After learning about the basics of the P&L statement and the income and expenses part of it, readers may now think that all they need to do now is subtract expenses from the income in order to compute the profit or loss. While this is almost true, some more steps are required to calculate the real profit/loss of a business.

Tax expense

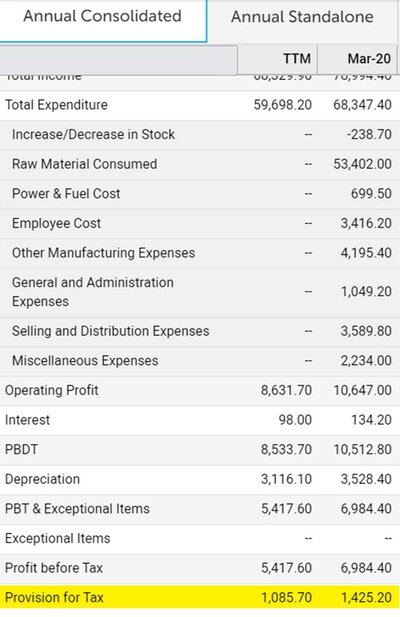

The Government of India levies income tax on the profit earned by every company. Therefore, when you subtract all expenses from the income, the figure you get is the profit before tax or PBT. Tax expenses are calculated based on the PBT and recorded in the P&L statement as the provision for tax. The real profit is what you get after the tax is deducted from the PBT. This figure is known as the profit after tax or PAT.

Investors must bear in mind that the provision for tax may not necessarily be the tax rate multiplied by the PBT. This is because there are many allowances and deductions from an income-tax point of view. Therefore, the amount of PBT is different and the tax payable varies too. Since this is an area where the management's inputs are required, investors should remember that the PAT declared in the P&L statement is also, to some extent, only an estimate and not the final figure.

Minority interest

Minority is another important aspect that investors should consider. However, this part comes only in a consolidated P&L (as opposed to a standalone P & L) where a company has subsidiaries and therefore, needs to prepare a single P & L, comprising the income and expenses of all its subsidiaries. According to accounting principles, the consolidated figure is calculated simply by adding all income and expenses. Let's look at a simplified version of the consolidated P&L of a hypothetical company (ABC Ltd), which has just one subsidiary (XYZ Ltd).

As stated in the above-mentioned table, the consolidated P&L is calculated by just taking the simple sum of the parent and subsidiary companies. However, when it comes to calculating this type of consolidated P&L, it is always presumed that the parent company owns 100 per cent of the subsidiary company.

Now a problem arises with this method when the parent company owns anything less than that. For example, if the parent company owns only 75 per cent of the subsidiary company in our above-mentioned consolidated table, then the parent company is entitled to only Rs 30, i.e., 75 per cent of Rs 40. Therefore, there would have to be an adjusting entry to decrease the profits by Rs 10 and this is precisely what the term 'minority interest' refers to.

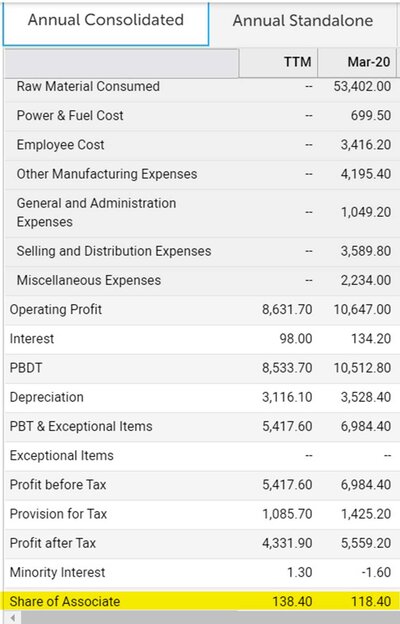

So, investors must always look at PAT after adjusting for the minority interest.

Share of associates

When a company has subsidiaries in which it has less than 50 per cent shareholding, then accounting principles do not require the company to create a consolidated P&L. Instead, the company can recognise a proportional share in its investee company's profits. It could be said that this entry is, in a way, the corollary of minority interest. For example, in the previous illustration, if ABC Ltd is the minority shareholder, holding 25 per cent in the subsidiary company (XYZ Ltd), then it would recognise a profit of Rs 10 in the P&L statement as its 'share of associate'.

Again, investors would do well to recognise that the net income as adjusted for its share of associate gives a more accurate picture of the company's overall profitability.

Earnings per share

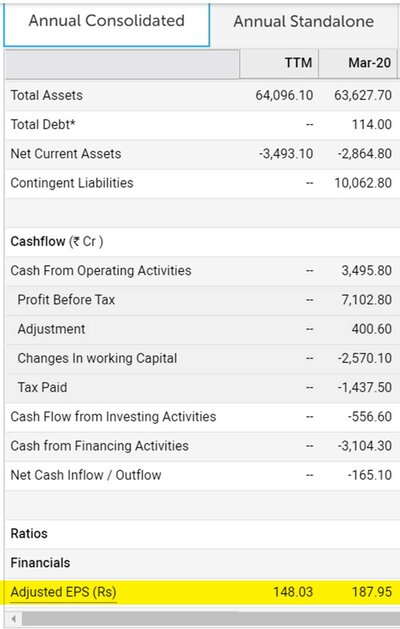

After making the above-mentioned adjustments, the final number is the consolidated PAT. This is the total amount of profit that is available to all shareholders. Although it is the primary factor that investors should take into consideration, it is equally important to consider earnings per share or EPS. It is calculated by dividing the total PAT by the total number of shares outstanding and is given on the website of Value Research under the head 'Adjusted EPS'.

While there is generally a perfect correlation between the consolidated PAT and the EPS, there are certain circumstances when these two numbers diverge. These happen when there is a significant change to the capital base of the company. A case in point is YES Bank Ltd. After a spell of poor performance, new shareholders infused a large chunk of capital at very nominal prices, thereby causing massive dilution for existing shareholders. This has led to a situation where even if the consolidated PAT of Yes Bank returns to its pre-stressed levels, the EPS will remain extremely depressed.

Also in this series:

Ask Value Research ![]()