A wise man once said, ''There is no free lunch on Wall Street.'' This holds true for investing in a mutual fund, too. Like any business that charges you for their services, mutual funds, too charge a fee for managing your money. This includes the fund management fee, agent commissions, registrar fees, and selling and promoting expenses. All this falls into a single basket called total expense ratio that is disclosed on a daily basis and is expressed as an annualised percentage of the fund's net assets.

The expense ratio states how much you pay a fund as a percentage of your investment every year to manage your money. For example, if you invest Rs 10,000 in a fund with an expense ratio of 1.5 per cent, then you are paying the fund Rs 150 a year to manage your money. In other words, if a fund earns 10 per cent and has a 1.5 per cent expense ratio, it would mean an 8.5 per cent return for an investor. Fund NAVs (net asset values) are reported net of fees and expenses. And so if you want to know how much the fund is deducting, the expense ratio can be found under the 'Disclosures' tab on the website of the given asset management company (AMC). Or you could access it on the Value Research website, on the page of the fund. Just search for your fund using the search bar at the top of the page.

Since the expense ratio is charged on a regular basis, a high expense ratio over the long term may significantly eat into your returns as a result of the power of compounding. For example, Rs 1 lakh over 10 years at the rate of 15 per cent will grow to Rs 4.05 lakh. But if we consider an expense ratio of 1.5 per cent, your actual total returns would be Rs 3.55 lakh, nearly 14 per cent less than what it would have been without any expense charge.

Different funds have different expense ratios. But the Securities & Exchange Board of India (SEBI) has stipulated the upper limit that a fund can charge. Equity funds can charge a maximum of 2.25 per cent, whereas a debt fund can charge 2 per cent (annualised) of the daily net assets. The maximum permissible limits for the expense ratio depend on the assets under management (AUM) of the fund. Look at the table below. The largest component of the expense ratio is management and advisory fees. From the management fee an AMC generates profits. Then there are marketing and distribution expenses. All those involved in the operations of a fund like the custodian and auditors also get a share of the pie. Interestingly, brokerage paid by a fund on the purchase and sale of securities is not reflected in the expense ratio. Funds state their buying and selling price after taking the transaction cost into account.

| AUM slab (Rs crore) | Maximum permissible TER for open-ended schemes | |

| Equity-oriented schemes | Other schemes (excluding Index Funds/ETFs and FOFs) | |

| 0-500 | 2.25% | 2.00% |

| 500-750 | 2.00% | 1.75% |

| 750-2000 | 1.75% | 1.50% |

| 2000-5000 | 1.60% | 1.35% |

| 5000-10000 | 1.50% | 1.25% |

| 10000-50000 | TER reduction of 0.05% for every increase of 5,000 crore AUM or part thereof | TER reduction of 0.05% for every increase of 5,000 crore AUM or part thereof |

| More than 50000 | 1.05% | 0.80% |

| Source: SEBI press release | ||

| Type of scheme | Maximum permissible TER |

| Equity-oriented close-ended or interval schemes | 1.25% |

| Other than equity-oriented close-ended or interval schemes | 1.00% |

| Index Funds/Exchange Traded Funds (ETFs) | 1.00% |

| Fund of Funds investing in actively managed equity-oriented schemes | 2.25% |

| Fund of Funds investing in actively managed other than equity-oriented schemes | 2.00% |

| Fund of Funds investing in liquid, index and ETFs | 1.00% |

| Source: SEBI press release | |

Expense ratio especially matters in the case of debt funds. They are usually expected to give a return of around 7-9 per cent. Thus, in a low yield universe, every penny will count. And as expenses are deducted from the fund before calculating the NAV, it is likely to be a major differentiating factor among bond funds where returns vary marginally.

In case of actively managed equity funds, the issue of expenses is more complicated. The wide divergence of returns between 'good' and 'bad' funds makes the expense ratio secondary. But here too, if you find two similar funds, the expense ratio can be a good differentiator. Perhaps, more important is the fact that expenses are charged at all times. Whether a fund generates positive or negative returns, expenses are always there.

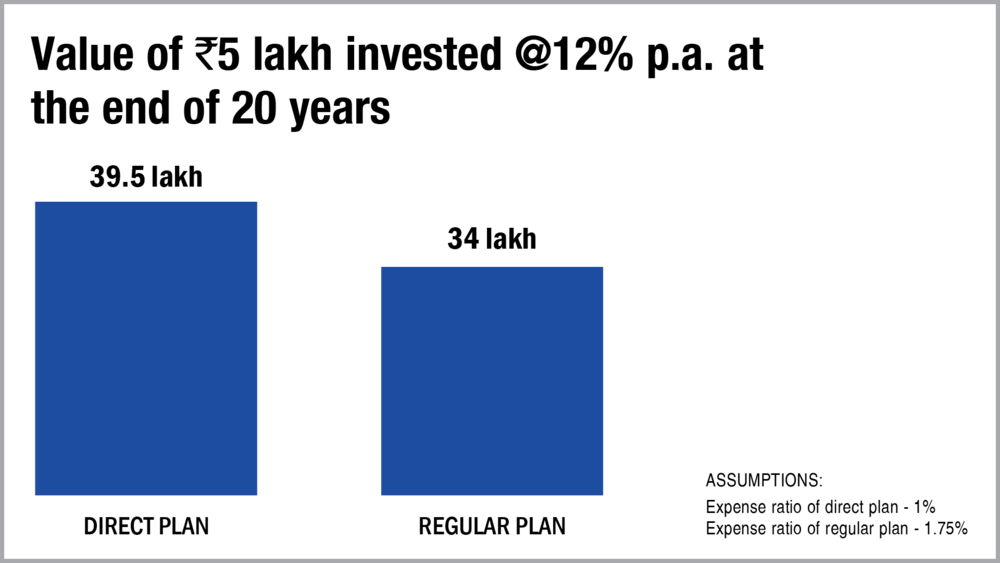

Direct plans have a lower expense ratio than regular plans. This is because in direct plans, the AMC saves on the commission paid to the mutual fund agent in regular plans. If as an investor you are capable of managing your own investments, by staying away from regular plans you may significantly lower your expense ratio and receive higher returns over time. Though the difference between expense ratio of direct and regular plans might not look substantial to you in percentage terms, but the impact on your overall corpus becomes meaningful over a period of time (see the graph).

Before venturing into any fund, the expense ratio is something you want to check. Bear in mind that a lower expense ratio does not necessarily mean that it is a better-managed fund. A good fund is one that delivers good return with minimal expenses.

This article was originally published on March 24, 2021.

Ask Value Research ![]()