SECTOR VIEW

The pre-pandemic situation

The Indian hospitality sector had been sailing smoothly before the pandemic came and spoiled the show. For the hotel sector, 2019 was a record year and 2020 was expected to be 'even bigger' in view of a sharp increase in domestic travel. According to the global research firm Mobility Foresights, the Indian hotel industry was growing at a decent rate of 4 per cent between 2015-2019 and the demand from domestic travellers remained a bright spot. Likewise, the Indian restaurant industry with an employee base of over seven million people was growing at a rapid pace on the back of the rising demand for eating outside, a higher disposable income, increasing urbanisation and the expansion of food-delivery services.

During the pandemic

Initiatives like lockdowns, social distancing, the stay-at-home order and restrictions on travel and mobility were undertaken to flatten the COVID-19 curve. Almost all the restaurants were asked to limit their operations only to the takeaway. Usually, operational costs of most hotels are fixed and quite high. During the pandemic, hotels had to bear these costs, along with other expenses, which led to a lot of cash burn. With restrictions in place and around 90 per cent fall in their revenues, the hospitality sector was one of the worst-hit sectors.

Although the start of 2021 had brought the hope of recovery for these players, the deadly second wave soon hit, affecting most of the Indian states profoundly. This placed the industry on the back foot again.

The present situation

With the pace of COVID infection slowing down and the vaccination drive gaining pace, companies in this sector have started witnessing a slow recovery. Domestic leisure and wedding businesses earn a big chunk of revenues for hotels but the demand from these segments has been muted because of the pandemic, thereby impacting the business.

As reported by the Federation of Hotel & Restaurant Associations of India (FHRAI), the Indian hotel industry took a hit of over `1.3 lakh crore in revenues for the fiscal year 2020-21 due to the pandemic. Businesses with high debt levels have been struggling to repay loans along with interest costs.

On the other hand, restaurants have been witnessing a faster recovery because of their home-delivery system. As most people have been staying at home and eating out less because of the fear of the infection, they have started ordering at home, thereby enabling restaurants to regain business as compared to their hotel counterparts.

STOCK VIEW: IRCTC

A central public-sector enterprise, the company operates four business segments - internet ticketing (27 per cent of FY20 revenue), catering (46 per cent), packaged drinking water (10 per cent) and travel and tourism (17 per cent).

The competitive edge

It is a pure-play monopoly business in three out of its four operating segments, namely internet ticketing, packaged drinking water and catering. It is the only authorised entity to manage catering services in trains and major static units at railway stations. At present, the catering segment - the major contributor to the company's revenues - is bearing the brunt of pandemic-related restrictions. However, as we move towards normalcy, this segment is likely to start gaining pace.

Also, it is the only authorised entity to manufacture and distribute packaged drinking water under the brand name 'Rail Neer' available at all railway stations and trains.

The company offers ticket-booking services through its website and mobile app and more than 30 crore tickets were booked in FY20. With the vaccination drive gaining pace and easing of lockdown-related restrictions, the number of railway passengers is likely to increase. On the other hand, with the resumption of daily activities, the hotel industry is also poised to recover. Amid all, the monopoly position of IRCTC in many of the segments makes it a good investment option.

Financials & valuations

As of March 2021, the company had a strong balance sheet with zero debt and cash and cash equivalents of more than `1,450 crore. Its stock trades at a very high P/E of 191 times, which is due to the loss of revenues in FY21 - which fell by more than 65 per cent. However, it managed to deliver an ROE of 13.5 per cent. Given the monopoly position of its businesses, the company is expected to bounce back sharply. Although the stock may appear to be overvalued at a P/B of 24.7 times, investors should keep this stock on their radar. As the demand for online ticketing is expected to increase in the future, the company will continue to earn a high operating-profit margin, which grew to 35.2 per cent in FY21 from 34.7 per cent in FY20. In the last one year, the stock has delivered a return of 67 per cent as against the Sensex which rose by more than 45 per cent.

ABOUT THE CHART AND THE TABLE

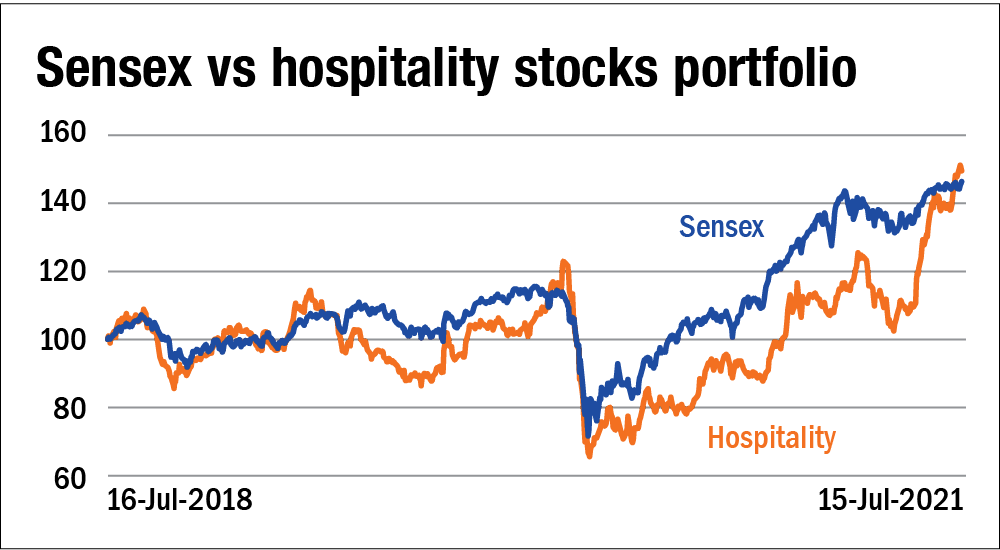

Sensex vs sector stocks portfolio

In the analysis above, we have given a three-year chart of the portfolio comprising the top stocks in the sector vis-à-vis the Sensex. This chart will help you assess the movement in the sector as compared to the market. The stocks considered for this chart are the ones given in the table of key stocks. It was assumed that one invested an equal amount in each stock three years ago. If a company was not listed three years ago, it was incorporated in the portfolio from its listing and the appropriate adjustment was made.

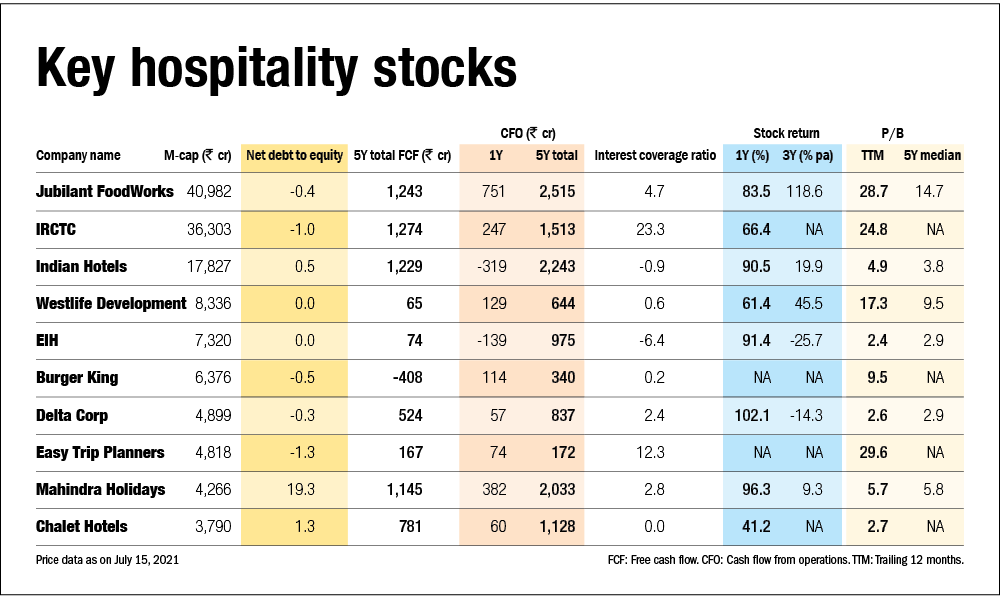

Key sector stocks

This table mentions the top stocks in the sector, along with their key financial stability numbers. Given that most companies in the sectors discussed have witnessed a significant drop in their profits, profitability related metrics may not be very useful. One must assess their balance-sheet and cash-flow strength. Following are the key columns in this table:

Net debt-to-equity: This is the debt to-equity ratio adjusted for cash and current investments. A negative ratio indicates more cash/current investments than debt. This is a comfortable position to be in.

Free cash flows: Cash flows from operations minus capital expenditure is free cash flows. They indicate that a company is able to incur capital expenditure from its own cash flows rather than depend on outside funding. This is highly desirable.

Cash flows from operations: This is cash generated from a company's operational activities. A positive value is desirable. A negative value indicates that profits, if any, are not getting converted into real cash, an undesirable scenario.

Interest-coverage ratio: It indicates how easily a company can service the interest on its debt. The higher the number, the better.

Also in this series:

Profiting from recovery: Aviation

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()