After gaining a basic understanding of the P&L statement let us focus a bit more on the 'income' part. Here investors need to conduct a more in-depth review of the accounting principles in order to have a more nuanced view of this important entry and evaluate a company's financial performance.

Principle 1: Income ≠ cash

As explained in the first part of this series, income is calculated by using accrual-based accounting principles. This means that sale is recorded in the P&L statement on the basis of the timing of the transaction, regardless of when the cash is received. For many retail businesses, there is no difference in timing, as they receive cash from customers immediately at the time of sale. However, for many B2B businesses, there is a significant gap between the sale of a product/service and the receipt of the payment for the same because their customers don't always pay on time. Businesses, which supply to the government (such as defence, infrastructure construction, etc.) and those entities that are in a weak financial position (For example: airports providing services to cash-strapped airlines and gencoms supplying electricity to distressed discoms) are particularly affected by this. Although the P&L would reflect the total amount of sales, it wouldn't show how much of the stated income has actually been received.

Takeaway: Investors should not presume that all the income shown in the income statement has actually been received by the company.

Principle 2: Operating income is more important than other income

When investors look at the P&L of any company on www.valueresearchonline.com, the total income is classified into two types of entries - operating revenue and other income (the terms revenue and income can be used interchangeably). While the former reflects the core income from the company's primary business, the latter reflects the income from all other sources, which are not directly related to the company's business. For example, a car manufacturer may earn interest from FDs or dividends from shares in other companies. There could also be a scenario where other income is purely an accounting entry, which is based on management estimates (ex: revaluation of the fair value). Therefore, investors must focus on the core operating revenue because earning other income is not only unsustainable but also not the fundamental purpose of running the company.

Takeaway: Investors should pay more attention to operating income and should not get carried away by increases in other income.

Principle 3: Revenue recognition varies from industry to industry

When it comes to recognising long-term contracts, the complicated nature of accrual accounting makes it a bit more tricky. Companies usually follow either the percentage completion method or completed contracts method. In the former method, the quantum of income recognised will be dependent on the percentage of the work completed, while in the latter, income is only recognised when the contract is fully completed. For example, when a real-estate company constructs an apartment, investors must check what method of income recognition is being followed by the company. Companies, like Ashiana Housing, recognise income only when homes are delivered. So, it may seem like their revenues are more uneven and lumpy (as it is tied to the completion of their projects) as compared to other companies who recognise revenue as construction progresses. But it doesn't reflect the ground reality and is just a natural consequence of their accounting principles.

Takeaway: Investors must always be mindful of the differences in accounting while comparing two different companies.

Conclusion

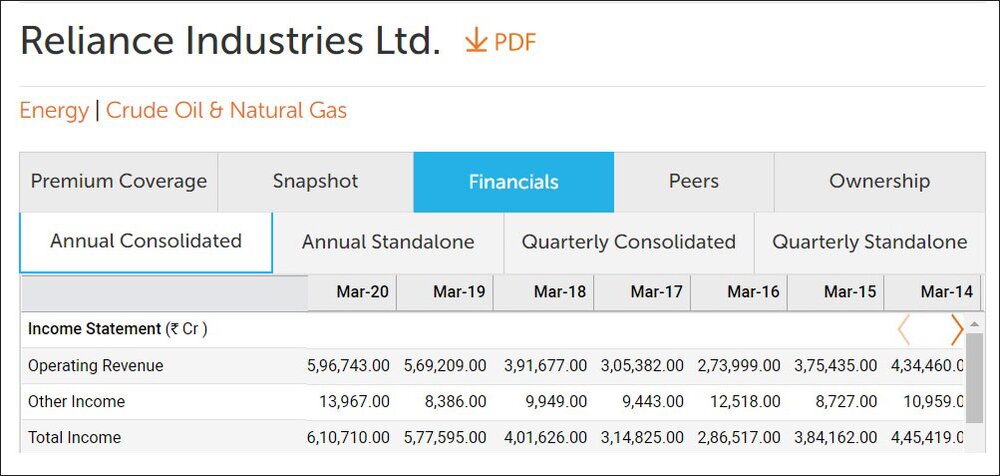

Figuring out the amount of money a company is earning is more complicated than it sounds. Therefore, investors need to rigorously examine every bit of the annual report and not just the financial statements before investing. And just as a reminder, investors can access the P&L of every listed company on www.valueresearchonline.com. Just type the name of the company in the search bar and you can access its page, which has the P&L under the 'Financials' tab. The following is a screenshot of the P&L of Reliance Industries and can be found here.

Also in this series:

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()