Vinayak Pathak/AI-Generated Image

Vinayak Pathak/AI-Generated Image

Summary: A company whose value exceeds half of India’s economy offers an important lesson in valuation. More so, when you look at the actual business underneath. Elon Musk’s control and capital burn mark the difference between a great business and a great investment.

On Friday morning in Texas, the market met a story large enough to overwhelm arithmetic. SpaceX began trading on Nasdaq. By the close, the company was worth a little over $2 trillion.

Bring its current market-cap number home. At roughly Rs 94 to the dollar, $2.5 trillion is about Rs 236 lakh crore. That is about 60 per cent of India's annual GDP and close to 42 per cent of the value of all BSE-listed companies. One company, built over 24 years, was being priced at a scale Indian investors usually reserve for countries, not businesses.

A company worth half India's GDP

| Item | Value (Rs lakh crore) |

|---|---|

| Total BSE-listed market value | 472 |

| India nominal GDP, FY26 | 357 |

| SpaceX current value | 236 |

The achievement is extraordinary. SpaceX made rocket reuse routine, built Starlink into the world's largest satellite-internet network, and gave Elon Musk the rare public-market moment that seems to turn technology, myth and money into one trade. But admiration is not analysis. A great company can still be a poor investment if the price asks too much of the future.

That makes this listing useful even for investors who will never buy the stock. It is a clean test of temperament. Can we admire the engineering and still question the valuation? Can we separate the company from the trade?

What the business is about

Strip away the launch-day noise and SpaceX is three businesses.

The first is launch. SpaceX designs rockets, flies them, lands the boosters and flies them again. That sentence now sounds familiar, which hides how radical it once was. For decades, rockets were used once and thrown away. SpaceX changed that.

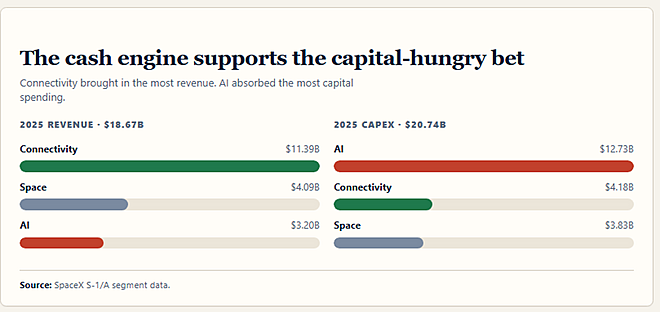

The second is Starlink, or the internet connectivity business. It works through a massive constellation of satellites that offer high-speed internet broadband. This is where economics becomes interesting. In 2025, SpaceX reported revenue of about $18.67 billion. Connectivity accounted for about $11.39 billion of that.

The third is artificial intelligence. Musk's AI ambitions now sit inside the same public company. The AI segment had about $3.2 billion of revenue in 2025, but it also carried heavy losses and the largest capital-spending burden.

That split matters. SpaceX is not one clean business. It is a cash-generating communications network, a capital-heavy space-infrastructure company and a speculative AI platform rolled into one stock.

The important question for investors to assess is: which part earns, which part spends, and which part is still only a promise?

What makes the business work

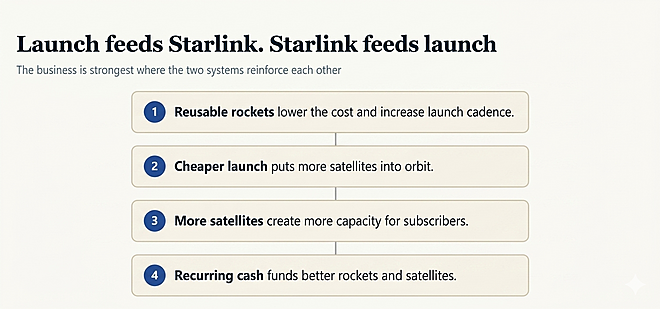

The satellite network, or Starlink, is the most attractive part of the business, which is reinforced by its rocket enterprise.

A rocket launch is a spectacle: fire, smoke, countdown, applause. Starlink is quieter: a dish on a roof, a ship at sea, a military unit, a monthly bill. That is where SpaceX changed from an aerospace contractor into an infrastructure company.

SpaceX follows a simple loop. Reusable rockets lower the cost of reaching orbit. Cheap launch lets it place more satellites faster than rivals. More satellites create more capacity. More capacity allows more subscribers. More subscribers produce recurring revenue. That funds the next generation of rockets and satellites.

A rival must solve the whole chain, not one link. It must launch cheaply, deploy a satellite constellation, win customers, keep replacing satellites and survive the capital cycle. That is why the moat is difficult to replicate. It is made of metal, spectrum, ground stations, customers and thousands of satellites overhead.

This is also why the market treats Starlink differently from a launch contract. A launch is lumpy. But Starlink’s subscription-like revenue repeats. Lumpy revenue must be won again and again. Recurring revenue gives a company time, visibility and a base from which the next investment can be made.

The price asks for a lot

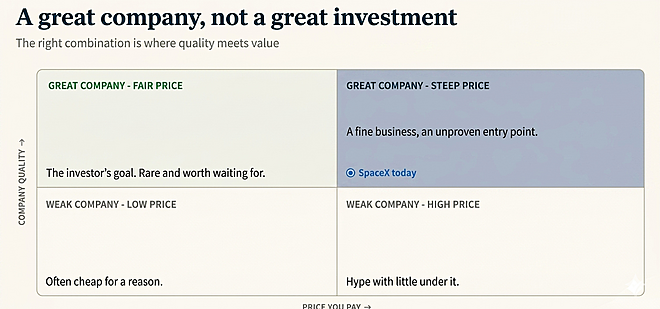

A strong business does not settle the investment question. It only begins it.

SpaceX came to market at a valuation most companies never see even after decades of public compounding. The problem is that the price already assumes a great deal of the future.

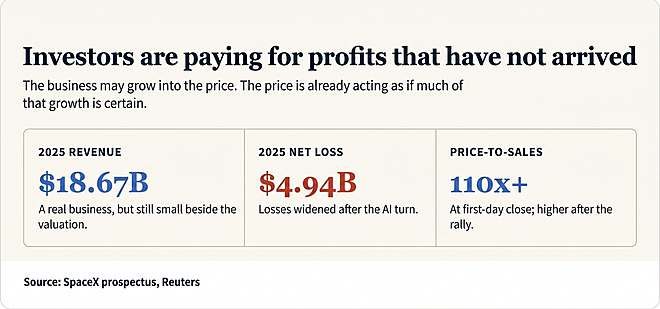

At the first-day close, the market value was more than 110 times the 2025 revenue of $18.67 billion. The company made a net loss of about $4.94 billion.

After the June 16 rally, the multiple was above 140 times. That is not a valuation based on today's profits (which don’t exist yet) but a claim on a future in which Starlink becomes a global utility, Starship works commercially, AI becomes a serious business, and capital spending finally turns into durable profit.

That future may arrive. But it may have hiccups. Regulators can slow satellite deployments. Governments can favour national champions. AI can consume capital faster than it creates returns. And when a stock begins public life at a heroic valuation, even good news can be too small to satisfy it.

This is the old market mistake in modern clothes. Investors first fall in love with the company, then use the company's excellence to excuse any price.

The right question is not whether SpaceX can be larger in 10 years. It probably can. The question is whether today's buyer is being paid enough for the execution risk, governance risk and valuation risk that stand between the company and that future.

Shareholders own the stock, not the control

A public market normally gives a shareholder three rights: to vote, to sue and to sell. SpaceX gives public shareholders economic exposure, but each right is thinner than it first appears.

Start with the vote. Public investors buy low-vote shares. Musk and insiders hold high-vote shares. Musk controls nearly 85 per cent of the voting power while owning a smaller 42 per cent stake in the company. Public shareholders may own the stock, but they do not control the company.

The second right is the right to sue. The filing narrows the legal road available to shareholders by steering disputes through specific forums and procedures. The rights exist, but they are fenced.

The third right is the right to sell. This is the most practical right of all. But a small float, which SpaceX has, can lift the stock quickly when demand is strong and make exits painful when the mood turns.

Indian investors know promoter control well, but this structure goes further than the ordinary listed-company bargain they are used to. A shareholder can enjoy the upside, but cannot easily discipline the promoter, block a strategic turn or demand a different board. That is not a reason to avoid the stock by itself. It is a reason to demand a higher margin of safety.

The asset and the risk are the same man

There is no way to analyse SpaceX without analysing Elon Musk. That is not celebrity gossip but plain investment analysis.

Musk is the reason SpaceX exists in its present form. He pushed it through early failures, backed reusability when the industry doubted it, and forced an engineering culture that moved faster than the old aerospace world. Without that temperament, SpaceX may have become another contractor.

The same temperament is also the risk. Investors are not buying a quiet committee culture. They are buying a founder-led system built around one person's judgment, impatience and appetite for risk. That can create miracles. It can also create abrupt strategy shifts, stretched spending and decisions ordinary shareholders cannot stop.

The AI turn shows the bargain. Investors who wanted a space-and-connectivity company now own a space-connectivity-AI company. It may prove brilliant. It also makes the company harder to value. The useful question is not whether Musk is admirable or erratic. He is plainly both productive and unpredictable. The useful question is whether the price gives investors room for that range of outcomes. At $2 trillion-plus, the room is not large.

So what should an investor do?

For most Indian investors, the answer is: admire it, study it, and probably do not chase it.

SpaceX is not a core holding for a normal household portfolio. It is too hard to value, too dependent on one person, too expensive on present numbers and too far outside the ordinary needs of long-term financial planning. Access, where available through overseas-investment routes, is not the same as suitability.

At most, it belongs in the satellite corner of a portfolio. Money you can afford to be wrong about. The better use of SpaceX is educational. It is a live case study in the hardest distinction in investing: company quality versus investment quality.

That distinction applies far beyond this IPO. It applies to every hot listing, every fashionable small-cap, every business with a charismatic founder and every sector that promises to reshape the future. The story may be true and the stock may still be priced for perfection.

The public investor today faces a different bargain. The rockets have already landed. Starlink has already scaled. The founder premium is already in the price. The future may still be large, but the entry point is no longer obscure.

That is why the wisest sentence about SpaceX is also the simplest. A great company is not automatically a great investment. The difference is the price. It always was.

Don’t pay any price for a great story

The lesson from SpaceX is simple: even the most exciting business can be a poor investment if the price is wrong. Value Research Stock Advisor helps you focus on the other side of the equation: good businesses bought at sensible prices. Explore our stock recommendations and build a portfolio where quality does not come at any price.

Ask Value Research ![]()