Efficient capital allocation is the hallmark of a multibagger. And return on capital employed (ROCE) is a useful metric to gauge a company's efficiency.

But it can be taken a step further.

Enter incremental ROCE. In incremental ROCE, instead of calculating the returns on the entire capital available (shareholders' equity + debt), we calculate the returns on the capital that has been reinvested into the company over a given period.

Here's an example.

Suppose company ABC had total capital of Rs 1,000 crore available in FY15 and generated Rs 100 crore worth of operating profit using that. Hence, its ROCE was 10 per cent (Rs 100 crore / Rs 1,000 crore).

However, by FY20, its total capital had increased to Rs 2,000 crore, and it earned Rs 250 crore as operating profit.

From the above, you can calculate incremental ROCE as follows:

Incremental ROCE = Change in operating profit / Change in capital employed

= (Rs 250 crore - Rs 100 crore) / (Rs 2,000 crore - Rs 1,000 crore)

= 15 per cent

What it means is that, from FY15 to FY20, the company generated higher returns on the reinvested capital than it did in FY15. Simply put, ABC improved its capital efficiency.

Why use incremental ROCE

Incremental ROCE provides a more holistic take on a company's capital efficiency. It brings the focus back to how efficiently a company is using its earning to generate more earnings, which, as we mentioned before, is crucial to building shareholder wealth.

Even the legendary Warren Buffett has highlighted the importance of incremental ROCE. In his annual letter to Berkshire Hathaway shareholders in 1992, he said, "Leaving the question of price aside, the best business to own is one that over an extended period can employ large amounts of incremental capital at very high rates of return."

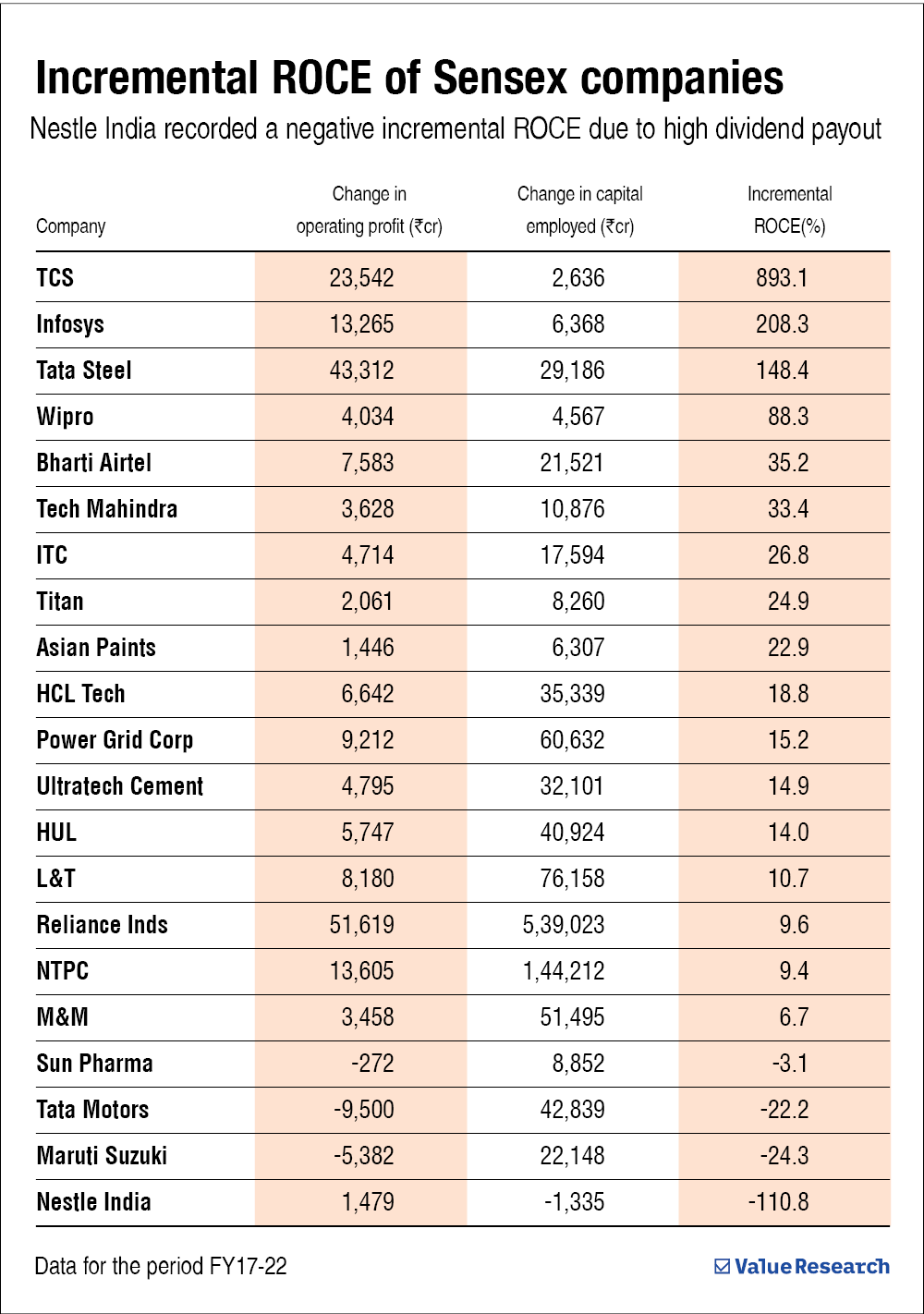

Here is how companies from the BSE Sensex (excluding banking and finance companies) performed in terms of incremental ROCE between FY17 and FY22.

Beware of buybacks and high dividend payouts

Suppose a company XYZ generated Rs 10 crore in operating profit after employing Rs 100 crore in FY15. Now, in FY20, it bought back some of its shares, which brought down the available capital to Rs 50 crore. But despite this, it generated an operating profit of Rs 15 crore in FY20.

This is an extremely desirable situation as despite employing half the capital, it managed to grow its operating profit by five per cent.

However, if you calculate the incremental ROCE for the above case, you will get a negative figure (as capital in FY20 is higher than in FY15), giving a false warning.

A similar scenario arises when a company distributes a high amount of dividends in a particular financial year, lowering its available capital.

Nestle India is a real-life example of this in our table.

Your takeaway

Note efficiency and profitability are indeed the two most crucial aspects of long-term wealth creation. And incremental ROCE is a useful metric to gauge both.

However, as investors, we must always dig deeper before making any decision. A company's management, promoters, growth opportunities, etc., are equally important. As always, do further research before investing in a company, regardless of its incremental ROCE.

Suggested read: Which is better: ROE or ROCE?

This article was originally published on May 11, 2023.

Ask Value Research ![]()