The company is the national master franchisee of the Burger King brand in India, which is the world's second-largest fast-food burger brand in terms of the number of restaurants. The Burger King brand has a global network of 18,675 restaurants in more than 100 countries. In India, it is one of the fastest-growing international QSR (Quick Service Restaurant) chains since its launch in the country.

Having a market share of 5 per cent in India's Rs 348-billion QSR market, the national master franchisee of the brand had 261 outlets across 17 states as on September 30, 2020, with QSR Asia as its holding company. Its restaurants are primarily located in four different locations, comprising high streets, shopping malls, food courts and drive-thru outlets.

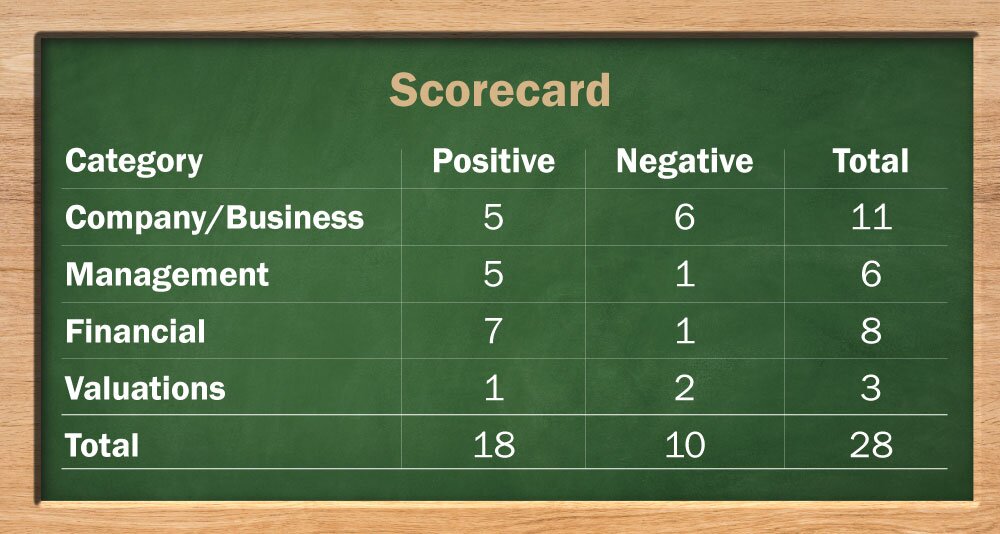

Strengths

- It is the national master franchisee of the Burger King brand in India, with exclusive rights to develop, establish, operate and franchise Burger King-branded restaurants in India.

- It offers a variety of value meals in a wide range of vegetarian and non-vegetarian offerings.

- Increased urbanisation, rising working population and income levels and the growing demand for fast food are some of the key growth drivers for the company.

- Also, the growing penetration of smartphones and the internet in India and the growing demand for online food delivery are some other tailwinds.

- Quick service restaurants are expected to grow at a rate of 19 per cent over the next five years.

- The company intends to open 700 outlets from currently 261 till December 31, 2026.

Risks/Concerns

- Change in the eating pattern owing to the pandemic and increasing awareness for a healthy lifestyle may adversely affect the company.

- The company has reported losses in the last four financial years and may incur losses in the near future.

- It operates in a highly competitive market and faces stiff competition from other QSR chains, such as Domino's, McDonald's, Subway, to name a few. Besides, there is competition from local unorganised players.

Total IPO size: Rs 810 crore

Purpose of issue: Disinvestment of the stake by QSR Asia

Fresh issue: Rs 450 crore

Offer for sale: Rs 360 crore

Additional details

Price band: Rs 59-60

Subscription dates: December 2-4

ROE (FY20): -29.2 per cent

Revenue (FY20): Rs 847 crore

Profit after tax (FY20): Rs. -77 crore (Loss)

Post-IPO, promoter holding: 60 per cent

Post-IPO, market cap: Rs 2259-2290 crore

Total debt: 196 crore

Net worth (Post IPO): Rs 669 crore (as on Sep 30, 2020)

Price/earnings ratio: NA

Price/book ratio: 3.4

Retail allocation: 10 per cent

IPO Questions

Company / Business

1. Are the company's earnings before tax more than Rs 50 cr in the last twelve months?

No, the company reported a loss of Rs 76 crore before tax in FY20. Also, the company has been reporting losses since FY17.

2. Will the company be able to scale up its business?

Yes, the company has been continuously opening up new outlets since its inception in India, with 261 outlets as on September 30, 2020. The company intends to open at least 700 outlets by December 31, 2026.

3. Does the company have recognisable brand/s, truly valued by its customers?

Yes, Burger King is the second-largest fast-food burger brand globally, with a network of 18,675 restaurants in more than 100 countries.

4. Does the company have high repeat customer usage?

Yes, a global brand name and the increasing demand for eating-out and fast-food have allowed Burger King to strengthen its position in the food business.

5. Does the company have a credible moat?

No, the company operates in a highly competitive market and competes with renowned international brands. Besides, it faces tough competition from the unorganised sector.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No, the company is subject to a broad range of food and safety regulations.

7. Is the business of the company immune from easy replication by new players?

Yes, the company has a large presence with more than 260 outlets across India, which may not be very easy to replicate.

8. Is the company's product able to withstand being easily substituted or outdated?

No, the company operates in the food and beverage industry and faces tough competition from McDonald's in the burger business.

9. Are the customers of the company devoid of significant bargaining power?

No, as stated above, the company operates in a highly competitive industry and customers of the company have a lot of other options to choose.

10. Are the suppliers of the company devoid of significant bargaining power?

Yes, the company has multiple suppliers for most of its key ingredients and actively manages its contracts with its suppliers of food ingredients and packaging materials.

11. Is the level of competition the company faces relatively low?

No, being in quick service restaurant business, the company faces very high competition.

Management

12. Does any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes, pre-IPO the promoters of the company hold 94 per cent stake in the company. Post-IPO the promoter will hold 60 per cent stake in the company.

13. Do the top three managers have more than 15 years of combined leadership at the company?

No, the company commenced its operations in 2014 in India.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with Sebi guidelines?

Yes, we have no other reason to believe otherwise. However, one of the directors is under an SFIO (Serious Fraud Investigation Office) investigation and the matter is currently pending for affairs of Royal Twinkle Star Club and other group companies.

15. Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

Yes, there is no material litigation going on against the company.

16. Is the company's accounting policy stable?

Yes, we have to reason to believe otherwise.

17. Is the company free of promoter pledging of its shares?

Yes, the promoter's shares are free of pledging.

Financial

18. Did the company generate the current return on equity of more than 15 per cent and return on capital of more than 18 per cent?

No, the company has been incurring losses since FY17 and its current ROE and ROCE are -29.2 per cent and -1.6 per cent, respectively.

19. Was the company's operating cash flow positive during the previous year and at least three out of the last four years?

Yes, the company reported positive operating cash flows in the last three out of four years.

20. Did the company increase its revenue by 10 per cent CAGR in the last three years?

Yes, the company's revenues have grown at a CAGR of 56.3 per cent in the last three years.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest coverage ratio more than 2?

Yes, the net debt-to-equity ratio stood at 0.6 as on September 30, 2020.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

Yes, the company has a negative working capital cycle of 28 days, wherein it receives payment well before it has to pay its suppliers.

23. Can the company run its business without relying on external funding in the next three years?

Yes, the company plans to use the fresh issue through IPO to repay debt and incur capital expenditure in the next three years.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

Yes, the short-term borrowings declined from Rs 100 crore in FY19 to Rs 20 crore as on September 30, 2020.

25. Is the company free from meaningful contingent liabilities?

Yes, contingent liabilities account for less than 1 per cent of the equity.

The Stock/Valuation

26. Does the stock offer operating earnings yield of more than 8 per cent on its enterprise value?

No, the stock will offer a yield of -0.3 per cent post IPO based on March 2020 numbers.

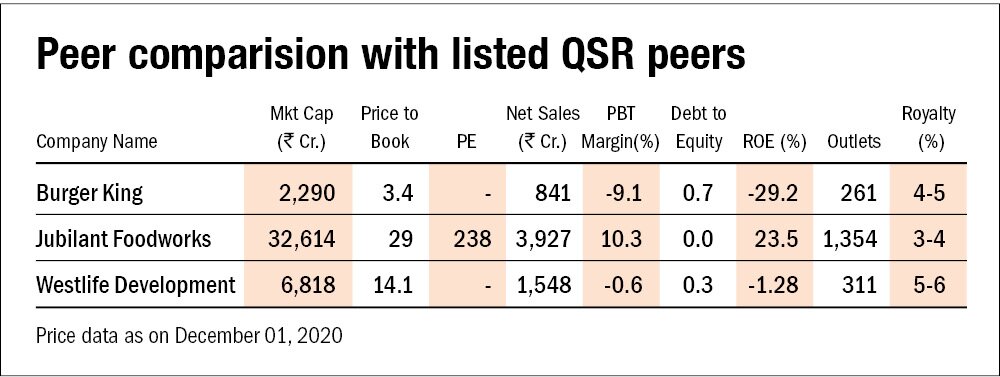

27. Is the stock's price to earnings less than its peers' median level?

NA, since the company is loss-making, P/E ratio is not applicable.

28. Is the stock's price-to-book value less than its peers' average level?

Yes, the stock's P/B ratio stood at 3.4, which is less than its peers average level of 21.7.

BRLM- Kotak Mahindra Capital, CLSA, Edelweiss Financial Services, JM Financial.

Ask Value Research ![]()