Home First Finance Company India Limited (HFFC) was incorporated in 2010. As its name suggests, the company is predominantly involved in providing home loans, with a focus on affordable housing. Promoted by private equity funds, it has a loan book of Rs 3,730 crore.

With a network of 70 branches, the company currently operates in 11 states, which account for around 79 per cent of the affordable-housing finance market in India. Almost 80 per cent of its loan portfolio is concentrated in just four states (Gujarat, Maharashtra, Tamil Nadu and Karnataka), with Gujarat alone constituting almost 40 per cent to its portfolio.

The company also offers construction finance, loans for purchasing commercial property and loans against property to both salaried and small business owners/self-employed customers.

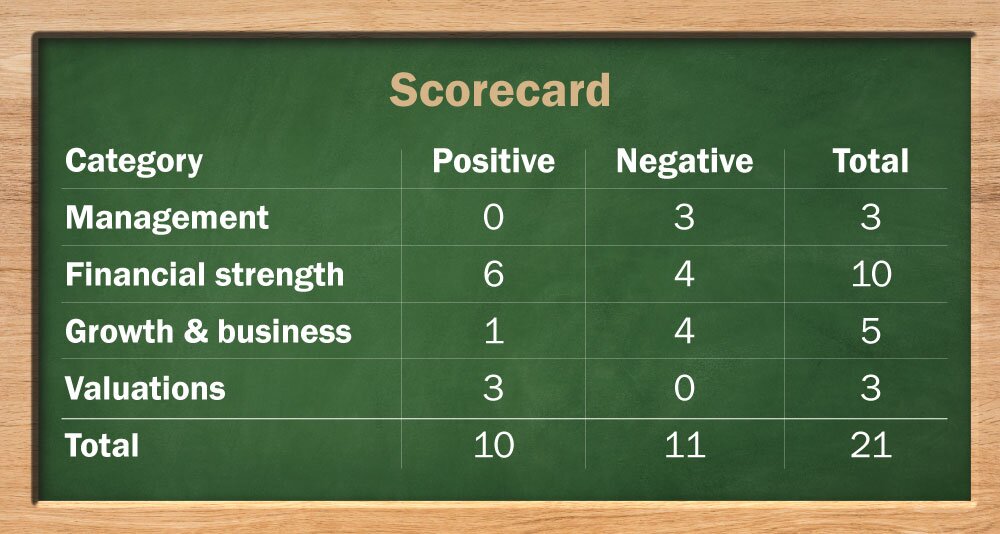

Strengths

- Focus on affordable housing: The company specifically focuses on customers in the middle- and low-income strata, with many of them being first-time borrowers. It assesses all income sources of a potential borrower, including those earned in cash, given that many employees may not necessarily be working in establishments that give salary slips or follow other documentation processes. This allows the company to get a holistic view of a borrower's true income and is, therefore, able to offer higher loan amounts.

With an average ticket size of Rs.10.1 lakh, the company mainly focuses on the home-loan segment, which accounts for around 92 per cent of its loan book. Also, the company's preference for lending to salaried borrowers, who constitute around 73 per cent of its customers, improves its loan book's stability. - Extensive use of technology: The company utilises technology considerably in its operations. Digital tools are used to make the data collection/customer onboarding processes faster and also make key decisions related to credit appraisal. By leveraging the company's IT systems, its centralised team is able to sanction loans within 48 hours. Even during the COVID-19-led national lockdown, the company's operations were largely unaffected, as employees seamlessly transitioned to working from home.

Risks & Concerns

Asset quality: The very fact that the company lends to borrowers who belong to the middle- and lower-income sections of the society increases the possibility of loan defaults. The pandemic has had an adverse impact on many such borrowers and this was reflected in an increase in the number of loans which were 30-day past due as of October 2020. This proportion of loans, which were 30 days past due, jumped from 1.6 per cent in March 2020 to 3.1 per cent and the management expects the number to remain elevated for the upcoming quarters. Although the stated net NPA ratio was 0.5 per cent as on September 30, 2020, given the Supreme Court's order which prevents the bank from recognising NPAs, the real value of NPAs is higher.

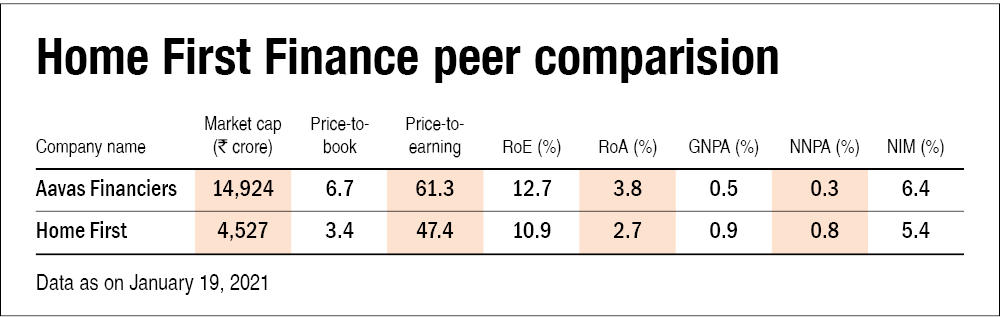

Valuation: Given that the company allotted shares on a preferential basis to private equity firms and its employees at Rs 334 just three months ago, its current asking price of Rs.517-518 seems a bit steep. Also, the 63 per cent CAGR in its AUM in the last three years was achieved on a smaller base and is likely to decrease in the future.

Competition: Although the affordable-finance market is growing, there is a lot of competition in this segment. It may be difficult for the company to compete with larger companies who benefit from higher economies of scale as reflected in their lower cost of funds.

IPO Details

Total IPO size: Rs 1153.7 cr

Fresh issue: Rs 265 cr [23%]

Offer for sale: Rs 888.7 cr [78%]

Price band: Rs 517-518

Subscription dates: Jan 21, 2021, to Jan 25, 2021

ROE (FY20): 8.5%

Net interest income (FY20): Rs 151.2 cr

Book value: Rs 988.1 cr as of September 2020

Book value (Post-IPO): Rs 1,332 cr

Management

1. Is the company free of any regulatory penalties?

No, National Housing Bank penalised the company multiple times in the past, with the latest one being in October 2020. Penalties were imposed for varied reasons, such as incorrect classification of data, failure to carry out a secretarial audit, etc.

2. Does the company provide for its non-performing assets (NPAs) adequately? More specifically, is the ratio of provisions to gross NPAs more than 50 per cent?

No, the company has provided for only 33 per cent.

3. Do the top five managers have stock as a meaningful part of their compensation (more than 50 per cent)?

No.

Financial strength and stability

1. Does the company have any fresh slippage to the total advances ratio of less than 0.25 per cent? (Fresh slippages are loans that became NPAs in the last financial year).

No. For the financial year 2020, the ratio of fresh GNPA total advances was 1.8 per cent.

2. Did the company generate a current return on equity (RoE) of more than 12 per cent and return on assets (RoA) of more than one per cent?

No. While annualised RoA was 3 per cent, the annualised RoE was 11 per cent as on September 30, 2020.

3. Has the company increased its loan book by 20 per cent annually over the last three years?

Yes, the loan book has grown at a CAGR of 63 per cent over the last three years.

4. Has the company increased its Net Interest Income (NII) by 20 per cent annually over the last three years? (Net interest income is the difference between the revenue that is generated from a bank's assets and the expenses associated with paying out its liabilities).

Yes, the net interest income has gone up by 2.4 times.

5. Is there any direct relationship between the increase in loan book and the increase in Net Interest Income (NII)?

Yes, there is a very strong relationship of 0.99 (correlation of one indicates a perfect relationship with each other).

6. Is the company's capital adequacy ratio more than 15 per cent? (The capital adequacy ratio (CAR) is a measure of a bank's capital. It is expressed as a percentage of a bank's risk-weighted credit exposures).

Yes, the CAR stood at 51 per cent as of September 30, 2020.

7. Can the company run its business without relying on any external funding in the next three years?

No, the lending industry is very capital intensive and there will always be a need for additional capital for expansion.

8. Did the company generate an average NIM of more than 3 per cent in the last two years? (Net interest margin or NIM denotes the difference between the interest income earned and the interest paid by a bank or financial institution relative to its interest-earning assets like cash).

Yes, its NIM for FY2019 and FY2020 stood at 5.5 per cent and 5.4 per cent, respectively.

9. Is the Average Gross NPA Ratio (Gross NPAs/Total Advances) over the last three years less than 1 per cent and the Net NPA Ratio (Net NPAs/Total Advances) less than 0.5 per cent?

No. While the GNPA's have been less than 1 per cent, the Net NPA ratio has been higher than 0.5 per cent.

10. Does the company have a cost-income ratio of less than 50 per cent?

Yes, the cost-to-income ratio for FY20 was around 35 per cent.

Growth and business

1. Will the company be able to scale up its business?

Yes. The market for affordable housing is vast and the company claims that its market share is just 1 per cent. As the housing stock in the country is increasing, the company should be able to scale up its business.

2. Does the company have a loan book of more than Rs 100,000 crore?

No,. the company's loan book was at Rs.3,730 crore as on September 30, 2020.

3. Does the company have a recognisable brand truly valued by its customers?

No. Even though the company is doing things uniquely, its internal technological workings will not be known to consumers, especially when the nature of business is such that there is hardly any repeat business.

4. Does the company have a credible moat?

No. This is because anybody can emulate the company's business practice - considering informal sources of income during the credit-appraisal process and using technology.

5. Is the level of competition faced by the company relatively low?

No. There are several players in this industry and many of these players are larger and therefore, the level of competition is not low.

Valuation

1. Is the company's price-to-earnings ratio less than its peer median level?

Yes. While Aavas Financiers trades at a trailing 12-month price-to-earnings ratio of 61, the IPO is being priced at a P/E of 47.

2. Is the company's price-to-book value less than its peer median level?

Yes. While Aavas Financiers is trading at a P/B value of 6.72, the upper band of issue price values Home First at a P/B ratio of 3.6.

3. Is the company's PEG ratio less than one? (The price/earnings to growth ratio (PEG ratio) is a stock's price-to-earnings (P/E) ratio divided by the growth rate of its earnings for a specified time period).

Yes. It has been 0.39 for the last three years.

Disclaimer: Author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()