The Union Budget in February 2023 announced a new small-savings scheme designed specifically for women called the Mahila Samman Savings Certificate (MSSC). While the finance minister provided some details about the scheme during the budget speech, there were still some unclear points, such as the circumstances under which partial withdrawals and premature closures would be allowed.

Now, after the budget has passed, the scheme has been officially launched on April 1, 2023, across 1.59 lakh post offices. Here is a detailed overview of the scheme based on the information available on the small-savings schemes section of the Indian post office website.

Mahila Samman Savings Certificate: Key features

April 1, 2023 to March 31, 2025

- Allowed only without penalty in case of the death of the account holder or in case of extreme compassionate grounds (life-threatening disease and/or death of the guardian).

- Can be closed after six months of account opening without giving any reason. However, the rate at which interest would be paid will get reduced by 2 percentage points. In the current scenario, it would be 5.5 per cent.

How does it work?

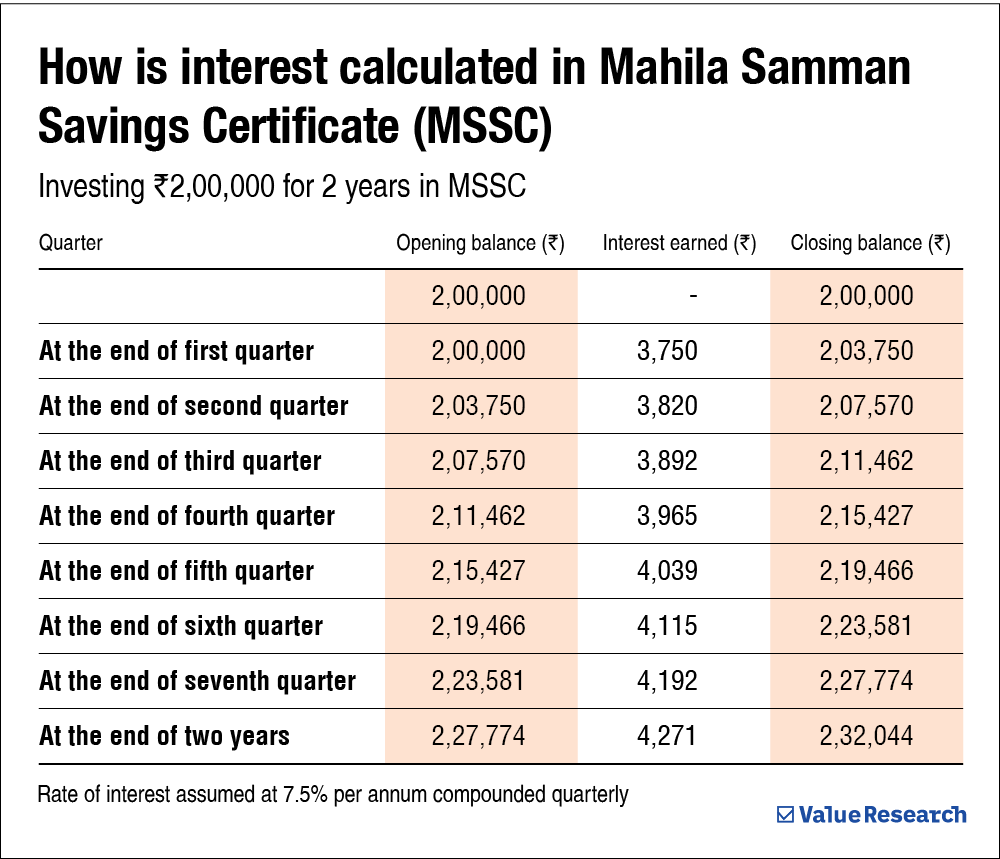

Mahila Samman Savings Certificate works like a fixed or time deposit, where interest gets calculated quarterly and accumulates along with the invested principal. For example, on an investment of Rs 2 lakh, the interest for the first quarter would be Rs 3,750. For the second quarter, it will be calculated at Rs 2,03,750 (Rs 2 lakh + Rs 3,750) since it is compounded quarterly. Accordingly, the maturity value at the end would be Rs 2.32 lakh.

How can you invest?

To invest in this scheme, you need to visit the nearest post office with a copy of your PAN, Aadhaar, a cheque for the deposit amount, and ask for the account opening form, which needs to be filled in and submitted.

How does it fare with other alternatives?

With a tenure of just two years, Mahila Samman Savings Certificate has the lowest tenure among all the small saving schemes. The other options with such a tenure are only a bank fixed deposit or a two-year-time deposit with the post office (POTD 2 year). On returns, it scores higher than both. A two-year-post-office deposit is currently returning 6.9 per cent, and a two-year fixed deposit from SBI is returning 7 per cent. So on that count, MSSC scores higher.

However, for senior citizens, opting for a Senior Citizen Savings Scheme (SCSS) may be better, as it is currently offering 8.2 per cent, although it comes with a tenure of five years.

This article was originally published on April 04, 2023.

Ask Value Research ![]()