In the past few years, we have been rather scathing about the new-age cash-burning philosophy of growth at all costs. Often, you would find us highlighting how, without profits, revenue and valuations are just fancy dressing.

But profits are not everything. Even the legendary Warren Buffett has often hinted that he values efficient capital allocation more than profit growth.

For metric lovers, he feels return-on-equity (ROE) growth is more important than earnings-per-share (EPS) growth.

So, the question now is, why does the greatest investor of our time feel that?

Suppose a company named ABC spent Rs 1,000 crore in a year on expanding its business. In doing so, it added assets, and its book value (and shareholders' equity) grew 25 per cent. This investment also brought in additional earnings, and its profit after tax grew 20 per cent.

However, if one was to calculate the ROE (profit after tax / shareholders' equity) after this rise in earnings, one would notice that there has actually been a decline, which signals inefficiency.

In fact, as long as the growth in book value outpaces earnings growth, there would be a decline in ROE.

Mathematically, it's quite simple. An increase in shareholders' equity (the denominator) without a commensurate rise in the numerator (profit after tax) means the ROE will fall.

Even if you disregard the maths, the logic is simple. If you are spending big, the jump in profit should also be significant. Without that, profit growth is not sustainable, and it is a sign of poor management and capital allocation.

And there are actually many real-world examples of the above scenario.

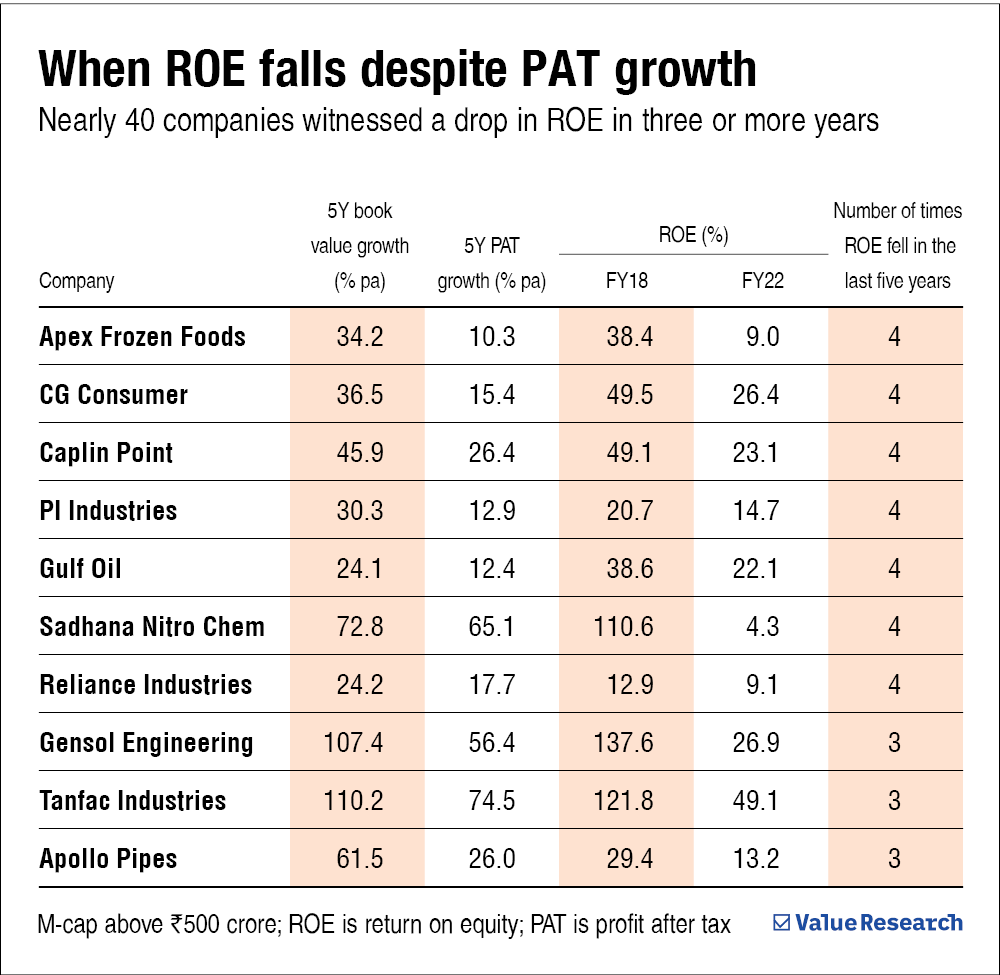

Here are 10 companies that posted a decline in their ROE numbers in the last five years despite double-digit per annum PAT growth.

We ranked the above companies based on the difference between their book value growth and PAT growth. Also, note that we excluded companies that recently got listed as they will have inflated shareholders' equity.

What you should do as an investor

We would like to point out that, at times, companies keep cash in hand, which inflates book value, to preserve capital for future opportunities. And waiting for the right opportunity to invest your capital is never a sign of poor management.

So does this mean our above exercise was in vain?

No. The purpose of the above exercise was to draw attention to the fact that if a company's book value growth is far higher than its PAT growth, it calls for scrutiny. Investors are often swayed when they see earnings growth in the green without analysing if the management is being efficient.

In short, you should focus both on earnings and efficiency when analysing a company. And as always, do the due diligence and research a company thoroughly before investing, not just its EPS growth and other popular metrics.

Suggested read: Efficiency kings on sale

This article was originally published on April 19, 2023.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()