On buying a liquid fund, the tax status changes from "Income from mutual funds" to "Interest from fixed deposit income". So in the short run you pay the gains as per "your tax slab" and in the long run you pay tax @10 per cent. So should I take the "dividend reinvestment" option and not the "payout or growth" options to make the most of it because of dividend distribution tax?

-Aseem Arora

The tax treatment in the mutual fund is categorised on the basis of:

i) Equity and Debt funds

ii) Long term and Short term

iii) Dividend and Capital Income

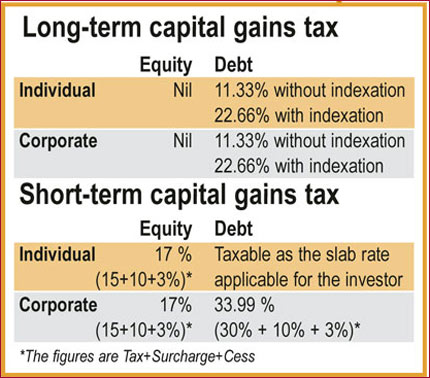

Equity, debt & the tax impact

Equity oriented funds are those funds where more than 65 per cent of the corpus is invested in stocks of Indian companies. Debt funds are those which invest more than 65 per cent in the debt market. Now let's say you hold the units of an equity scheme for more than a year, in that case you are eligible for long-term capital gains, which is zero. In other words, you pay no tax. But if you sell the units within a year, you have to pay short-term capital gains.

In the case of debt funds, if you sell the units after a year, you will have to pay a long-term capital gains tax, either with or without indexation, whichever is lower. Indexation is used to calculate tax when inflation is taken into account. This is good because it reduces the amount of capital gain and subsequently, the amount you end up paying as tax. If you sell the units within a year, the short-term capital gain will be clubbed with the income of the individual investor, to be taxed as per the prevailing slab system

Dividend distribution tax

The dividend distribution tax (DDT) is a tax payable by debt oriented mutual funds. This DDT is paid before dividend is distributed to the unit holders. Equity based schemes are free from dividend distribution tax. Even though dividend is tax free in the hands of the investors, the NAV of the fund falls more than the dividend declared. This is due to the fact that the DDT paid by the mutual fund is deducted from the dividend itself.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Dividend reinvestment or payout

As far as the growth option is concerned, there is no dividend income and the investor has to pay only short-term or long-term capital gain, depending on how long the units are held.

In a debt or liquid fund, DDT is levied on dividend reinvestment and payout options. This is apart from the short-term or long-term capital gains tax.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

The Re-investment option is a clear winner over the growth option. You have rightly suggested choosing the dividend re-investment option over the growth one, as dividend distribution tax acts as a concession in the re-investment option.

This article was originally published on July 15, 2008.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()