AI-generated image

AI-generated image

Gold has surged a remarkable 20 per cent in the last 12 months. As a result, many traditional jewellery companies have seen their share prices soar. However, not all have enjoyed such fortunes.

Take Vaibhav Global, for instance. Despite investments from prominent figures like Vijay Kedia and Ashish Kacholia, this company's returns have lagged behind the broader market over the last 10 years.

No shine for Vaibhav Global

Comparing six-month returns of major jewellery companies

| Name | 6M return (%) |

|---|---|

| Kalyan Jewellers India | 22 |

| Titan | 1 |

| PC Jewellers | 66 |

| Vaibhav Global | -12 |

| SBI Gold ETF | 21 |

| *Return calculated as of May 10, 2024 | |

This intrigued us and made us delve deeper into its performance history. But first, let us understand what Vaibhav Global is all about.

Formerly known as Vaibhav Gems, Vaibhav Global is a multinational electronic retailer and fashion jewellery and lifestyle accessories manufacturer. It sells its products through its home shopping channels, Shop LC in the United States and TJC in the United Kingdom.

Early slump and recovery

Once a traditional brick-and-mortar jewellery retailer, Vaibhav Global saw a massive downturn in its business during the 2008 financial crisis. Its revenue dropped by 33 per cent annually in just two years since 2008.

Seeing this plunge, the company shifted its focus towards artificial jewellery. It started selling discounted artificial jewellery (manufactured in India and China) priced between $20 and $30 in the premium markets of the US and UK. This strategic shift proved successful, and the company saw its revenue grow by 40 per cent annually from 2010 to 2014.

Vaibhav Global also optimised its sales strategy by harnessing the power of TV channels. The company appealed to its audience by featuring popular hosts and captivating content, making TV sales the largest revenue segment at 61 per cent as of the nine months ending December 2023.

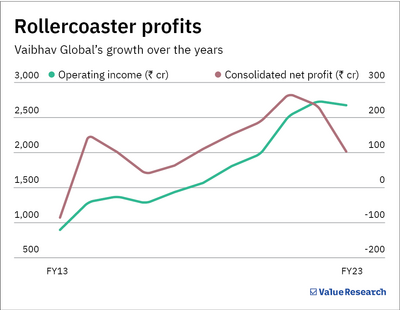

Stagnant performance

However, the initial success between 2010-14 hit a plateau. Since FY14, the company reported only an 8 per cent increase in revenue and a 4 per cent annual decline in profit after tax (PAT) over the last nine years.

Several factors have stifled its growth:

-

Underestimating competition:

Vaibhav Global aimed to undercut major industry players like QVC and HSN with lower prices and vertical integration. However, these competitors fought back with unexpected discounts and attractive payment plans. QVC's acquisition of HSN for $4.2 billion solidified its top position in video commerce.

- Changing industry dynamics: A study by Liechtmen Research points out the declining trend in subscriptions for pay-TV media. This decline in traditional TV subscriptions and the growing preference for online shopping platforms like Amazon is troubling since the company still relies on TV as its main source of revenue.

Strategies for growth

To combat the stagnant performance and adapt to the evolving market, Vaibhav Global has employed several strategies:

-

Geographical expansion:

It has expanded into new markets, including Germany, and is planning to enter Japan. This strategy has resulted in its topline growing by 23 per cent YoY in Q3 FY24.

- Product diversification: Vaibhav Global has introduced lifestyle products and collaborated with third-party players. However, since the company does not want to rely entirely on third-party offerings, it has capped the revenue contribution from such players at 20-30 per cent.

Conclusion

The company's initiatives to foster growth are promising. The management appears optimistic, with a revenue growth projection of 13-15 per cent for FY24 and even higher for FY25. However, its past stagnant performance does not align with this optimistic projection. Further, the challenges confronting growth cannot be ignored. Also, valuations are a concern. It is currently trading at a high P/E of 48.5.

Investors are advised to exercise caution. The market offers several other promising opportunities with stronger fundamentals and more robust growth prospects.

Also read: This pharma stock soared 2x in one year. Is there still time to invest?

Ask Value Research ![]()