Shivam is planning to buy a house and the one he likes is exceeding his budget by a few lakhs. He does not want to compromise on the house, as it's a lifetime purchase but he does not have the funds to meet the deficit. Shivam has some investments in the National Pension System (NPS) Tier I account and is now wondering whether he could somehow use that. After all, it is his money.

Being a pension scheme, the NPS Tier I account matures only when the subscriber reaches the age of 60. Even at that time, 60 per cent of the corpus can be withdrawn as a tax-free lump sum, while the remaining 40 per cent has to be utilised to buy an annuity plan unless the value of the total corpus does not exceed Rs 5 lakh. Although the subscriber has the option to defer the maturity till he reaches the age of 75, he cannot redeem all his money before 60. If he chooses to close the account prematurely, at least 80 per cent of the corpus has to be utilised to buy an annuity plan. Complete corpus can be withdrawn as a lumpsum on premature exit only if the corpus does not exceed Rs 2.5 lakh. Given that, Shivam is left with the only option of making a partial withdrawal.

Conditions to fulfil for a partial withdrawal

Although the NPS Tier I account allows a partial withdrawal before the subscriber reaches the age of 60, there are some conditions attached to it, as listed below:

- The subscriber must have completed at least three years.

- Partial withdrawals can be made only three times during the entire tenure.

- The money should be utilised only for any of the following purposes:

- Higher education or marriage of children

- Purchase or construction of a residential house. However, the subscriber should not have any other house in his name.

- Expenses related to skill development/re-skilling or any other self-development activities

- Establishment of own venture or start-up

- Medical and incidental expenses arising out of the disability or incapacitation suffered by the subscriber

- Treatment of self, spouse, children or dependent parents in the case of any of the following specified illnesses: cancer, kidney failure, primary pulmonary arterial hypertension, multiple sclerosis, major organ transplant, coronary artery bypass graft, aorta graft surgery, heart valve surgery, stroke, myocardial infarction, coma, total blindness, COVID-19, paralysis and any serious or life-threatening accident

- There should be a gap of at least five years between any two partial withdrawals. This condition is removed if the money is required for any medical emergency.

- The subscriber cannot withdraw more than 25 per cent of the contributions made by him.

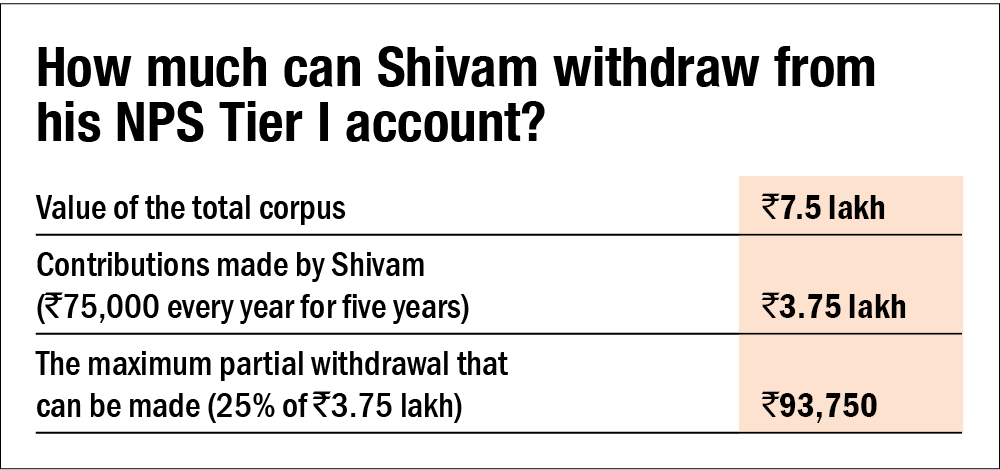

The last condition, which limits the withdrawal amount to 25 per cent of the self-made contributions, is often misunderstood by many. Investors usually think that they can withdraw up to 25 per cent of the total investment value or the corpus that is in their NPS Tier I account. But that is not true. The NPS account usually receives contributions from both the employee and the employer, barring the situation where an account has been opened under the 'All Citizen' model. As per the rules, you are allowed to withdraw only up to 25 per cent of the contributions made by you and not of the total corpus. Let us discuss it with an example. Suppose Shivam has an accumulated balance of Rs 7.5 lakh in his NPS account. Out of this, the contributions made by him is Rs 3.75 lakh, with an investment of Rs 75,000 per year made for the last five years. Then, he can withdraw only up to Rs 93,750 (25 per cent of 3.75 lakh). Money received on partial withdrawals is exempt from taxes.

The process to make a partial withdrawal

Earlier, the partial-withdrawal request was approved by the nodal officer following the verification of all supporting documents as the evidence of the mentioned purpose. However, in a bid to reduce the turnaround time and to make the procedure more agile, partial withdrawals can now be made only through self-declaration without any supporting document. The process is completely online. Here are the broad steps:

- Log in to the CRA website (NSDL or Karvy) by using the login credentials for your NPS Tier I account.

- Go to 'Transact' and select 'Partial withdrawal'.

- Select the amount and reason for the partial withdrawal.

- Furnish a self-declaration form mentioning that the money will be spent only for the declared reason.

- Verify your bank account and contact details.

- Authenticate by using the OTP sent to your mobile/email.

- The amount will hit your bank account on the fifth working day after you submit the online request.

Should you make a partial withdrawal?

Situations like the one faced by Shivam are quite common. In such situations, there is a strong urge to dip in your retirement savings. However, that should be a last resort and this fund should be used only in the case of an emergency. Retirement is a long phase, spanning about two to three decades, when our income stops but expenses and inflation continue. Unnecessarily using the money saved for retirement may help you fulfil your current dream but may push you towards a harder time during the golden years of your life. Even if Shivam or anyone else has to utilise the money saved for retirement for buying a house, the used amount needs to be re-filled as early as possible. However, one may still be on a losing front in terms of the compounding benefit that one would have otherwise reaped.

This article was originally published on November 05, 2021.

Ask Value Research ![]()