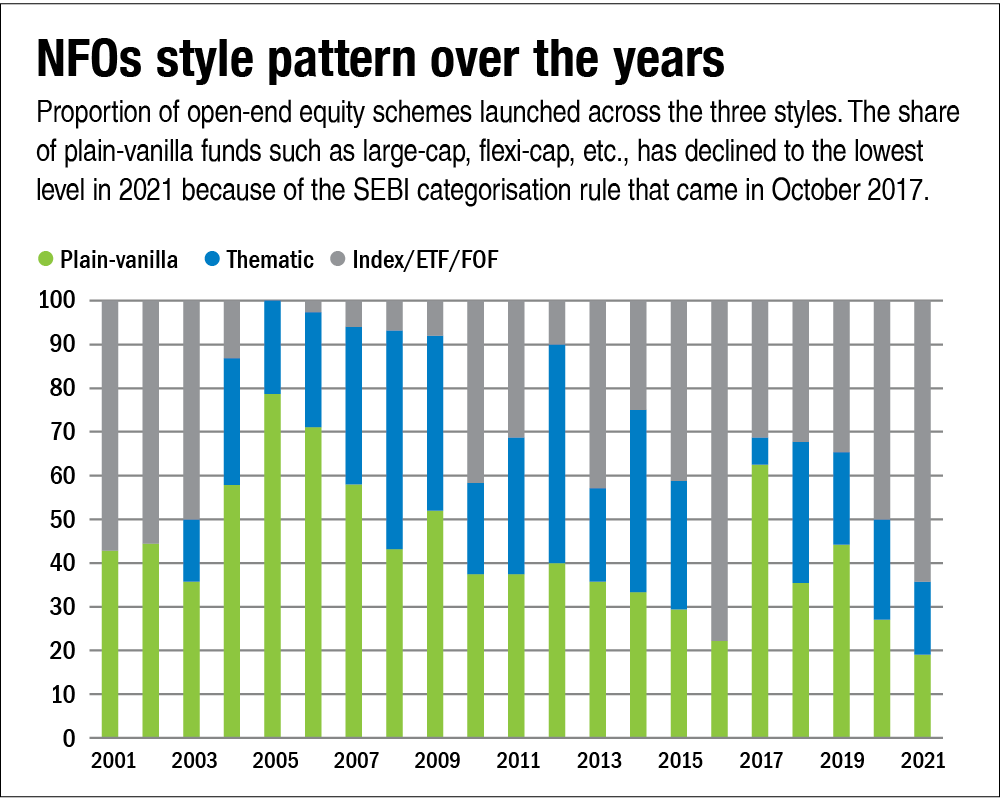

Another route adopted by AMCs to keep the inflows going was by launching more and more funds that were alike. There was such a deluge of similar fund options at the disposal of investors which did nothing but confused them. As a result, in October 2017, the regulator asked AMCs to demark all their schemes in 36 specified categories and restricted them to have only one scheme in each category except for index funds, exchange-traded funds (ETFs), fund of funds (FOFs) and sectoral/thematic funds. Now you can understand why niche-style or thematic funds are overflowing in the market lately. This makes NFOs even more superfluous to merit entry in a common investor's portfolio as most of these ideas are new, with their own inherent risks.

Breaking NFO misconceptions

NFO ≠ IPO: During the bull run and the IPO season, some people misinterpret NFOs as an opportunity to make quick gains, as in the case of an IPO. In the case of an IPO, there is a possibility of making profit because the issue price (the price you pay) can be different from the listing price of that stock. This is a demand-supply function. However, in an NFO, there is no concept of listing so to say. You pay Rs 10/unit and that's it. Now you will make a gain only when the underlying portfolio performs well, just like any existing fund.

NFO NAV is not a cheap NAV: While this misconception was more prevalent in the past, still some investors are under the misconception that investing in an NFO as compared to any other existing fund is cheaper just because NFO comes with a NAV of Rs 10, while the NAV of old funds is higher. It is completely wrong to judge a fund by its NAV. You earn returns when portfolio securities do well and a new fund has no advantage whatsoever in bringing about that outperformance because of its low NAV. The NAV is just used to calculate your return.

Also in this series:

NFO mania is back: Old vs new funds

NFO mania is back: Why new funds lag behind

Ask Value Research ![]()