A boom phase is going on for specialty chemical players in India with several of these companies commanding rich valuations. Anupam Rasayan is the latest entrant to this party. The company is involved in custom synthesis and manufacturing of specialty chemicals. Custom synthesis means the exclusive synthesis of compounds a company carries out on behalf of its customer. The company's products are used as additives, ingredients or intermediates in its customers' final products.

The company divides its business into two parts:

a. Life science specialty chemicals (96 per cent of FY20 revenue) comprising products related to agrochemicals (around 70 per cent), personal care and pharmaceuticals

b. other specialty chemicals (4 per cent of FY20 revenue), comprising specialty pigment and dyes, and polymer additives

The company, over the years, has built strong relationships with various companies including Syngenta Asia Pacific, Sumitomo Chemical Company and UPL, helping it to grow its exports revenue to 68 per cent for FY20, with its major export market being Europe (36 per cent). Further, the company has also managed to increase its commercialised products from just 15 in 2015 to 41 in December 2020.

The chemical sector in India has benefitted in recent years from the China effect. First, the environmental crackdown in China on pollution-causing chemical plants in 2015 led to sudden supply-side problems, thereby benefiting the Indian players. And now, the pandemic is leading global companies to reduce their dependence on China. However, there is a long way to go for the $22 billion Indian specialty industry, which represents just 1-2 per cent of the world's exportable specialty chemicals as of today.

To reap the benefits of this trend, Indian chemical players have been doing massive capex spends. Anupam Rasayan has invested more than Rs 680 crore in the last three years (till FY20) and has more than doubled its capacity to 23,438 MTs.

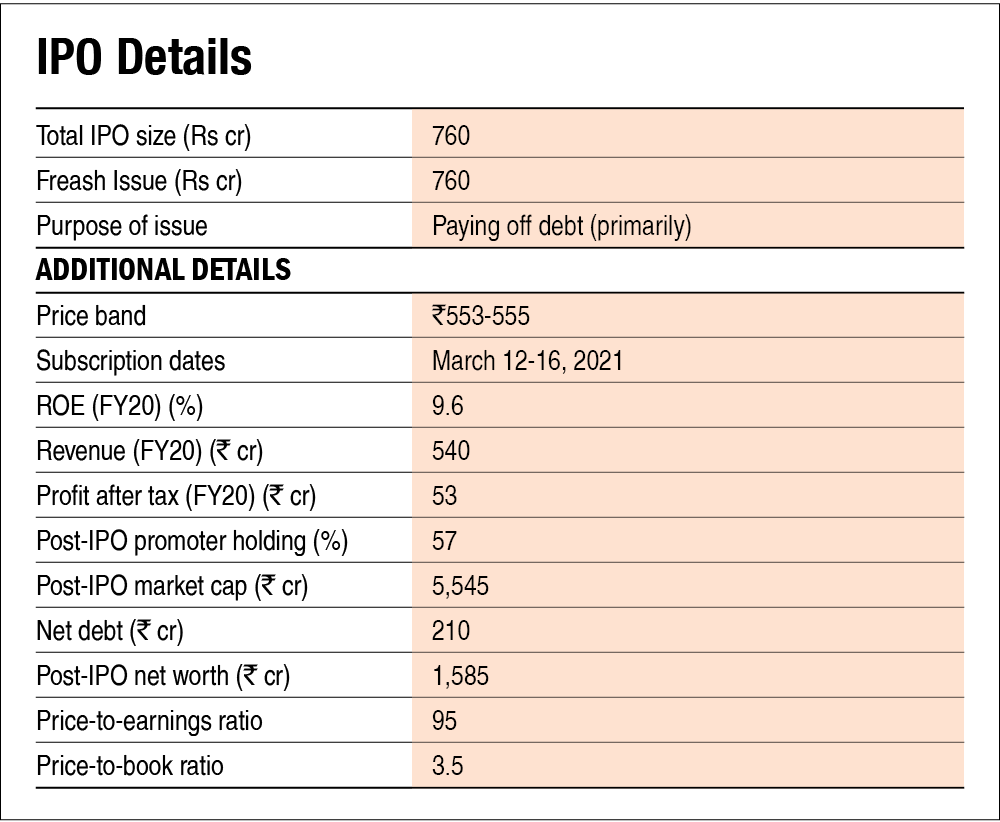

Now, the company is raising around Rs 760 crore through its IPO, out of which around Rs 564 crore would be used towards paying off existing debt. The company is also looking forward to ramping up its two recently commenced facilities. Further, it is also looking forward to adding more number of large customers, especially focusing on the Japanese market.

Strengths

- Custom synthesis players, such as Anupam Rasayan, enjoy a strong relationship with their customers. The business relationship is not only limited to selling a product but also of sharing confidential information, process knowledge, product development and more. As a result, customers typically select manufacturers after carefully reviewing them and tend to develop long-term relationships with them as well as limit the number of such manufacturers. This company has been manufacturing products for certain customers for over 10 years and as per the management, the company is the key supplier for its top 10 customers. Such a strong relationship provides high barriers to entry.

- The company, over the years, through focus on R&D, has been able to increase its product portfolio from 25 products in FY18 to 41 products as of December 2020.

- The company, over the years, has focussed on boosting its process capabilities. It utilises continuous processes to carry out various chemical reactions instead of the conventional batch technology. The conventional technology is extremely hazardous in nature and generates a large volume of acidic wastewater, which, in turn, is very difficult to treat and dispose.

- As a result of backward integration, the company's dependence on imported raw materials as a percentage of total raw materials purchases has decreased from 26 per cent in FY18 to 22 per cent in FY20. In particular, imported raw materials from China as a percentage of total raw materials purchases has also decreased to 12.2 per cent in FY20 from 17.1 per cent a year back.

Risks/Weaknesses

- The company carries 6-7 months inventory against the industry average of 1.5-2.5 months, highlighting poor working capital management. The management, in the con call, attributed this to single price quotes to customers each year, requirement of keeping a high inventory and other factors. High inventory days increase the working capital requirements of the company, which in turn leads to requirement of short-term debt and decreased profitability.

- The company will list at a price of Rs 555 and a P/E of around 95 based on twelve months earnings till December 2020 and post-IPO outstanding shares. The valuation of the company is at a steep increase as compared to the recent equity infusion by the corporate promoter, which was at a price of around Rs 200-250 in 2020.

- The company doesn't have any patented products. Moreover, its R&D expense is pretty low at 0.4 per cent of FY20 revenue as compared to its peers (3.5 per cent average).

- The company is vulnerable to industrial hazards and regulatory scrutiny since it deals with critical chemicals.

- The company has a concentrated set of customers with the top 10 customers accounting for around 87 per cent of its revenue. Loss of any big customer can result in substantial revenue loss.

- Almost 68 per cent of the company's revenue comes from exports, exposing the company to foreign exchange risk.

- The promoters of the company have given personal guarantees against some loans taken by the company.

IPO Questions

The company/business

1. Are the company's earnings before tax more than Rs 50 crore in the last twelve months?

Yes. The last twelve months PBT stands at Rs 83 crore as of December 2020.

2. Will the company be able to scale up its business?

Yes. Since 2017, the company has been on a capex drive. It has done a capital expenditure worth more than Rs 680 crore in the last three years (till March 2020). Currently, the overall capacity utilisation stands at around 75 per cent. Availability of ready excess capacity, strong tailwinds like the supply chain shift from China to India, government-led push, emergence of custom synthesis players for the specialty chemicals sector and India's low share (1-2 per cent) in exports of specialty chemicals provides the company with an opportunity to scale up its business smoothly.

3. Does the company have recognisable brand/s, truly valued by its customers?

Not applicable. The company is involved in custom synthesis and manufacturing of specialty chemicals. Its customers are mainly B2B players. In such a business, the application of brands is of little consequence.

4. Does the company have high repeat customer usage?

Yes. Custom synthesis players such as this company work in close association with their customers. The company enters into long-term agreements with its customers, usually ranging from two to five years. Strong relationships with its customers provides the company with high repeat customer usage.

5. Does the company have a credible moat?

Yes. Customers of custom synthesis and manufacturing companies work very closely with each other. This involves sharing of confidential information, process knowledge and other important business information. The whole process of acquiring new customers is a long process taking around 12 to 24 months with multiple levels of complexities. Such challenges provide a credible moat to custom synthesis players.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No. The company meets around 22 per cent of its raw material needs from imports, including close to 12 per cent coming from China. Further, around 68 per cent of its revenue in FY20 came from exports. Hence exposing the company to geopolitical risks. Moreover, the hazardous nature of company's products makes it vulnerable to regulatory scrutiny and changes.

7. Is the business of the company immune from easy replication by new players?

Yes. New players would find it very tough to replicate the business of the company. The company works in close association with its customers wherein the customer even shares confidential business information with the company. This trend is also evident in the fact that just the top 10 customers of the company account for around 87 per cent of its FY20 revenue. As per the management, the company is either the sole or at least amongst the top three suppliers for its top 10 customers.

8. Is the company's product able to withstand being easily substituted or outdated?

Yes. The company is a specialty chemicals manufacturer. Specialty chemicals are low-volume and high-value products which are used primarily as additives or to provide a specific attribute to the end product. Though the company needs to continuously spend on R&D to produce such high-value products, specialty chemicals can not be easily substituted or outdated.

9. Are the customers of the company devoid of significant bargaining power?

No. The top 10 customers of the company account for around 87 per cent of its revenue. Since the customers basically outsource a critical part of their business to custom synthesis players such as Anupam Rasayana, they enjoy substantial bargaining levers. These levers range from maintaining a minimum amount of inventory, indemnity to customers from losses arising on account of the company's inability to meet product specifications and more such things. Further, the company enters into a single-selling-price contract with its customers every year while the inventory is purchased multiple times. This, in effect, leads to an elongated working capital cycle.

10. Are the suppliers of the company devoid of significant bargaining power?

Yes. Cost of raw material has typically represented more than 55 per cent of the company's revenue in the last few years. The company sources its raw material from multiple vendors in India, China and Japan. Over the years, the dependence on raw material from China has reduced, coming down to 12.2 per cent (as of FY20). This was achieved through backward integration. Since the company doesn't rely on a small set of suppliers and enjoys a substantial number of payable days, the suppliers of the company do not have significant bargaining power.

11. Is the level of competition the company faces relatively low?

No. The $20 billion specialty chemicals sector in India is highly competitive with a number of players. The industry started experiencing a major tailwind ever since the Chinese government started cracking down on pollution-causing chemical companies in 2015. Yet, China accounts for approximately 17-18 percent of the world's exportable specialty chemicals, whereas India accounts for only 1-2 per cent. Presence of multiple domestic and international players makes specialty chemicals a competitive space to be in.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes. Post the IPO, the promoters will hold around 57 per cent stake in the company.

13. Do the top three managers have more than 15 years of combined leadership at the company?

Yes. The promoter-cum-MD of the company has been associated with the company for the last 28 years while the CFO has been associated with the company since 2005 (for 16 years).

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with SEBI guidelines?

Yes. We have no reason to believe otherwise.

15. Is the company free of any litigation in court or with the regulator that casts doubts on the intention of the management?

Yes. As per the company's prospectus, the company and the management is free from any material litigation.

16. Is the company's accounting policy stable?

Yes. As per the prospectus, the company has followed a stable accounting policy.

17. Is the company free of promoter pledging of its shares?

Yes. None of the shares of the promoter are pledged.

Financials

18. Did the company generate the current and three-year average return on equity (ROE) of more than 15 per cent and return on capital employed (ROCE) of more than 18 per cent?

No. The average three-year ROE till March 2020 stood at 10.5 per cent while the ROCE was around 9 per cent for the same period.

19. Was the company's operating cash flow positive during the previous three years?

No. The cash from operations was negative in FY18, while it turned positive in FY19 and FY20.

20. Did the company increase its revenue by 10 per cent CAGR in the last three years?

Yes. The company increased its revenue by 24 per cent from FY18 to FY20.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest-coverage ratio more than 2?

Yes. Taking into account that Rs 564 crore out of the IPO proceeds would be used towards paying off certain debt, the net debt-to-equity ratio post IPO will stand at around 0.13 (as per cash and cash equivalents as of December 2020).

22. Is the company free from reliance on huge working capital for day-to-day affairs?

No. For various reasons, the company maintains a substantial amount of inventory on its balance sheet and hence its inventory days have ranged 6-7 months, which is way higher than the industry average of 1.5-2.5 month. Post the IPO, the company would carry a Rs 25 crore working capital loan and would require short-term loans for smooth functioning of its businesses.

23. Can the company run its business without relying on external funding in the next three years?

Yes. The company has done substantial capex in the last three to four years and has recently commenced two new facilities. The overall capacity utilisation of the company (as of December 2020) stood at around 75 per cent and the management is looking forward to ramping up utilisation without incurring any new capex spend in the near future.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

No. The company's short-term borrowings have shown an increasing trend and have increased by around 16.8 per cent from March 2018 to December 2020. However, post-IPO, the outstanding short-term borrowings should drastically reduce.

25. Is the company free from meaningful contingent liabilities?

Yes. As per the prospectus, the company is free from any meaningful contingent liabilities.

The stock/valuations

26. Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

No. Based on post-IPO enterprise value of Rs 5754 crore and twelve month operating earnings as of December 2020, the yield would be around 2.5 per cent.

27. Is the stock's price-to-earnings less than its peers' median level?

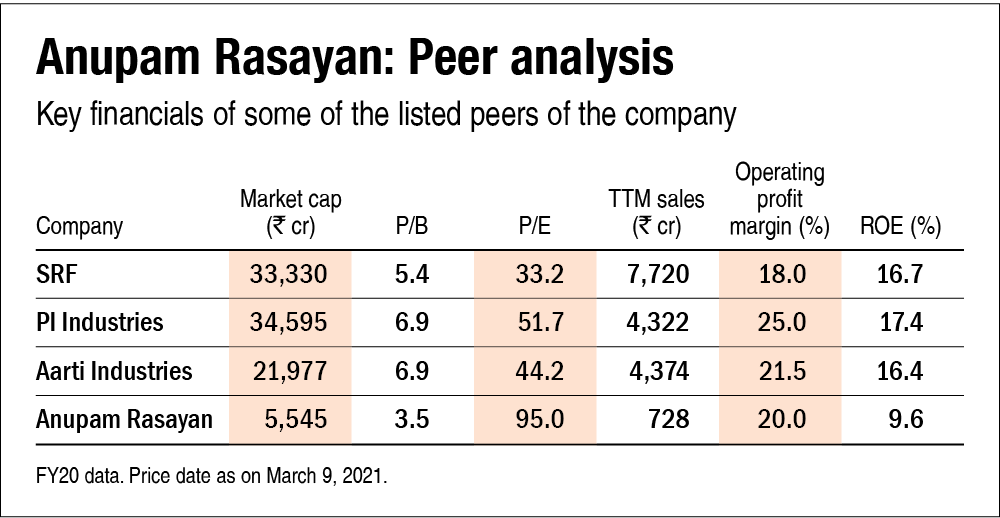

No. Based on December 2020 earnings, the stock would trade at a P/E of around 95, which is way higher than its peers' median P/E of 44.

28. Is the stock's price-to-book value less than its peers' average level?

Yes. Based on equity post the IPO, the stock would trade at a P/B of around 3.5, which is lower than its peers' median P/B of 6.9.

Disclaimer: The author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()