Debt-fund investors have turned into a bundle of nerves amid debt defaults, rating downgrades, segregations and, more recently, winding-up of some schemes. In view of these events, investors are now looking for safer alternatives with debt-fund kind of returns but without considerable exposure to the debt markets. From this perspective, arbitrage funds have come up as a substitute. These funds derive their returns from the mispricing between the cash and derivatives market for equities. They also enjoy equity-like taxation. The risk-return payoff of these funds is quite like that of liquid funds. We compare arbitrage funds with liquid funds and tell you whether they are suitable for you.

Returns and assets

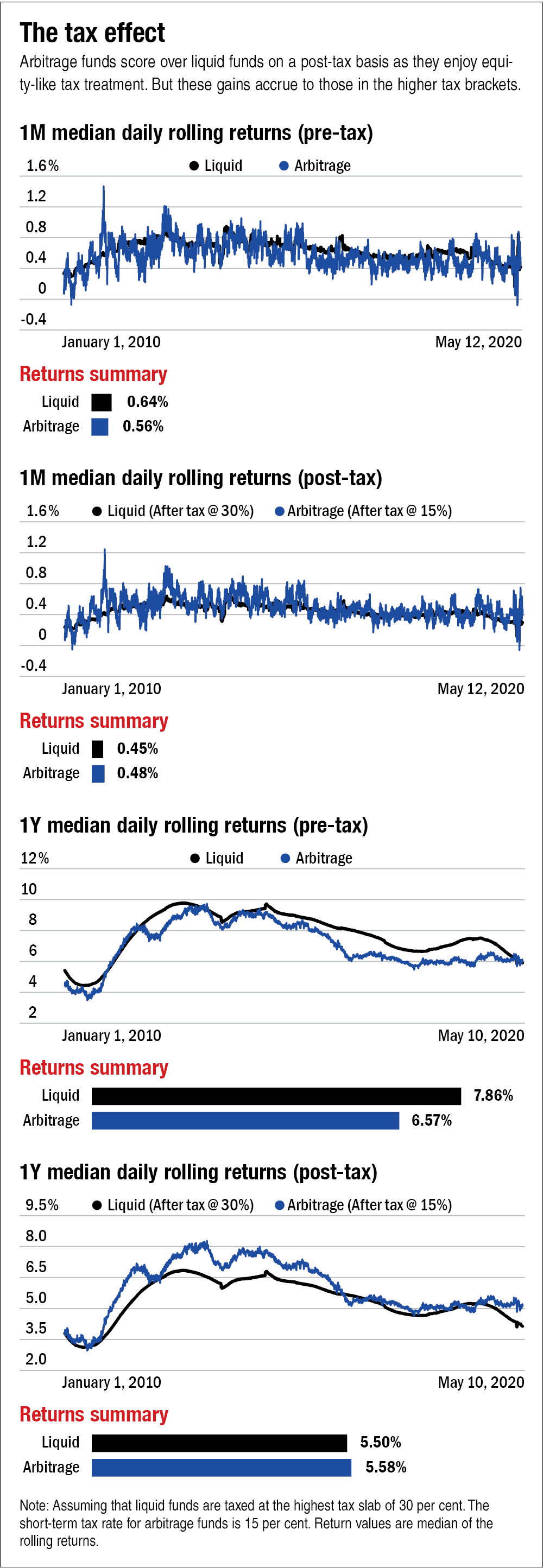

We compared the daily median returns of liquid funds and arbitrage funds rolled over one month and one year. An analysis of the 10-year period highlights that it is the beneficial tax treatment of arbitrage funds that tilts the scale slightly in their favour (see the graph titled 'The tax effect'). But this benefit accrues only to investors in the higher tax brackets. For investors in the lower-tax brackets, the difference vis-à-vis the liquid funds might not be much.

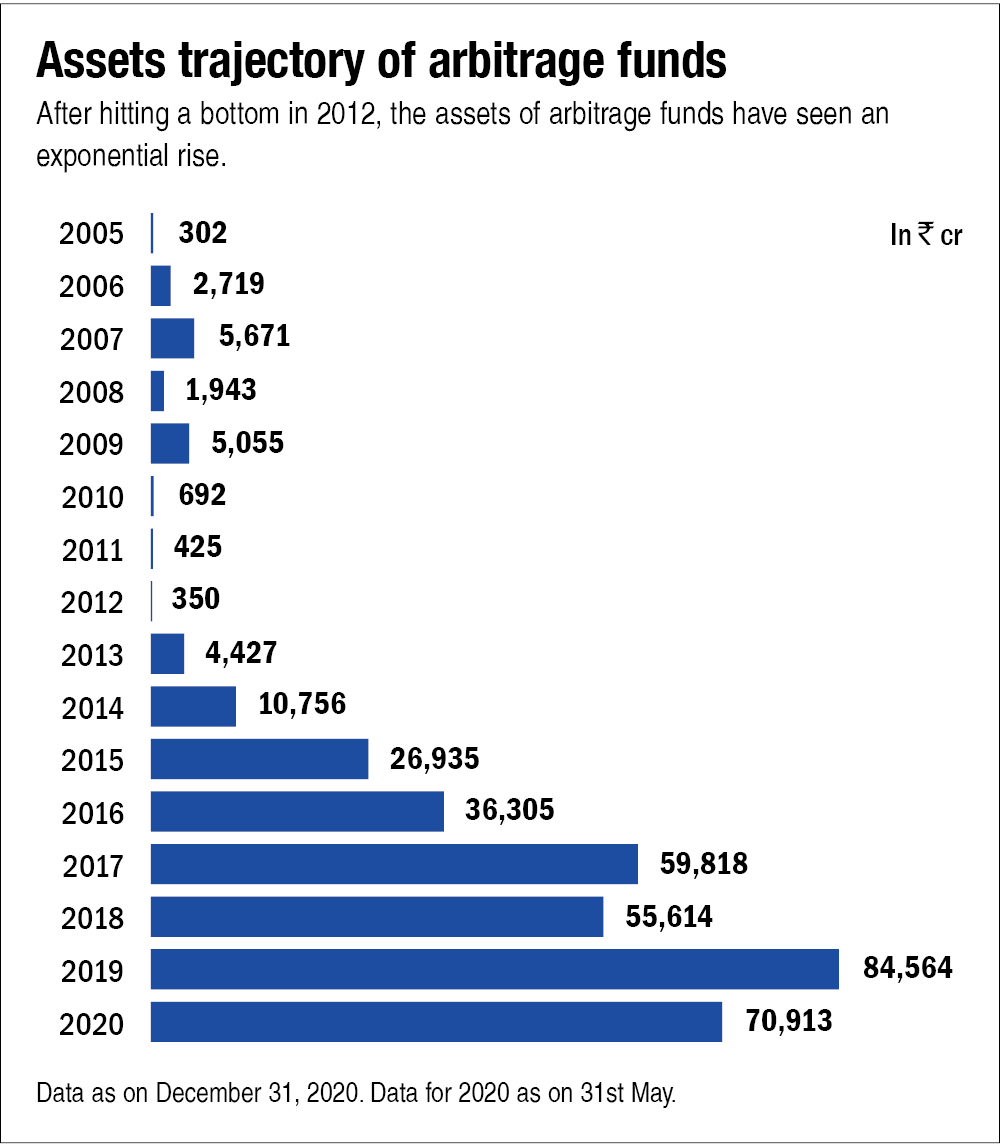

The category has seen steady inflows ever since the government increased the long-term capital-gains tax and the lock-in period for debt funds in 2014 (look at the graph 'Assets trajectory of arbitrage funds).

However, a swelling asset base can make it difficult to find enough arbitrage opportunities and generate meaningful returns. To understand how concerning this is, we asked Hiten Shah, who runs Kotak Equity Arbitrage Fund, the largest arbitrage fund in the industry. "The size of the arbitrage industry is important rather than the size of the individual fund. Till the time the total industry position in cash future arbitrage is around 40-50 per cent of the total open interest, there is no pressure on the spread," says the fund manager. Our estimates suggest that by the end of May, we were already trending beyond the 50 per cent mark. Moreover, it remains to be seen what impact the increase in the upfront margin requirement (from June 1, 2020) has on the market-wide open interest in stock futures.

Volatility, liquidity and cost

As compared to liquid funds, arbitrage funds fluctuate more in shorter time frames (refer back to the graph titled 'The tax effect'). There have been instances of them delivering even negative returns over one month. This happens because arbitrage positions are marked to market on a daily basis. There can also be instances when the spreads turn negative, particularly when markets are highly volatile, shrinking the opportunities available. Such instances occurred recently in March and again in May and early June.

Both arbitrage and liquid funds are reasonably liquid. Liquid funds invest in securities maturing in 91 days or less and generally have high-quality papers. Further, a large amount of corporate money goes in and out of these funds daily. Thus, their portfolios are highly liquid. Even for arbitrage funds, liquidity does not seem to be a problem. According to Hiten Shah, arbitrage funds invest about 65-68 per cent in cash and future arbitrage, 15-20 per cent in FDs and 12-20 per cent in liquid AAA rated papers. It's this 20 per cent of the debt allocation which is used to honour redemptions. Only for redemptions beyond 20 per cent of the AUM, the arbitrage positions have to be squared off.

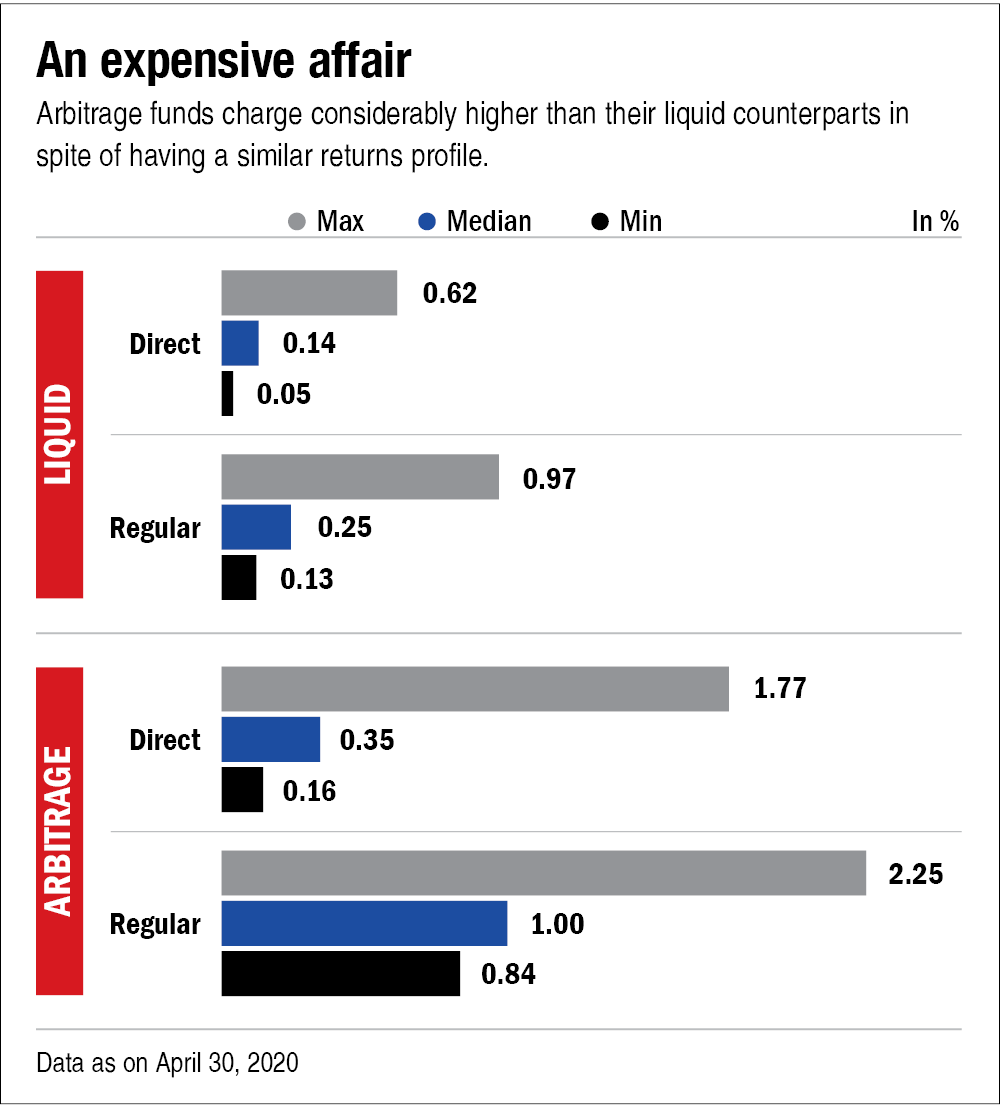

The median expense ratio of the regular plans of arbitrage funds stands at 1 per cent as against 0.25 per cent for liquid funds (see the chart 'An expensive affair'). Also, there is a steep exit load, broadly ranging from 0.25-0.5 per cent, for redemption from arbitrage funds within one month. In the case of liquid funds, it stands at 0.0070 to 0.0045 per cent for redemptions within seven days. Given the higher cost of early withdrawal from arbitrage funds, it makes sense to invest in them at least with a three-month horizon.

From the analysis above, it's clear that the only factor working for arbitrage funds vis-a-vis liquid ones is their favourable taxation but even that is not universal. Hence, for most investors, liquid funds are the better choice.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()