'If I'm already living in the fastest-growing economy in the world, why should I look for investment opportunities elsewhere?' That's a very valid question that many Indian investors ask when you suggest the idea of investing overseas.

In the long run, stock prices and company profits track GDP growth. Today India is the fastest-growing large economy in the world and is expected to remain so for the foreseeable future. The IMF expects Chinese GDP growth, at 6.6 percent in 2018, to slide further to 6.2 per cent next year. But India is expected to sustain a 7.3 per cent plus growth rate, racing ahead at more than twice the rate of the global economy.

But despite India being home to a thriving economy with favourable demographics, it makes sense for Indian equity investors to invest a part of their portfolios overseas. If you're wondering why, here are five good reasons to explore international investing.

1. Wider canvas of opportunities

Can you quickly name some top-of-mind brands on which you spend big money? Chances are that your list will feature Amazon, Flipkart, Microsoft, Netflix, Apple, Samsung, LG, Honda, Swiggy and the like. You'll notice that a majority of these brands are not listed on the Indian stock market. The same goes for Google, Facebook, YouTube, Instagram, and Twitter, among others.

This tells you that though we may be sitting pretty in the fastest-growing large economy in the world, many of the equity investment opportunities arising out of that growth are not available on the Indian exchanges. The global markets, particularly markets like the US, are home to technology and consumer companies of a global stature with the kind of scale, customer base, network effect and competitive moat that very few Indian companies can think of emulating, even over the next decade.

If you want to own such strong companies and brands in your portfolio, which are beneficiaries of emerging consumer trends, you will necessarily need to look to the international markets.

World Bank data tells us that despite its 5,000-odd listed companies, India's market capitalisation, at $2.3 trillion, is still at a fraction of the global market capitalisation, which stands at $79 trillion. Why stick to 3 per cent of the listed universe, when there's another 97 per cent waiting to be explored?

2. More bargains

In financial markets, it is seldom that any good opportunity to multiply money remains a secret for long. With the Indian economy widely acknowledged to be a fast sprinter, foreign portfolio investors, and venture-capital and private-equity firms have been flocking to it for the last many years, bidding up stock valuations. Domestic investors taking a fancy to equities in the last four years has added to the frothy valuations, too.

The net result of all this is that Indian stocks, while promising from a business perspective, are no longer bargains from a valuation perspective.

In recent years, India has consistently figured among the most expensive stock markets in the world. In end-January 2019, while India's Nifty 50 traded at a trailing price-to-earnings (P/E) multiple of 23 times, the Shanghai Composite was at 12 times; the Hang Seng at 11 times; South Korea's KOSPI at 11 times; Taiwan's TAIEX at 13 times; Thailand's SET at 15 times; and Indonesia' Jakarta Composite at 21 times. The Indian bellwethers are steeply priced when compared to developed markets, too, with the US DJIA trading at a P/E of 16 times; Euro Stoxx 50 at 14 times; and Japan's Nikkei at 14 times. The picture is not very different on a forward P/E basis.

Comparing some well-known US-listed consumer names to Indian ones also underlines the valuation gap. While 3M in India trades at a P/E of 73, 3M in the US trades at 20 times. McDonalds in the US trades at 25 times, while Jubilant Foodworks (Domino's) in a similar business is at a lofty 55 times. While a P&G in the US trades at a P/E of 23, P&G in India is at a steep 101.

One is not making the case here that the global companies have far superior prospects compared to these Indian companies. But investing 101 tells us that the higher the valuation at which one buys stocks, the higher the expectations of profit growth from companies. Therefore, stiff valuations make Indian stocks more vulnerable to any disappointment on the earnings or growth front than those in global markets. This is another good reason to look beyond Indian markets for your equity bets.

3. Diversification benefits

Equities are a volatile and whimsical asset class. That's why you are advised to diversify your stock basket in every way you can. A diversified equity fund helps you spread your risks across many stocks and sectors instead of concentrating on a few. A multi-cap equity fund is considered a good core portfolio choice because it diversifies your risks across different market-cap segments. Similarly, investing a part of your portfolio overseas helps you diversify by not depending entirely on the Indian economy or Indian companies to fulfil your long-term goals.

This way, you can shield your portfolio from purely domestic factors that affect your equity returns - foreign investor pull-outs from Indian markets, sudden changes in regulations or government policies that affect domestic companies, bolts from the blue like demonetisation or GST that disrupt the Indian economy, political risks like elections in a specific year.

A global exposure can also help protect your equity portfolio from severe downside when the bears rampage in the Indian market. History tells us that Indian indices soar the most when global stock markets are in a bullish phase. But they also take the biggest battering when the going gets tough for global equities. During the dot-com bubble burst in 2000, the Sensex lost 21 per cent, but the DJIA got away with a 6 per cent loss. The US housing crisis saw the Sensex lose 52 per cent in 2008 but the US market, ironically, managed lower losses of 34 per cent. 2011 was a terrible year for Indian stocks, with the Sensex sinking by 24 per cent, but it was a positive year for the US markets.

India reacts badly to periods of global volatility because they usually deal a double whammy of falling stock prices and a depreciating rupee to foreign investors, prompting them to pull out in a knee-jerk fashion.

That's a third good reason to explore international investing. Investing a part of your portfolio in more mature markets can help smooth out the bumps in your equity portfolio if global risks suddenly rear their head.

4. Gaining from dollar strength

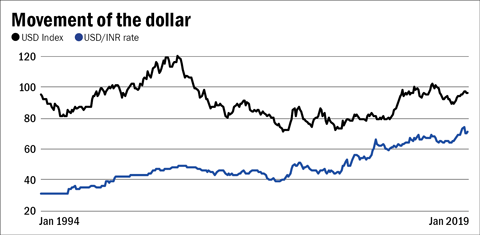

For all the mess that the US economy gets into from time to time, we all know that the US dollar is the uncrowned king of global currencies and the ultimate safe-haven asset for global investors. On this aspect, it has comfortably beaten gold. In fact, every time economists have predicted gloom and doom for the US economy, it has been resilient, with the dollar emerging stronger from the turmoil.

The rupee, on the other hand, has not been so lucky. Every time there's a hint of a global oil-price rise, political upheaval or rising imports in India, the rupee is quick to depreciate against the dollar. India perpetually runs a current account deficit and its inflation rates are always many notches above those of developed economies.

The rupee has consistently headed south against the dollar for the last many decades, irrespective of how the Indian economy has fared. The rupee's 55 percent depreciation against the dollar in the last 25 years would have directly padded up the returns of any Indian investing overseas.

Diversifying into dollar assets also makes sense for an Indian investor because it will steady your portfolio when macro risks are looming large for India, be they from a sky-rocketing oil, global rate hikes or risk-averse FPIs.

Investing in overseas stocks, particularly dollar-denominated ones, helps you convert the challenge of rupee depreciation into an investing opportunity to earn better returns.

5. Dollar commitments

If ordinary folk can look to own dollar assets in their portfolio to add a kicker to their returns, it becomes a necessary bet for affluent investors or HNIs who have dollar expenditure to meet every year. Many Indian families with relatives abroad or children pursuing higher studies overseas have to budget for a dollar outgo every year towards the maintenance of their near and dear. Others may take annual vacations abroad which entail a hefty outgo in foreign exchange. The steadily weakening rupee can cost such folks quite a packet over time, bloating their expenses from year to year.

Owning some dollar assets in your portfolio by investing overseas can help hedge your portfolio against rupee depreciation if you have out-of-pocket expenses denominated in dollars.

Finally, while international investing has many benefits, it can backfire if you do it with short-term returns in mind. Many investors are today rushing into Brazil funds because they had a bumper year in 2018 or buying a US opportunities fund or a Nasdaq 100 ETF just because FAANG (Facebook, Amazon, Apple, Netflix and Google) stocks have blown out the lights in the last three years.

This is a bad idea. As with any other investment, rushing into the international funds just because their past one-year or three-year returns look good can be damaging to your portfolio. Taking a strategic approach to owning international funds is your best bet. Choose your international fund carefully, decide on a pre-set allocation to that fund (say 10 per cent of your equity allocation) and stick to it through thick and thin, with a minimum five-year horizon. As with any equity investments, SIPs are always better than lump-sum investments.

Ask Value Research ![]()