SFBs are set up in line with the government's initiative of financial inclusion and inclusive banking for the underbanked or unbanked sections of the economy. Holding an edge over NBFCs, these banks can take deposits, which enable them to get funds at low costs and earn high-interest margins. Further, the deposit rates of some SFBs are higher than those offered by larger commercial banks.

With a network of 991 banking outlets across 17 states and union territories in India, Equitas Small Finance Bank is the leader among SFBs in terms of the distribution network. Further, it is the second-largest SFB in India in terms of assets under management (AUM) and total deposits in FY19.

The SFB's product offerings include small business loans, housing loans, agriculture loans, vehicle loans and microfinance loans. On the liability side, it offers current accounts, salary accounts, savings accounts and term deposits to its customers. Besides, Equitas SFB also offers a range of third-party products, including insurance, FASTag for toll plazas and mutual fund products.

Strengths

- A well-diversified asset portfolio: Equitas SFB has been able to offer a diverse basket of products to its customers and at the same time, has significantly reduced its dependence on the microfinance business from 28.4 per cent on March 31, 2018 to 23.2 per cent on June 30, 2020.

- Large presence- It is a leader among SFBs in terms of the distribution network.

Risks and Concerns

- COVID-19 impact: There was a significant decline in collections as well as disbursements, owing to the pandemic and the restrictions imposed by the lockdown, which could also lead to an increase in NPAs going forward.

- Fierce competition: The company operates in a highly competitive industry. Also, the products offered by the company are also provided by large banks, NBFCs and microfinance companies.

- Concentration of advances: A majority of advances are from customers located in Tamil Nadu, accounting for 55 per cent of the total advances as on June 30, 2020. Any development, such as political unrest and any kind of disruption, can adversely affect its operations.

Total IPO size: Rs 510-518 crore

Fresh issue: Rs 280 crore

Offer for sale: Rs 237.6 crore

Price band: Rs 32-33

Subscription dates: October 20-22, 2020

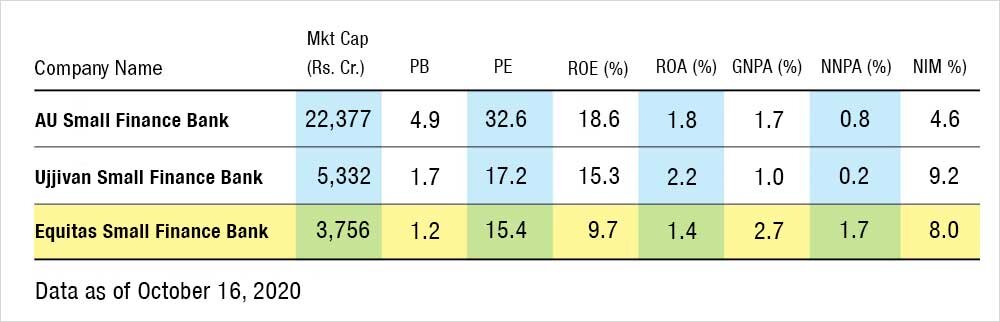

ROE (FY20): 9.7 per cent

Net interest income (FY20): Rs 1495.3 crore

Post-IPO valuation: Rs 3756 crore

Book Value (Pre-IPO): Rs 2788 crore

Book Value (Post-IPO): Rs 3068 crore

Management

1. Is the company free of any regulatory penalties?

No, the RBI has put two penalties on the company i.e. restrictions on the opening of new branches and freezing of remuneration of the managing director and chief executive till further notice, as they failed to list the company on the stock exchange within three years of the commencement of operations.

2. Does the company provide for its non-performing assets (NPAs) adequately? More specifically, is the ratio of provisions to gross NPAs more than 50 per cent?

No, however, the company had provisions of 48.8 per cent as on June 30, 2020.

3. Do the top five managers have stock as a meaningful part of their compensation (more than 50 per cent)?

No, the company has an ESOP plan but no option has been exercised or allotted as of now.

Financial strength and stability

1. Does the company have any fresh slippage to the total advances ratio of less than 0.25 per cent? (Fresh slippages are loans that became NPAs in the last financial year).

No, the fresh slippage for FY19 stood at 0.79 per cent and gross NPA stood at Rs 417 crore as on June 30, 2020.

2. Did the company generate a current return on equity (RoE) of more than 12 per cent and return on assets (RoA) of more than one per cent?

No, ROE for FY19 stood at 9.7 per cent, however, ROA stood at 1.4 per cent during the same period.

3. Has the company increased its loan book by 20 per cent annually over the last three years?

Yes, the company was able to increase its loan book by more than 34 per cent annually over the last three years.

4. Has the company increased its Net Interest Income (NII) by 20 per cent annually over the last three years? (Net interest income is the difference between the revenue that is generated from a bank's assets and the expenses associated with paying out its liabilities).

Yes, the company was able to increase its NII by around 41 per cent over the last three years.

5. Is there any direct relationship between the increase in loan book and the increase in Net Interest Income (NII)?

Yes, they both appear to move in line with each other, with a very strong correlation of 0.99 (Correlation of one indicates a perfect relationship with each other) from FY17 to FY20.

6. Is the company's capital adequacy ratio more than 15 per cent? (The capital adequacy ratio (CAR) is a measure of a bank's capital. It is expressed as a percentage of a bank's risk-weighted credit exposures).

Yes, the capital adequacy ratio stood at 22 per cent as on June 30, 2020, as compared to 15 per cent mandated by the RBI. Further, the proceeds raised from the IPO will be used to increase the capital base.

7. Can the company run its business without relying on any external funding in the next three years?

No, the industry wherein the company operates is capital-extensive and in order for expansion, additional capital is required.

8. Did the company generate average NIM of more than three per cent in the last two years? (Net interest margin or NIM denotes the difference between the interest income earned and the interest paid by a bank or financial institution relative to its interest-earning assets like cash).

Yes, the company generated an average NIM of 7.8 per cent in the last two years.

9. Is the Average Gross NPA Ratio (Gross NPAs/Total Advances) over the last three years less than one per cent and the Net NPA Ratio (Net NPAs/Total Advances) less than 0.5 per cent?

No, the average gross NPA and Net NPA stood at 2.6 and 1.5 per cent, respectively, in the last three years.

10. Does the company have a cost-income ratio of less than 50 per cent?

No, the cost-to-income ratio stood at 67.2 per cent as on June 30, 2020.

Growth and Business

1. Will the company be able to scale up its business?

Yes, due to the absence of formal banking services for a significant section of the Indian population and the government's growing focus on financial inclusion, coupled with the SFB's largest network of banking outlets, will help the bank to scale up its business. Further, the growing demand for affordable housing and vehicles is likely to give a boost to its products.

2. Does the company have a loan book of more than Rs 100,000 crore?

No, the company had a total loan book of Rs 15,572.9 crore as on June 30, 2020.

3. Does the company have a recognisable brand truly valued by its customers?

No, the company operates in a highly competitive industry wherein the interest rate plays a very vital role. Some of its competitors have a low cost of funds as compared to the bank, which may pose a threat to its market share.

4. Does the company have a credible moat?

No. Although the company is the second-largest small finance bank in terms of assets under management (AUM) with a market share of 16 per cent, it operates in a highly competitive industry and faces stiff competition from other small finance banks, large banks, non-banking finance companies and microfinance companies.

5. Is the level of competition faced by the company relatively low?

No, as stated above, the company faces significant competition from unorganised, small participants, in addition to the above-mentioned organised sector participants.

Valuation

1. Is the company's price-to-earnings ratio less than its peer median level?

Yes, it is priced at a P/E of 15.4 times on a post-IPO diluted basis against the median P/E of 24.9 times.

2. Is the company's price-to-book value less than its peer median level?

Yes, its price to book stands at 1.2 times based on the fully diluted post-IPO basis, which is less than the industry median of 3.3 times.

3. Is the company's PEG ratio less than one? (The price/earnings to growth ratio (PEG ratio) is a stock's price-to-earnings (P/E) ratio divided by the growth rate of its earnings for a specified time period).

Yes, the company's PEG ratio stood at 0.51 times, taking the growth in earnings for the last three years.

The book running lead managers- Edelweiss financial services, IIFL Securities and JM Financials.

Ask Value Research ![]()