Sheela is 42 years old. She works as a professor of zoology. Her husband passed away in an accident ten years ago. She has a daughter who is dependent on her. Unfortunately, her daughter is hearing-impaired.

| Savings & investments | Amount (Rs) |

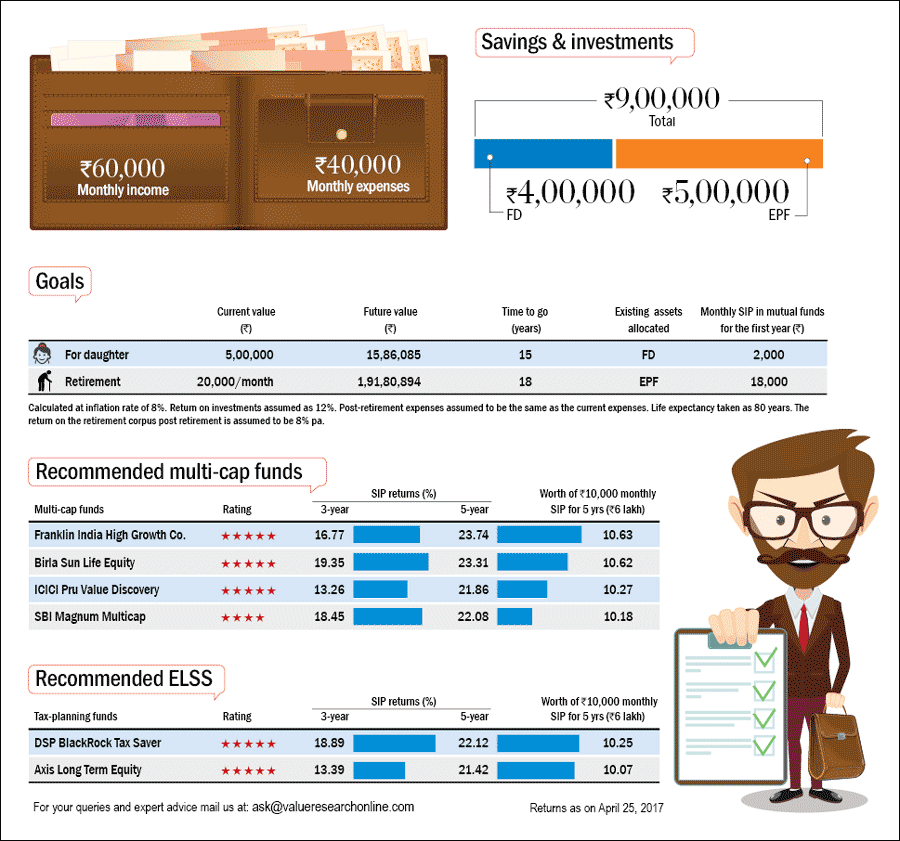

| MFs | 95000 |

| FD | 100000 |

| EPF | 200000 |

| Total | 395000 |

| Monthly income | 60000 |

| Monthly expenses | 40000 |

| Insurance | Nil |

| Liabilities | Nil |

Sheela wants us to develop a financial plan for her that could help her fulfil her goals of retirement and accumulating sufficient corpus for her daughter. Here's our plan for her.

Emergency fund

Sheela should park Rs 2,40,000 (six months' expenses) for any unforeseen contingencies. The amount in her FD can be earmarked as her emergency fund.

Health insurance

Any unforeseen medical emergencies can derail one's financial prospects. Sheela must get health insurance for herself and for her daughter. A medical check-up may be required when she buys a health plan.

Life insurance

Sheels's daughter is financially dependant on her, so it is important for her to buy life insurance. She can buy term insurance worth Rs 1-2 crore. This will cost her Rs 10,000-12,000 annually.

Investment portfolio

Sheela already contributes to the Employees' Provident Fund, which comes under Section 80C and provides income-tax deduction. Since the total investment allowed under Section 80C is Rs 1.5 lakh, she can invest the balance in a tax-saving fund. Our recommended tax-saving funds are given on the adjacent page. She can invest in any one of them.

Sheela has 18 years left for her retirement, so she can easily reach her retirement goal and build a seperate kitty for her daughter to attend to her medical needs or education.

She has a surplus of Rs 20,000 per month. If she invests in equity mutual funds for the next 18 years, she can accumulate around Rs 1.91 crore (assuming a 12 per cent return). See the adjacent page for a list of our recommended multi-cap funds. Sheela can pick any two of the funds listed

in the table.

This article was originally published on April 27, 2017.

Ask Value Research ![]()