Retail investors have conventionally used liquid funds either for very short-term investing needs or to park their emergency corpus. The premise behind investing in these funds is that they are able to generate reasonably better returns than a savings bank account without compromising on liquidity. Even though the returns aren't guaranteed as in the case of a bank account, the risk of loss in these funds is negligible.

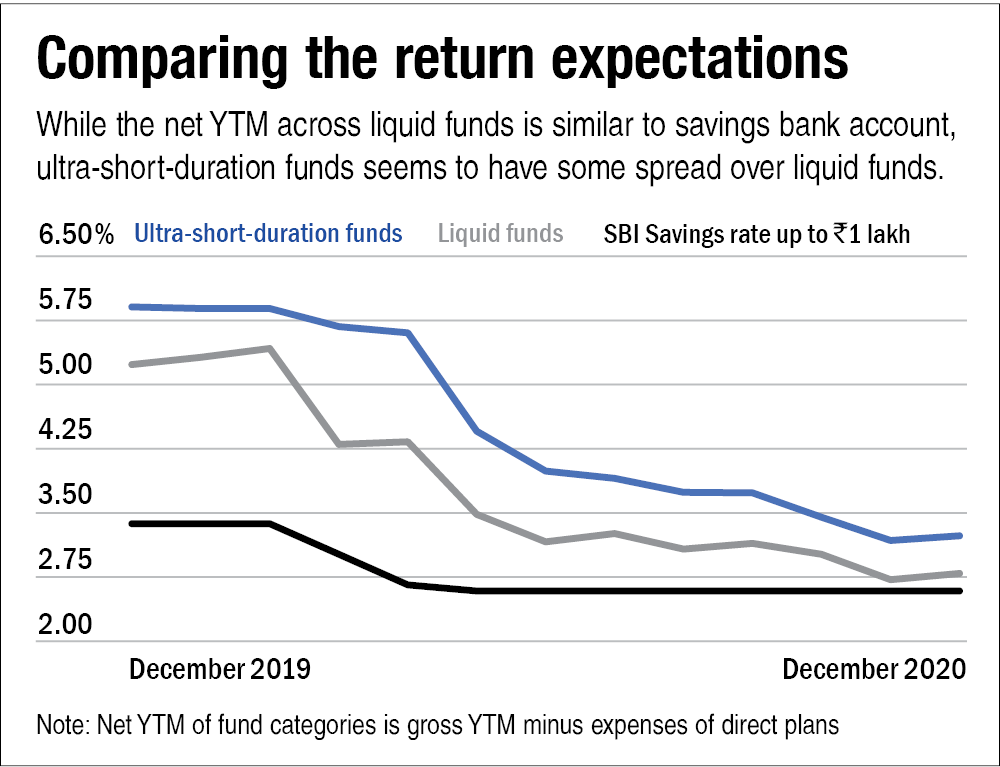

However, in the present scenario, with the interest rates hitting their multi-decadal lows, the advantage liquid funds had over a savings bank account has weaned off. The graph titled 'Comparing the return expectations' shows how the net yield-to-maturity (YTM) of liquid funds has dropped over the last one year to hover around at a touching distance of the savings account rates.

Many fund managers believe that while interest rates reversal may take some time to happen, the RBI's future course of action will be to incrementally start withdrawing the surplus liquidity from the markets. Therefore, yields towards the shorter end of the yield curve, which are fairly compressed, may inch up a bit. So as and when liquid funds' portfolios become due for maturity, these funds will reinvest at better yields, thereby giving slightly better returns to investors. Although, they will still be only slightly more than the savings account rates.

Faced with a dilemma as to whether it still makes any sense to trade the surety of their bank account for a liquid fund, retail investors might want to consider ultra-short-duration funds, the closest siblings of liquid funds.

Ultra-short-duration funds, to begin with, are placed right next to liquid funds in terms of the tenure of bonds they invest in. So, while the latter invest in bonds having a tenure of up to three months, ultra-short-duration funds build a portfolio of bonds maturing in three to six months. The graph 'Comparing the return expectations' shows that even though the gap between the yields of these categories has narrowed down of late, ultra-short-duration funds are still yielding about 0.5 per cent more than liquid funds. For some investors, this margin can be meaningful enough to shift a portion of their portfolio allocation.

Devang Shah, Deputy Head-Fixed Income, Axis Mutual Fund, says, "In a neutral environment where we are not expecting rate hikes and immediate liquidity withdrawal, one should be investing in the ultra-short-duration category."

Shah also believes that an investor should look at the gap in YTMs between the liquid and ultra-short-duration categories. "If the gap is flat or up to 25 basis, then you should stay in liquid funds. If the YTM gap is larger, like in present times, one gets a significant cushion. So, for the near term, if the investment horizon is at least three months, I would continue to advise the ultra-short-duration category," he notes.

The element of risk

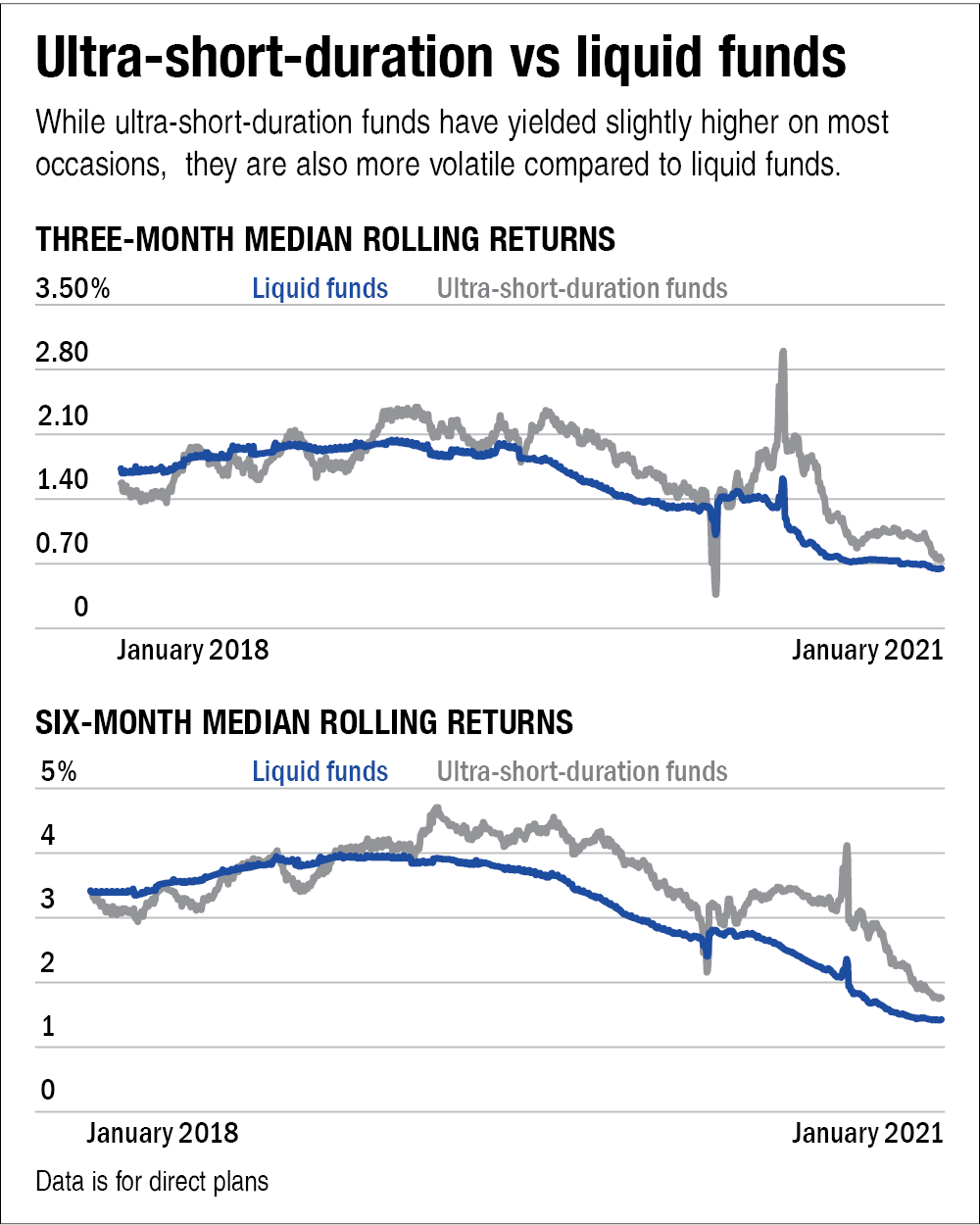

It needs to be kept in mind that ultra-short-duration funds are more volatile than liquid funds. A comparison of the daily rolling three-month and six-month return (see graph Ultra-short-duration vs liquid funds) of the two categories highlights this.

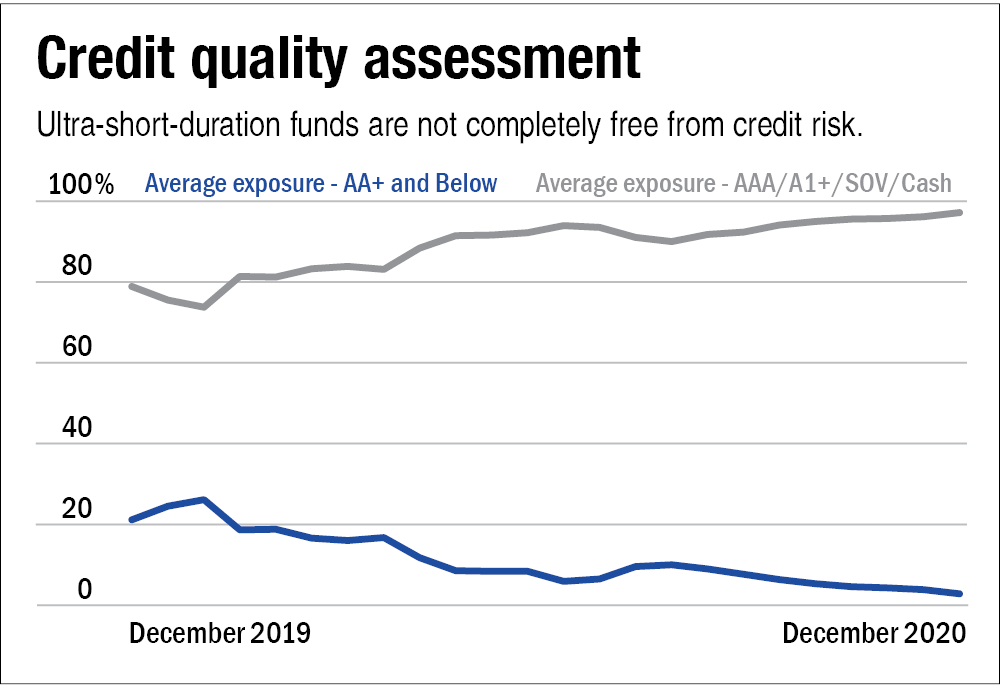

Another caveat is about the credit quality. While ultra-short-duration funds as a category are generally low on credit risk, there are some funds which have a history of taking notable exposures to less than AAA rated papers. So, selectivity is important.

What should an investor do?

For an allocation where the priority is liquidity and safety of capital, returns come secondary. For people who are not willing to accept a higher element of risk in their emergency bucket, allocating in a liquid fund or savings account might be worth a thought. However, if you don't mind the volatility, you may consider having some portion invested in ultra-short-duration funds. However, once the interest rates start to rise, you may be better off moving back to liquid funds.

If you choose to invest in ultra-short-duration funds, do take note of the expense ratios. In the ultra-short-duration category, the gap between the expenses of direct and regular plans is so wide that even shifting from the regular plan to the direct plan may prop up your returns by close to 0.5 per cent. Therefore, investing in a direct plan would be a better option.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()