Nazara Technologies is a leading diversified gaming and sports-media platform company, having its presence in India and developed global markets, such as Africa and North America. The company provides services across various categories comprising:

- Gamified early learning (39.2 per cent of revenues for the six month period ending September 30, 2020): The company entered this space through the acquisition of Kiddopia, its flagship gamified early-learning app, in FY20. The company strives to deliver an immense learning experience to early learners through gamification.

- E-sports (31.2 per cent of revenues): E-sports has emerged as the largest disruptor in the global traditional sports market. In FY18, the company acquired Nodwin Gaming - a market leader in the segment with a market share of 80 per cent in the Indian e-sports market. The company also owns Sportskeeda.com, which is the largest e-sports news website in India, with a focus on content across various e-sports and traditional sports such as WWE, cricket and soccer, among others.

- Telco subscription (21.3 per cent of revenues): Under this segment, the company offers over 1,021 android games targeting mostly first-time users. The company offers this service in associations with telecom operators.

- Freemium and real-money gaming: These include free-to-play sports-simulation games. Also, following its acquisition of HalaPlay Technologies, the company is also participating in fantasy sports. Besides, it is involved in the real-money gaming business in Kenya.

Strengths

Leadership position with a diversified portfolio: The company offers premium and popular gaming solutions across the e-sports and mobile-gaming platforms in India, with a significantly high market share.

Rise of the gaming industry: Once considered as a form of escapism, the gaming industry has emerged as one of the largest and fastest-growing segments within the media and entertainment sector.

Increasing penetration of smartphones: The penetration of smartphones in India is expected to reach 90 per cent by 2023, thereby leading to a significant rise in the numbers of mobile gamers.

Rise in Gen-Z population: The digitally mature Gen-Z population is more involved in gaming, owing to their familiarity with today's high-end technologies.

Risks

- Fast-changing technology can be a potential hindrance to the company's future prospects. Therefore, it needs to upgrade technology constantly to provide better services.

- Fierce competition and the increasing popularity of free-to-play and freemium games may lead to a decline in the company's revenues in the future. Media-rights licensing and partnerships with global game publishers are the key revenue drivers for its e-sports segment. For these two, the company is highly dependent on agreements with these global publishers.

IPO Questions

The company/business

1. Are the company's earnings before tax more than Rs 50 crore in the last twelve months?

No, although the TTM (trailing twelve months) numbers are not available, the company has reported a loss before tax of Rs 21 crore in the last financial year ending March 31, 2020.

2. Will the company be able to scale up its business?

Yes, being a technology-play company operating in a fast-growing industry, the company has enough room to expand its business. The Indian gaming industry is poised to benefit from the growth of digital infrastructure and a significant rise in the demand for quality gaming content. Also, the company's platform-based business model is easily scalable.

3. Does the company have recognisable brand/s, truly valued by its customers?

Yes, the company owns some of the very well-renowned brands, such as Kiddopia, Sports Keeda and Nodwin Gaming.

4. Does the company have high repeat customer usage?

Yes, for most of its offerings, the company has witnessed increased Monthly Active Users (MAUs) from 40.17 million in FY20 to an average of 57.54 million across all games for the nine-month period ending December 31, 2020.

5. Does the company have a credible moat?

No, entry barriers are relatively low in mobile gaming. So, new competitors can easily enter the market. Thus, there is always a threat of new and better gaming content, which could eat away the company's market share.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No, the company has to comply with various key regulations, such as the Information Technology Act, Data Privacy Bill and Gambling Legislations, along with various guidelines for online gaming.

7. Is the business of the company immune from easy replication by new players?

No, the low entry barriers and increasing demand for mobile gaming can attract new competitors in the Indian gaming industry.

8. Is the company's product able to withstand being easily substituted or outdated?

No, with the rapid advancement of technologies, the company faces the threat of new and better products from new and existing players.

9. Are the customers of the company devoid of significant bargaining power?

No, the customers of the company aren't devoid of any bargaining power, as they have plenty of other options to choose from.

10. Are the suppliers of the company devoid of significant bargaining power?

Yes, the company's suppliers include technology providers which do not have any bargaining powers.

11. Is the level of competition the company faces relatively low?

No, the company faces stiff competition from established entertainment and gaming companies, such as Sony Interactive Entertainment, Reliance Jio, Tencent and Microsoft Game Studios. Apart from this, emerging gaming start-ups, such as Dream 11, Mobile Premier League (MPL), and Game 24*7, have increased the competition.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

No, the promoters of the company held 22.9 per cent of the stake in the company pre-IPO, which would further reduce to 20.7 per cent post-IPO.

13. Do the top three managers have more than 15 years of combined leadership at the company?

Yes, Mr Rakesh Shah, CFO and Mr Manish Aggarwal, CEO, have a combined leadership of 16 years at the company.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with Sebi guidelines?

Yes, we have no reasons to believe otherwise.

15. Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

Yes. The company, as well as the management, is free from any material litigation that casts any doubt on the intention of the management.

16. Is the company's accounting policy stable?

Yes, we have no reason to believe otherwise.

17. Is the company free of promoter pledging of its shares?

Yes, the promoter's stake is free of any pledging.

Financials

18. Did the company generate current and three-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

No, the three-year average ROE and ROCE stood at -1.3 per cent and 0.7 per cent, respectively.

19. Was the company's operating cash flow positive during the previous year and at least four out of the last five years?

No, the company reported negative cash flow from operations in two out of the last five years.

20. Did the company increase its revenue by 10 per cent CAGR in the last five years?

Yes, the company's revenue has grown at a rate of 10.1 per cent annually in the last five years.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest-coverage ratio more than 2?

Yes, the company is debt-free.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

Yes, being in the digital technology business, there is not much reliance on working capital. Also, working-capital days stood at nominal 13.7 days in FY20.

23. Can the company run its business without relying on external funding in the next three years?

Yes, the company made various acquisitions in the past and have cash and cash equivalents of more than Rs 184 crore, which will reduce the need for relying on external funding for its operations.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

Yes, the company is debt-free.

25. Is the company free from meaningful contingent liabilities?

Yes. As per the prospectus, the company is free from any meaningful contingent liabilities.

The Stock/Valuation

26. Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

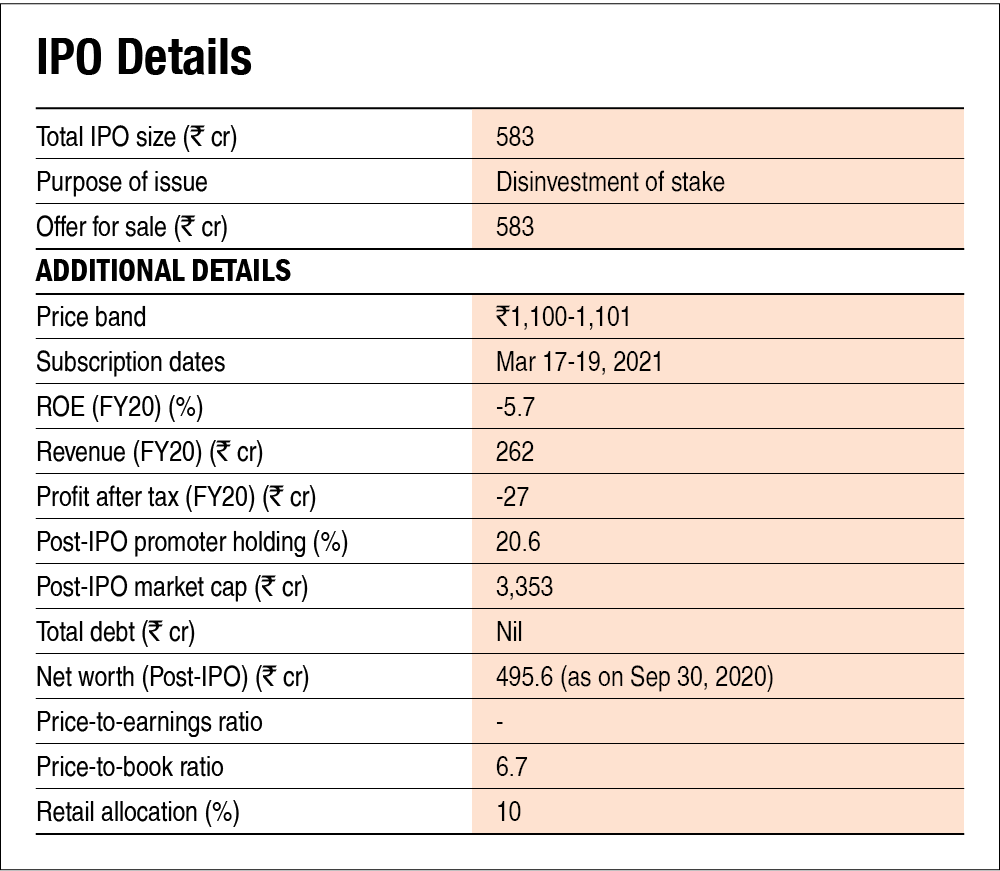

No, the company's stock will offer an operating yield of -0.6 per cent as per its losses in the last financial year and a post-IPO enterprise value of Rs 3169 crore.

27. Is the stock's price-to-earnings less than its peers' median level?

N/A. The company reported losses in the last financial year ending March 31, 2020. Also, there are no listed companies that are engaged in similar businesses.

28. Is the stock's price-to-book value less than its peers' average level?

NA. There are no listed companies whose business is comparable with the company's business. However, the stock current P/B stood at 6.7 based on September 30, 2020 numbers.

Disclaimer: The author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()