Income that is not spent is called saving. If you don't spend 10 per cent of your income every month and just keep the cash in your cupboard, then you are saving money. Keeping cash is a simple concept, but by itself, it does a lot of damage to your wealth. The basic reason for that is money doesn't retain its value. Prices rise and what was worth Rs 100 last year is probably worth Rs 5 or 10 or even Rs 20 more this year. Inflation eats away your savings, bit by bit. We all know this, but despite that we fail to incorporate this knowledge into our saving and investment decisions. We all fail to take this into account when we put away money in supposedly safe deposits and such, for long periods of time.

While many may understand compound interest, very few appreciate the decompounding effect of inflation on their money. What compound interest gives, inflation takes away. To put it another way, inflation is effectively the reverse - it's like decompound interest. Since each year's inflation occurs on top of the previous year's inflation, it means that the effect is just like that of compound interest.

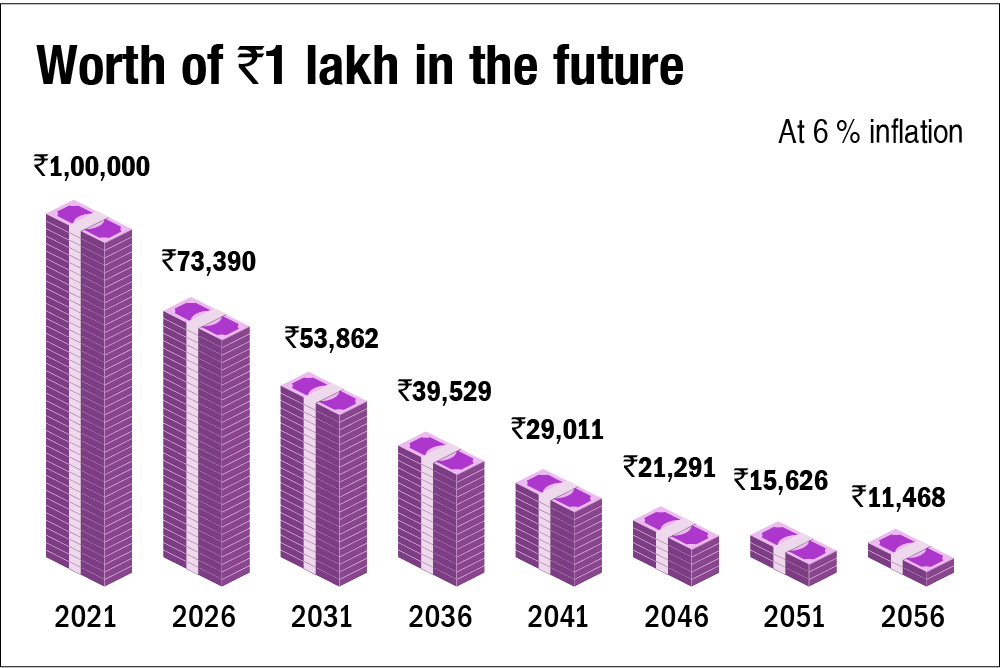

Consider a situation where you invest Rs 1 lakh of your money in a deposit which earns you perhaps 6 per cent a year. At the same time, prices are also generally rising at the rate of 6 per cent a year. In such a situation, your compounding returns will just about keep pace with inflation. The actual amount will increase, but what you can do with it won't. So, for example, over 10 years, your Rs 1 lakh will become Rs 1.79 lakh. However, at the same time, on an average the things you could buy for Rs 1 lakh will also cost Rs 1.79 lakh. In effect, you have not become any richer. The purchasing power of your Rs 1 lakh is still 1 lakh.

We all remember what things used to cost in the past - how someone earning Rs 10,000 a month was comfortably middle class 30 years ago. However, it's very hard for us to extend such extrapolations into the future. People think in nominal terms and the future impact of inflation is awfully hard to internalise. But savers should always adjust for inflation. If today Rs 2 crore sounds like the kind of money you'll want 20 years from now, then you might actually need to have about Rs 6.5 crore, assuming an inflation of 6 per cent. If you work backwards from there, you'll need to save about Rs 1.41 lakh a month if the returns expected are also 6 per cent. If the expected returns are 9 per cent, then you will need to save a lot less - about Rs 1 lakh a month.

Think carefully about this. People who are relying on deposit-type savings which yield very little real rates of return (i.e., above inflation rate), need to save a lot more in order to avoid old-age hardship. All of us who don't have some inherently inflation-adjusted old-age income (like rentable property) need to understand this math and act upon it before it's too late. This may not look urgent - you can always postpone it to another day - but it's definitely more important than whatever else you are planning to do next weekend.

Suggested read:

The inflation monster is destroying your wealth every year!

The power of compounding

This article was originally published on April 12, 2022, and last updated on October 11, 2022.

Ask Value Research ![]()