Incorporated in 2002, Shyam Metalics and Energy is a metal-producing company that focuses on long-steel products and ferroalloys. The company is one of the largest producers of ferro alloys and the fourth-largest name in the sponge iron industry with regard to the installed capacity. Since the commencement of its operations, the company has been delivering operating profits every year.

Currently, the company has three manufacturing plants with a total installed capacity of 5.7 million tonnes per annum (MTPA), along with captive power plants with an installed capacity of 227 MW as of December 2020. Now, the company plans to expand its capacity to 11.6 MTPA and 357 MW by FY2025.

The company has a diversified product mix, including long-steel products such as iron pellets, sponge iron, steel billets, TMT, wire rods and ferroalloy products. Two of its manufacturing plants work as 'ore to metal,' which operates across the value chain of steel manufacturing and it helps the company maintain margins and insulate it from price volatility. The company sells its products across 13 states and 1 union territory through 42 distributors (as of December 2020).

Strengths

- Its plants are located near to rich mineral belts of India, which provide close proximity to raw-material sources. It ultimately helps in reducing transportation costs and increasing operational efficiencies.

- The company utilises its waste materials or by-products, such as pollution ducts, waste heat and solid waste, as the raw materials for its captive power plants. The company generates almost 90 per cent of its power consumption through these plants at an average rate of Rs 2.24 per kwh, while Rs 5-7 is charged for the grid power.

- As one of the few companies in India, the company has captive railway sidings. It helps in the reduction of freight costs and turnaround time when it comes to the transportation of raw materials to plants and finished products to customers.

- The company has a diversified product mix, along with the forward and backward integration of its manufacturing plants. It provides the company with the flexibility to sell intermediate products, as well as use them for captive consumption.

- As compared to other steelmakers, the company has better financial strength in terms of debt-to-equity, which is one of the least in the industry.

Risks/concerns

- The prices of steel are volatile and very sensitive to the cyclical nature of industries it serves. The demand for steel is dependent on industries such as real estate, automobiles and infrastructure. Thus, a decrease in the demand from these industries could have adverse effects on steel prices, thereby leading to lower revenue and margins for the company.

- There are certain criminal proceedings against the promoters and directors of the company and they are released on bail.

IPO questions

Company/business

1. Are the company's earnings before tax more than Rs 50 cr in the last twelve months?

Yes, in the trailing twelve months, the company reported earnings before tax of Rs 580 crore as on December 30, 2020.

2. Will the company be able to scale up its business?

Yes, an increased focus on infrastructure spending by the government and the rising demand growth for long steel and ferro alloys will allow the company to expand its business. Also, the company is already working towards its expansion plans. Further, it is planning to set up a blast furnace for the production of DI pipes.

3. Does the company have recognisable brand/s, truly valued by its customers?

Yes, the company sells its products under the brand 'SEL' and caters to large domestic customers, such as Jindal Stainless Steels, Jindal Stainless Steel (Hisar) and Rimjhim Ispat.

4. Does the company have high repeat customer usage?

Yes, the top 10 customers of the company accounted for 22.3 per cent of the total revenues in FY20. Although the company does receive repeat orders from its customers, it does not enter into long-term contracts with them.

5. Does the company have a credible moat?

No, the company faces high competition from both domestic and international steel producers.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No, the company has to comply with various industry-specific and environmental laws and regulations.

7. Is the business of the company immune from easy replication by new players?

Yes, metal production is a highly capital-intensive business, which may act as an entry barrier for new players.

8. Is the company's product able to withstand being easily substituted or outdated?

No, the company is engaged in steel products and ferroalloys which can't be differentiated. Thus, its products cannot withstand being substituted.

9. Are the customers of the company devoid of significant bargaining power?

No, the company's top 10 customers account for 22.3 per cent of its revenue. Such high reliance on a select group of customers can constrain its ability to negotiate its arrangements with them.

10. Are the suppliers of the company devoid of significant bargaining power?

No. The company will have to pay liquidated damages if it fails to buy a specified quantity of some of its raw materials.

11. Is the level of competition the company faces relatively low?

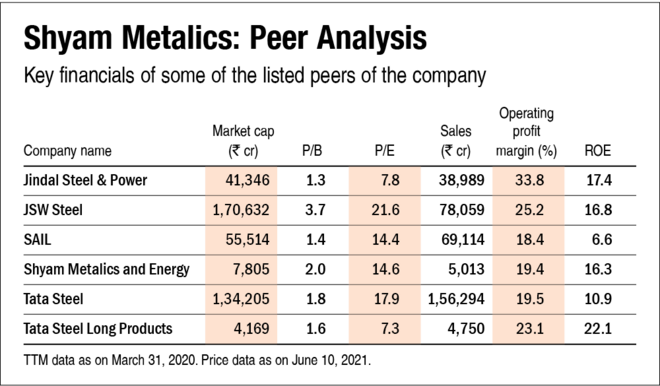

No, the company operates in a highly competitive industry and faces stiff competition from large-steel producers like Jindal Steel and Power, Tata Steel, SAIL and JSW Steel.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes, one of the founders and managing directors of the company Mr Brij Bhushan Agarwal will hold a 9.1 per cent stake in the company post the IPO.

13. Do the top three managers have more than 15 years of combined leadership at the company?

Yes, the chief financial officer of the company Mr Shree Kumar Dujari has been associated with the company since 2006.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with Sebi guidelines?

Yes, we have no reasons to believe otherwise.

15. Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

No, there are certain criminal proceedings against the promoters of the company.

16. Is the company's accounting policy stable?

Yes, we have no reasons to believe otherwise.

17. Is the company free of promoter pledging of its shares?

Yes, the promoter's stake is free of any pledging.

Financial

18. Did the company generate the current and three-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

Yes, the three-year average ROE and ROCE stood at 24.9 per cent and 21.6 per cent, respectively.

19. Was the company's operating cash flow positive during the previous year and the last three years?

Yes, the cash flow from operating activities has been positive in the last three years.

20. Did the company increase its revenue by 10 per cent CAGR in the last three years?

Yes, the company's revenue grew at a rate of 21.9 per cent in the last three years.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest-coverage ratio more than 2?

Yes, the company's interest-coverage ratio stood 8.1 times as of December 2020.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

No, metal production is a capital-intensive business and requires high working capital. Also, the cash-conversion cycle stood at 74.8 days which is also high.

23. Can the company run its business without relying on external funding in the next three years?

Yes, the company has been generating positive cash flows and has cash and cash equivalents of more than Rs 275 crore, which will reduce its dependence on external funding. Moreover, the company will be repaying a part of its debt which will further reduce interest cost and increase profitability.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

No, the company's short-term borrowings have increased from Rs 278.6 crore in FY18 to Rs 682.3 crore as of December 2020.

25. Is the company free from meaningful contingent liabilities?

No, the company reported contingent liabilities to a tune of Rs 304.2 crore as of December 2020.

The stock/valuation

26. Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

Yes, the company's stock will offer an operating yield of approx 8 per cent as of December 2020.

27. Is the stock's price-to-earnings less than its peers' median level?

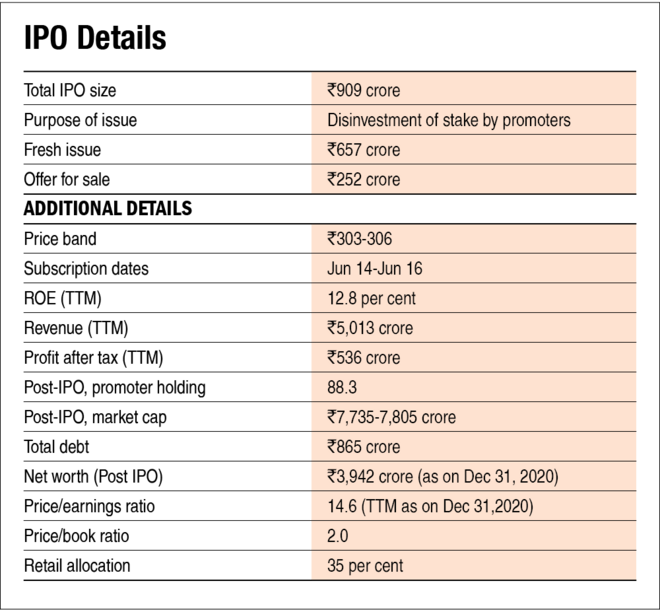

No, the company's stock would trade at a slightly higher P/E of 14.6 as compared to its peer's median level of 14.4.

28. Is the stock's price-to-book value less than its peers' average level?

No, based on equity post the IPO, the stock would trade at a P/B of around 2, which is higher than its peers median of 1.6.

Disclaimer: The author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()