A general insurer safeguards the insured from any uncertainties that arise due to an unforeseen event, such as health problem, accidents and natural calamities. ICICI Lombard and New India Assurance are two general insurers that listed on the Indian exchanges in 2017.

The business model

Unlike life insurers, general insurers do not make money from the net difference between the premiums received and claims paid as in most cases claims are higher than what they receive as premiums. They are highly dependent on investment income generated in the form of dividends, interest, etc.

Key metrics

Key metrics used in the general-insurance industry are as follows:

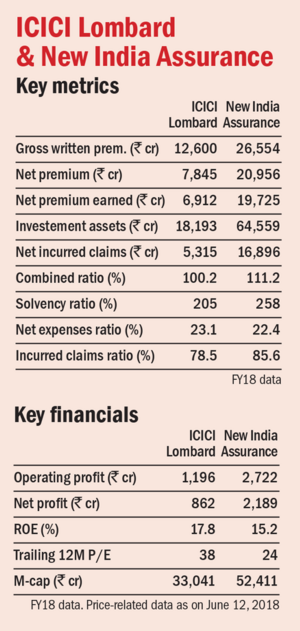

Gross written premium: The total amount received as the premium for the insurance policies issued. The higher the total premium, the better it is.

Net premium: Total premium less the premium 'ceded' to a reinsurer or another insurer plus the premium accepted from another insurer. A general insurer has to buy reinsurance from companies like GIC Re for at least 5 per cent of its policies, as mandated by the insurance regulator, IRDA. This helps in lowering the general insurer's risk. The premium paid for this has to be deducted from the total premium. Also, insurers transfer some of their risk to other insurers and pay premium for it or they can take on some risk from other insurers and get paid.

Net premium earned: Net premium less safety reserves. A higher net premium earned means higher earnings for the insurer.

Net incurred claims: Claims incurred in a specific period after adjusting for those paid by the reinsurer. High incurred claims could lead to underwriting losses.

Combined ratio: How much a general insurer is paying in claims and expenses as compared to the premiums earned. A ratio above 100 per cent means underwriting losses, i.e., the company is paying more in claims and expenses than the premiums it is collecting.

Solvency ratio: A measure used to test the solvency of the insurer in the worst-case scenario, i.e. all the insurance claims materialise at once. The regulator has mandated it to be at least 150 per cent.

Net-expenses ratio: The ratio of operating expenses, including the cost of acquiring new customers, to the net premium earned. A low net-expenses ratio suggests efficiency.

Incurred-claims ratio: The ratio of claims incurred to the net premium earned. Incurred claims are a sum of the claims paid and the claims due during the year. A low incurred-claims ratio is desirable.

This article is part of a series on how to assess new business models.

Ask Value Research ![]()