My friend Ankit was buzzing with excitement when we met for tea.

"Fifteen per cent!" he announced before I'd even taken my first sip. "My portfolio returned 15 per cent last year."

I nodded, genuinely impressed. The markets had been good, but he'd clearly done better than average.

"That's fantastic," I said. "How much are you putting away each month?"

His enthusiasm dimmed a bit. "Uh, about 5 per cent of my salary right now."

And there it was. The fundamental misunderstanding that I keep seeing, even among financially savvy people.

Chasing returns vs building wealth

"Isn't investing all about getting the highest returns?" Ankit asked.

A lot of people think that way. It's understandable—a 12 per cent return feels objectively better than an 8 per cent return. Who wouldn't want more?

But here's the thing—your savings rate, or the percentage of your income that you save to invest, is what really builds wealth.

"Returns go up and down," I explained. "One year, the market gives you 15 per cent; the next, it wipes out half your gains. If you're only saving 5 per cent of your income, even a 15 per cent return won't make you wealthy fast enough. But if you're saving more, even with modest returns, your wealth grows rapidly."

Ankit leaned in, intrigued. "Okay, but how much difference does it really make?"

Why savings rate beats high returns

I showed him a quick comparison on my phone:

It is not about how much returns you earn

It is about how much you save

| Person A | Person B | |

|---|---|---|

| Monthly income | Rs 1 lakh | Rs 1 lakh |

| Savings rate | 5% (Rs 5,000) | 25% (Rs 25,000) |

| Annual investment returns | 15% | 9% |

| Corpus after 25 years | Rs 1.38 crore | Rs 2.66 crore |

Despite the lower return, Person B—who saved more—ended up with nearly double the wealth.

Ankit's eyes widened. "So, saving more beats chasing high returns?"

"Exactly," I nodded. "The more you save, the less you need to rely on market performance to build wealth."

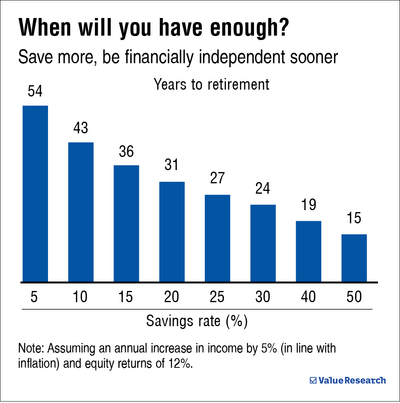

How savings rate affects retirement

Here's a rough idea of how your savings rate affects your time to retire:

-

Save 10 per cent → Retire in 40+ years

-

Save 30 per cent → Retire in 24 years

- Save 50 per cent → Retire in 15 years

Ankit was flabbergasted. "So if I save 10 per cent of my salary, I have to work for over 40 years!"

I smiled. "Which is why you save more. The higher the savings rate, the earlier you can hang up your boots."

Final thought

This isn't to say investment returns don't matter. They do—especially over long periods. The difference between 9 per cent and 12 per cent returns over 30 years is huge.

But here's the key takeaway: focusing on savings rate early on makes a bigger difference than chasing high returns. And unlike returns, your savings rate is something you can control.

So, instead of stressing over the next hot stock or fund , focus on saving more. That's what really builds wealth.

Also read: The five laws of stupid investing

This article was originally published on April 02, 2025.

Ask Value Research ![]()