Nikunj is 29-year-old single man, working in a PSU at Ranchi. He wants to buy a house worth ₹50 lakh with his savings and bank loan. He doesn't know how much insurance is adequate for him and he want to save for his travel plans. He wants us to help him plan his investments with a moderate risk.

| Income | Amount (₹) |

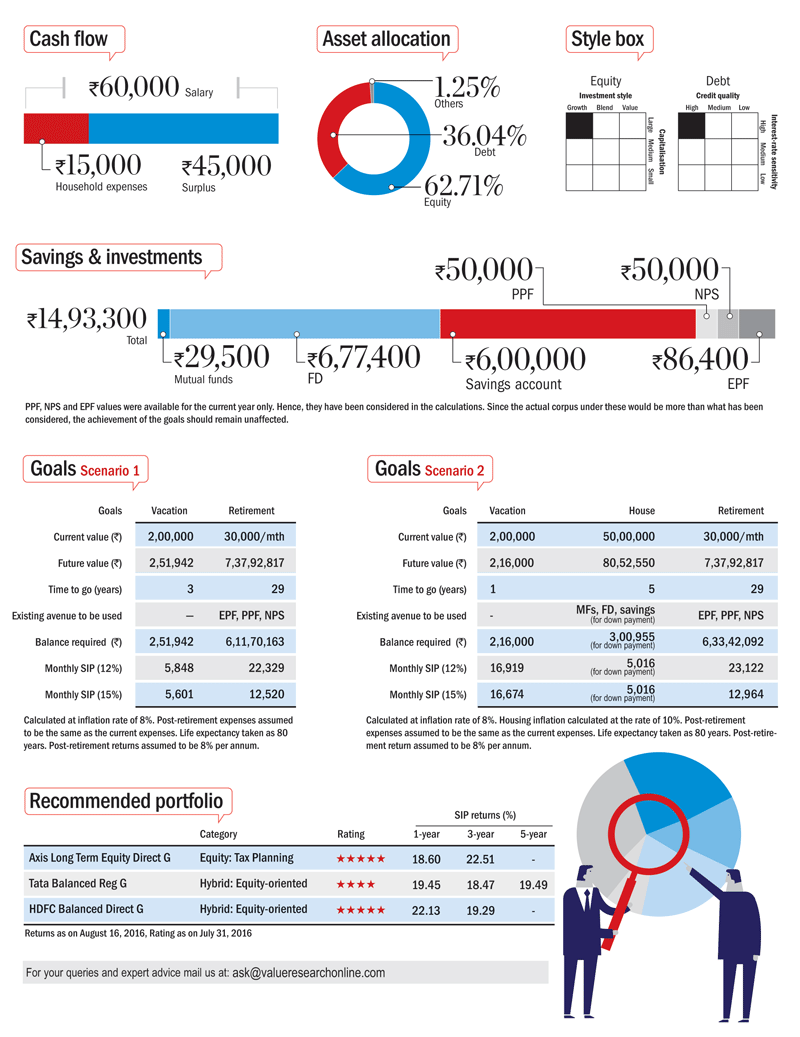

| Salary (Monthly) | 60,000 |

| Expenses (Monthly) | 15,000 |

| Savings | |

| Mutual Funds | 29,500 |

| Fixed Deposits | 6,77,400 |

| Savings account | 6,00,000 |

| PPF | 50,000 |

| NPS | 50,000 |

| EPF | 86,400 |

| Total | 14,93,300 |

| Insurance Premia | |

| Life Insurance Premium (endowment) | 25,000 |

| Health Insurance (Monthly) | 0 |

| Loans/Liabilities | 0 |

What he has (Cash Flow)

- Monthly income: ₹60,000

What he wants (Goals)

- A house worth ₹50 lakhs

- Money for travel plans (annually 1 long distance and 2-3 short trips)

What he should do?

Dealing with emergency

Nikunj can earmark ₹45,000 (three months' expenses) from his savings account for an emergency fund. He should opt for the sweep-in facility to earn higher returns on this corpus.

Health is wealth

Nikunj has a medical cover from his employer. He should also buy a personal health cover. It can be handy if the employer-provided group-insurance limit gets exhausted or he is in the midst of switching jobs. He can buy Apollo Munich Easy Health Standard for a sum assured of ₹5 lakh. The annual premium would range from ₹6,300 to ₹7,000.

Life insurance

Nikunj has a traditional endowment plan with a sum assured of ₹5 lakh. He should surrender it as it is unlikely to offer returns that can beat inflation. The premium is also quite high.

Assuming that his parents are financially dependent on him, he needs a life cover of ₹80 lakh to ₹1 crore. He can buy an online term plan worth ₹1 crore from Max Life at an annual premium of ₹7,500. When he gets married and has a dependent spouse, he will need to reevaluate his insurance requirement.

Growing money

Nikunj wants to buy a house worth ₹50 lakh. We have assumed two scenarios for this.

Scenario 1: He is staying in rented accommodation.

In this case, he can use the surplus in his savings account and the fixed deposit for the down payment (₹10 lakh). He can get the rest of the amount (₹40 lakh) financed from a bank. He should opt for a home loan with the facility of accelerated prepayment options.

Though saving for retirement is as much important as saving for other goals, a major portion of his surplus will go towards the home-loan EMI. Hence, he will not be able to fulfil his vacation and retirement goals.

Scenario 2: He is staying with his parents or at employer-provided accommodation.

In this case, he should wait till he gathers enough funds for his home purchase. We have postponed his home-purchase goal by five years. For this, he should invest his FD and savings-account surplus in mutual funds. Assuming a 12 percent return in five years, he can easily accumulate more than 30 per cent of the house value for the down payment. For the balance, he can take a home loan.

Nikunj has invested in several funds. In order to ensure proper diversification and keep things simple, two-three funds are enough. He can keep the two balanced funds and the tax-saving fund and exit from the rest. The balanced funds will provide him the right debt-equity divide. The tax-saving fund will help him save taxes. He should avoid investing in a sectoral fund as it provides limited diversification.

Though the PPF has guaranteed returns and tax benefits, the returns are low. He can continue with the minimum investment to keep the account active and direct his tax-saving investments to the ELSS. He can continue with the NPS, since the tax-saving allowance for the NPS investment cannot be used in any other way.

This article was originally published on August 18, 2016.

Ask Value Research ![]()