Summary: Every crisis feels like the one that's finally different. It almost never is. Here's the framework for when headlines are screaming and your instincts are telling you to do exactly the wrong thing.

February 24, 2022. Russia invades Ukraine. Markets fall 5 per cent in a day. Rahul, a disciplined investor, watches his portfolio show a Rs 12 lakh loss. Messages flood in: “Sell everything”, “Move to cash”, “World War 3 is starting” His brother-in-law sells half his equity holdings and urges him to follow. It feels different this time—a geopolitical shock, not a routine market correction.

Rahul instead checks his allocation and rebalances to the target allocation. Eighteen months later, his portfolio is up over 25 per cent. His brother-in-law is still sitting in cash, waiting for “clarity.”

The headlines kept screaming. The disciplined portfolio stopped listening.

The illusion of ‘this time is different’

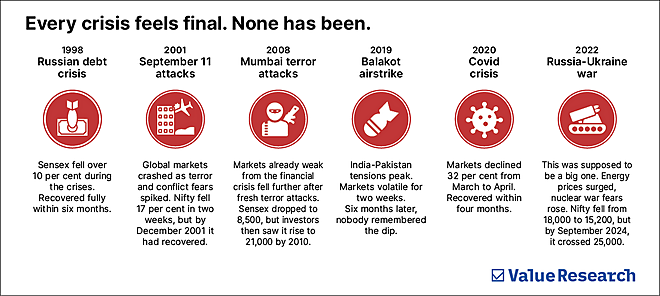

Every geopolitical crisis feels uniquely terrifying when we are living through it. Yet market history shows they rarely damage long-term returns. Markets recovered far faster than the fear suggested. Each crisis felt existential in real time, but ended up being a temporary speed breaker, as illustrated in the timeline mapped below.

No harm to long-term returns

These are the things markets care most about: corporate earnings, interest rates and valuations. Geopolitical events rarely change these fundamentals permanently.

Take the Russia-Ukraine war. Energy prices spiked. Supply chains were disrupted. Inflation accelerated. These created short-term volatility. But did they alter the long-term earnings trajectory of Indian companies?

ICICI Bank still lends money. Asian Paints still sells paint. Titan still sells jewellery. The war was terrible, but it did not stop Indians from banking, buying homes or getting married.

Corporate India adapted, found alternative suppliers and customers, and kept growing. Within a year, most companies’ earnings had recovered or exceeded pre-war levels.

Contrast this with the 2008 financial crisis. That was not geopolitical but structural. Banking systems froze, credit dried up, and companies struggled to function. Recovery took years because the damage was economic, not just sentiment-driven.

Geopolitical shocks are usually sentiment shocks. They create fear, volatility and dramatic headlines. But they rarely break the underlying economic machinery.

The deadly temptation to time geopolitical events

When a crisis hits, our instincts scream at us to act. Doing nothing feels irresponsible. Ironically, this is where wealth often gets destroyed, not in the crisis itself but in the panicked response. Here is what typically happens:

Stage 1: Panic sell. Markets crash and you sell because “it will get worse.”

Stage 2: Frozen wait. Markets stay volatile. You wait for “clarity” before entering again. Clarity rarely comes quickly.

Stage 3: Painful miss. Markets recover 20 or 30 per cent from the bottom. You are still in cash and it now feels too expensive to re-enter. Investors who sell during geopolitical shocks usually underperform those who stay disciplined. Not because they choose poor investments but because they exit at the wrong time or remain on the sidelines.

The rebalancing advantage

Here is the counterintuitive truth. Geopolitical crises can become opportunities for disciplined investors. When markets fall, equity as a share of your portfolio drops. Rebalancing forces you to buy low. Not because you are brave, but because you are systematic.

The greatest risk during geopolitical volatility is not that markets fall. It is that you sell low and turn temporary losses into permanent ones by missing the recovery.

The framework for handling geopolitical volatility

Before crisis: Set your system

1. Define your asset allocation based on goals and risk capacity, not geopolitical forecasts.

2. Set rebalancing bands. A range of ±5 per cent is common.

During crisis: Execute your system

1. Reduce news consumption. Headlines trigger emotion, not investment insight.

2. Check allocation, not daily prices. Once a month is enough. Did any asset class fall below your rebalancing band? Then act. If not, do nothing.

3. Rebalance systematically. Use new money to buy underweight assets.

After crisis: Review, don’t regret

1. Evaluate the process, not just the outcome.

2. Avoid hindsight bias. Timing one crisis correctly does not mean you will time the next.

But what if this time really is different?

This question appears in every crisis. What if this war escalates? What if the global system breaks? Here is the honest answer. If the world truly collapses, portfolio allocation will not matter. Food, water and safety will.

But the probability is extremely small. In three decades of post-liberalisation markets, India has seen wars, terror attacks, political instability and global shocks. None permanently broke the system.

The framework summary

Do: Stick to your asset allocation, rebalance if allocations drift, reduce news noise, and focus on long-term fundamentals.

Don’t: Panic sell, try to time the crisis resolution, assume ‘this time is different’, or let headlines override your system.

The world will always feel dangerous. That is precisely when your portfolio allocation should feel boring.

Also read: A temperature check

Ask Value Research ![]()