The world of investing is always innovating. Over time, many strategies, models, systems, etc., have made inroads into the investment world. Many of these had their genesis in the developed markets.

These days, fund investors frequently come across 'ESG' funds which are being launched by many fund houses. In the last one year, ending December 2020, seven such funds have been launched. Given the rise of this new category of funds, we felt it would make sense to delve deeper to understand what it offers and whether one should invest in it.

'ESG' funds seek to invest in businesses that score high on environmental, social and governance (ESG) standards. Over the last decade, ESG investing has become quite a rage in the developed markets, as seen from the surge in the number of funds and indices constituting socially responsible investing, impact investing, sustainable investing, etc.

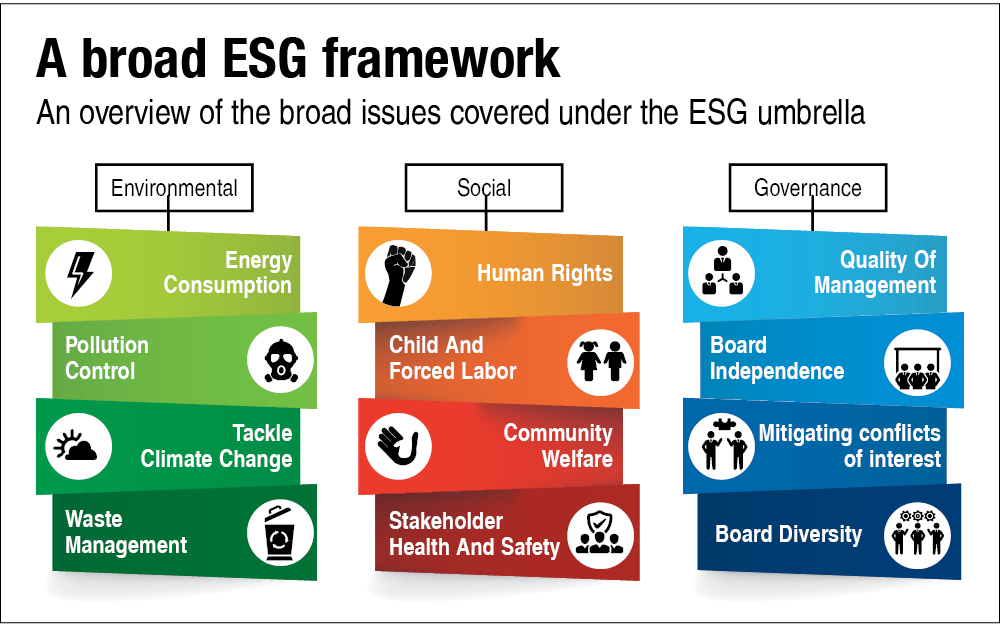

This trend has its roots in 2005, when Kofi Annan, the then UN Secretary-General, had invited a group of the world's largest institutional investors to develop the Principles for Responsible Investment (PRI), which centred around tackling the ESG issues (see the illustration 'A broad ESG framework'). This created the PRI network, the world's leading proponent of responsible investing.

The 521 signatories of the PRI group manage more than $103 trillion (as of March 2020) in line with the ESG principles. ESG assets have grown at about 22 per cent per annum since the inception of this theme in 2006.

Global and Indian perspectives

While ESG funds are new to Indian investors, there are more than 3,000 such schemes available globally. This suggests a welcome shift from the sole focus on profitability at any cost to sustainable growth.

Businesses across geographies have been improving their ESG disclosures over several years now. This has given birth to a number of third-party ESG data and ratings providers. This support industry is itself worth about a billion dollars, as per some estimates.

India doesn't have a long history of ESG-focused regulations. There has been some oversight on business by government bodies such as the Ministry of Environment, Forest and Climate Change and the Ministry of Labour and Employment but it has been nowhere close to the attention given to the ESG theme worldwide.

On the brighter side, through the Companies Act 2013, India became the first country in the world to make corporate social responsibility (CSR) mandatory for businesses with a certain turnover and profitability. Such businesses are required to spend 2 per cent of their average net profit of the past three years on CSR.

More recently, in late 2020, SEBI introduced new norms for ESG disclosures by the top 1,000 listed entities by market capitalisation. These have to be complied with by FY22. Actually, the market regulator's ESG focus dates back to 2012, when the top 100 listed companies were mandated to include a business responsibility report as part of their annual reports.

So, while the ESG theme is new in India, a realisation of its importance has been around for several years now.

The investment case

For the Indian investor, the million-dollar question is, should one invest in ESG funds? Well, your personal inclination towards the ESG cause does have a big role to play in this. Apart from that, here we evaluate the available ESG funds from an investment perspective.

The higher cause

As an individual investor, one might want to be altruistic with one's investments and ESG investing could be a way in which one can give back to the society and be more proactive towards the conservation of the environment. Investor support to ESG-grade companies might be a powerful motivation for businesses to bring a step change in their attitudes instead of just paying a lip service to ESG-related responsibilities.

But what really accounts for ESG compliance can be highly subjective due to its qualitative nature and hence one may feel confused about what qualifies and what doesn't. For example, big tech companies have announced their goals of becoming carbon-neutral and, in some cases, even carbon-negative in the coming decades. This would rate them quite high on environmental factors. However, in recent years, their policies related to data privacy have come under the scanner and continue to remain a concern affecting their standing on the social factors. So, finding all the three components of ESG in a single company could be a tough ask in itself.

Further, not all ESG parameters have clear-cut, black and white boundaries. For example, a popular electric-vehicle maker, which became the largest one by market cap in 2020, is planning to source cobalt from a Congolese mining giant. But certain human-rights groups have raised concerns regarding child labour against this mining major. Here, even though the automaker is not directly falling short on any ESG norms, one of its stakeholders in the value chain is blatantly flouting the social norms.

Also, not all 'green' investments are green. One may consider use of natural gas as more environment-friendly than coal. However, when one considers the process of fracking for extracting natural gas and its long-term ill effects on health and ecosystem, the so-called 'green' investment starts to look black.

The next issue is a lack of common ground among institutions as to which companies qualify as ESG investments. Indian AMCs seem to leverage their own research expertise, along with data from external rating agencies, for ESG assessment and evaluation. In certain cases, AMCs also utilise the expertise of their foreign partners (for example, Amundi for SBI and Schroders for Axis). Then there are certain funds - for instance, those launched by Mirae Asset - that are more passive in nature. Their ESG framework is as defined by an underlying index.

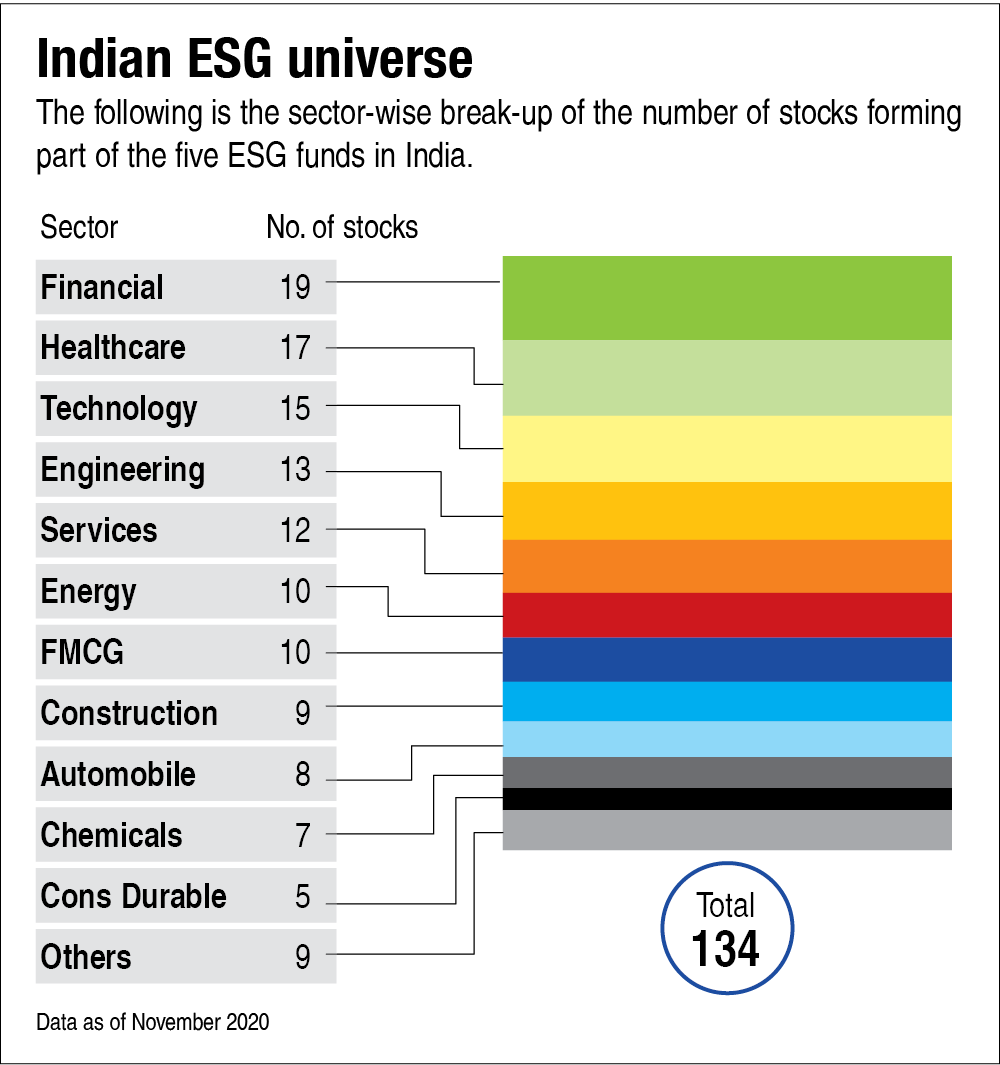

Further if we see the universe of stocks in the portfolios of five available ESG funds (as of November 2020), we get a universe of 134 stocks, which is fairly large (see the chart 'Indian ESG universe'). This proves that the criteria used to pick stocks in these funds varies in a fair degree, thanks to the subjective nature of the ESG classification.

This lack of standardisation is a much-criticised aspect of ESG funds worldwide. Universally, there are no common ESG factors, which makes it difficult to compare businesses. Thankfully, to address the issue of standardisation, the International Business Council released the ESG Reporting Metrics and Disclosure Standards in September 2020, developed in collaboration with Deloitte, EY, KPMG and PwC. The standards include 21 core and 34 expanded metrics and disclosures that are aligned with the United Nations' Sustainable Development Goals (established in 2015) pertaining to the ESG domain. However, it would take a while before they are universally accepted and improved upon over the years.

So, for an ESG-conscious investor, this means that until all such issues are taken care of, investing for a 'higher cause' may not be fully rooted in reality.

Performance

The primary goal of any investment decision is to generate sufficient returns for a given degree of risk. Given the risk that equity investors take, it's understandable that they would want their funds to be ahead of the rate of inflation at least. So, ESG funds should also be able to fulfil these expectations. However, given that the ESG funds available in India today have a limited history, we can't comment on their track record.

The proponents of ESG funds highlight that such funds invest in companies with sustainable models. As the human society progresses, such businesses have better chances of surviving and growing. In the Indian scenario, where foreign investors play a crucial role in market movements, sustainable businesses can also attract more of foreign capital. Clean governance would mean that raising capital would be relatively easier for such businesses. Finally, such stocks should also be less volatile as their ownership would be in stronger hands.

On the flip side, one should take the promise of ESG funds with a grain of salt. According to the IMF's Global Financial Stability Report published in October 2019, funds that are marketed as 'sustainable investment funds' may need to sound moderate while claiming any outperformance over their conventional peers as there was no conclusive evidence of one being superior to the other in terms of delivering returns for its investors.

Additionally, correlation should not be considered as causation. Stocks with superior ESG standing might have performed better, but that does not mean their outperformance could solely be attributed to the ESG phenomenon.

A unique investment opportunity?

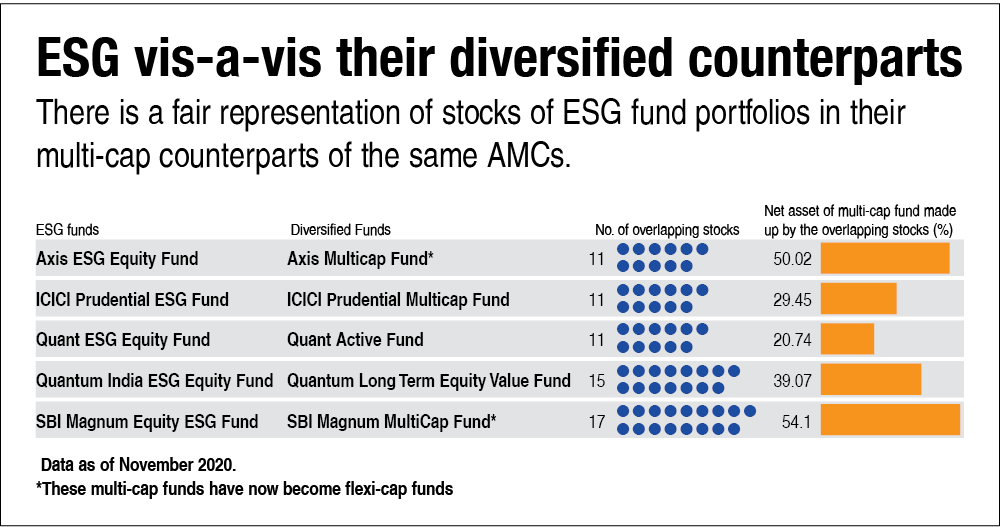

Are ESG funds really unique or does your plain-vanilla flexi-cap (now flexi-cap) also has enough of ESG plays. To check this, we compared the five available ESG funds with their diversified counterparts of the same AMC. See the table 'ESG vis-a-vis their diversified counterparts'.

We see that the that number of overlapping stocks between the ESG funds and their diversified counterparts ranges from 11 to 17 and the net asset of this overlap in the diversified funds varied from around 21 per cent to significant 54 per cent.

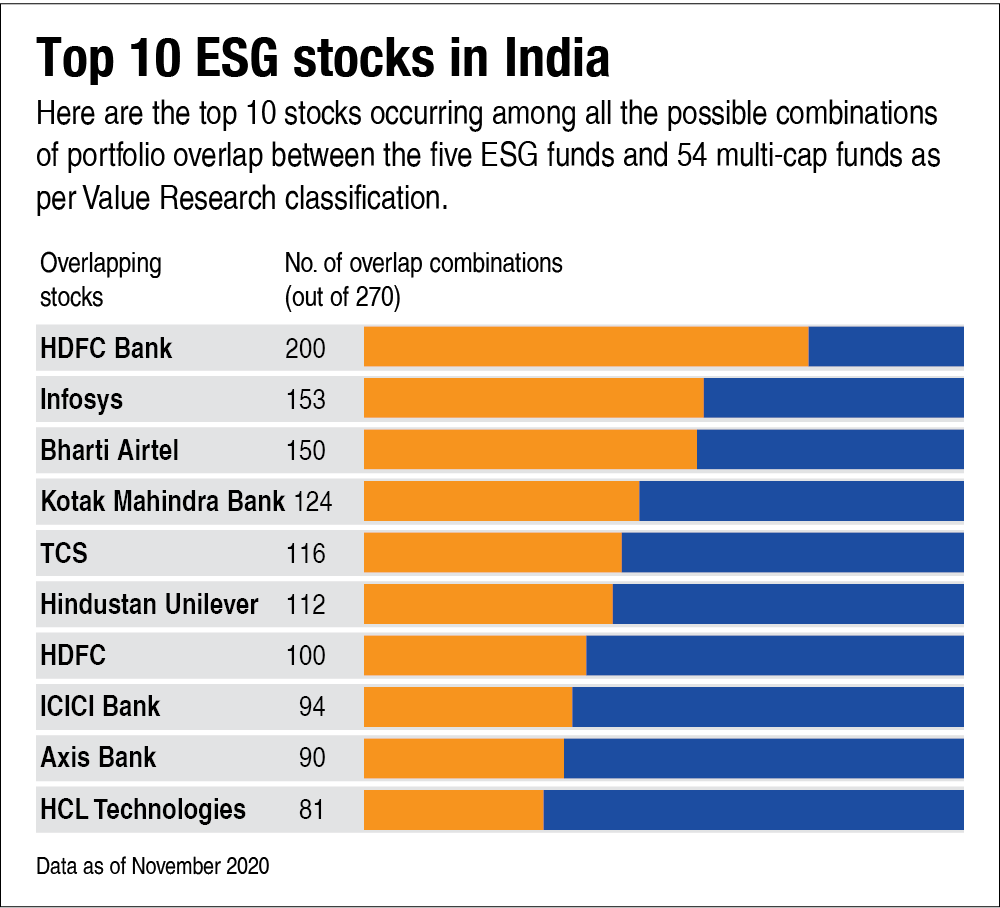

Further, when we compared the ESG fund portfolios with those of multi-cap funds (many of which have now become flexi-cap), the 10 stocks with the maximum overlap were majorly large caps, most of which belong to the financial and technology sector (see the chart 'Top 10 ESG stocks in India'). These would find a place in the portfolio of any good equity fund.

Additionally, some prominent AMCs such as SBI and Kotak have also established ESG framework at the fund house level, not just limiting it to ESG funds.

Thus, we find that there is a fair representation of ESG stocks, as determined by their selection in ESG funds, among the existing diversified funds. As the tailwinds for ESG picks up in India, this overlap in more diversified categories should only increase. This trend may be further fuelled by the fact that more and more companies will start becoming responsible, thus bringing a bigger proportion of the listed market cap in the country under the ESG radar.

So where does it take us?

The world's preparedness towards the handling of a pandemic-like situation was found wanting when an actual pandemic hit us last year. This has strengthened the case for a better handling of matters relating to climate change as its effects would be more long-lasting and in certain cases irreversible, with no ready solution. Thus, ESG factors are being looked at more seriously from a risk-mitigation perspective.

The ESG phenomenon could also help develop a responsible attitude among businesses towards the environment, society and a cleaner way of operating. This attitude can then percolate down the entire value chain. This will help create goodwill and safeguard against any regulatory backlash in the future. While some may fret about higher regulations and disclosures creating hurdles in the smooth functioning of businesses, one must understand that not having them could be an even bleaker proposition.

ESG is certainly much bigger, broader and more diverse than the kind of thematic funds we've had so far. Unlike other themes, we may not be as apprehensive about ESG's rationale as a steady-state part of your portfolio. But one shouldn't make investing decisions based on just these parameters. The ESG factors need to be a part of a broader investment framework and risk-assessment strategy so that one can safeguard against any unfavourable outcomes. Thus, as an investor, you need to assess whether ESG funds offer any unique investment opportunity that is not offered by your plain-vanilla diversified funds.

In its current form, ESG may not provide a distinct edge. Further, we have limited data on which to base our decisions. But as more companies become ESG-conscious, investment management teams would automatically embrace ESG in their investment-evaluation approach. And if the superior performance claims of ESG do materialise, then a higher degree of representation of such companies would naturally be there in mainstream diversified funds. After all, more companies which are genuinely responsive towards the environment and society are in everybody's interest.

Till that time is it better to stay on the sidelines and watch this trend unfold. One can continue investing in good diversified funds that have all of the bases covered in terms of risk, whether ESG-related or not.

Ask Value Research ![]()