The flood of IPOs of new-age companies has sparked countless debates on valuations in recent years. And more often than not, these debates are centred around P/E. Take the example of Nykaa. When the new age cosmetic seller debuted on D-street, many veterans pinched their noses when they saw a P/E of 1,600 times.

And rightly so. But very few were curious if Nykaa would ever earn enough to match its market cap, i.e., will it earn enough profits in its lifespan to break even its market capitalisation?

This is where the payback ratio comes in. It provides an estimate of how long a company will take to accumulate profits equal to its market capitalisation. Generally, it is calculated using the following equation:

Payback ratio = Current m-cap / estimated cumulative profit of the next five years

As future profits are open to interpretation, payback ratios may vary from investor to investor, depending upon how conservative they are with their projections.

A twist to the formula

We wanted to conduct a simple exercise with the payback ratio. Our goal was to determine the payback ratio of companies with a market cap of Rs 500 crore.

However, it's no secret that we are a conservative bunch. Hence, in that spirit, we assumed that the companies would repeat their last five years' performance. Meaning that in the next five years, they will earn exactly how much they earned in the past five years.

However, we hit a minor snag. You see, it might be possible that some companies recorded some losses a year or two and their cumulative profits of the last five years add up to zero.

Hence, we took companies that had a positive five-year cumulative profit figure.

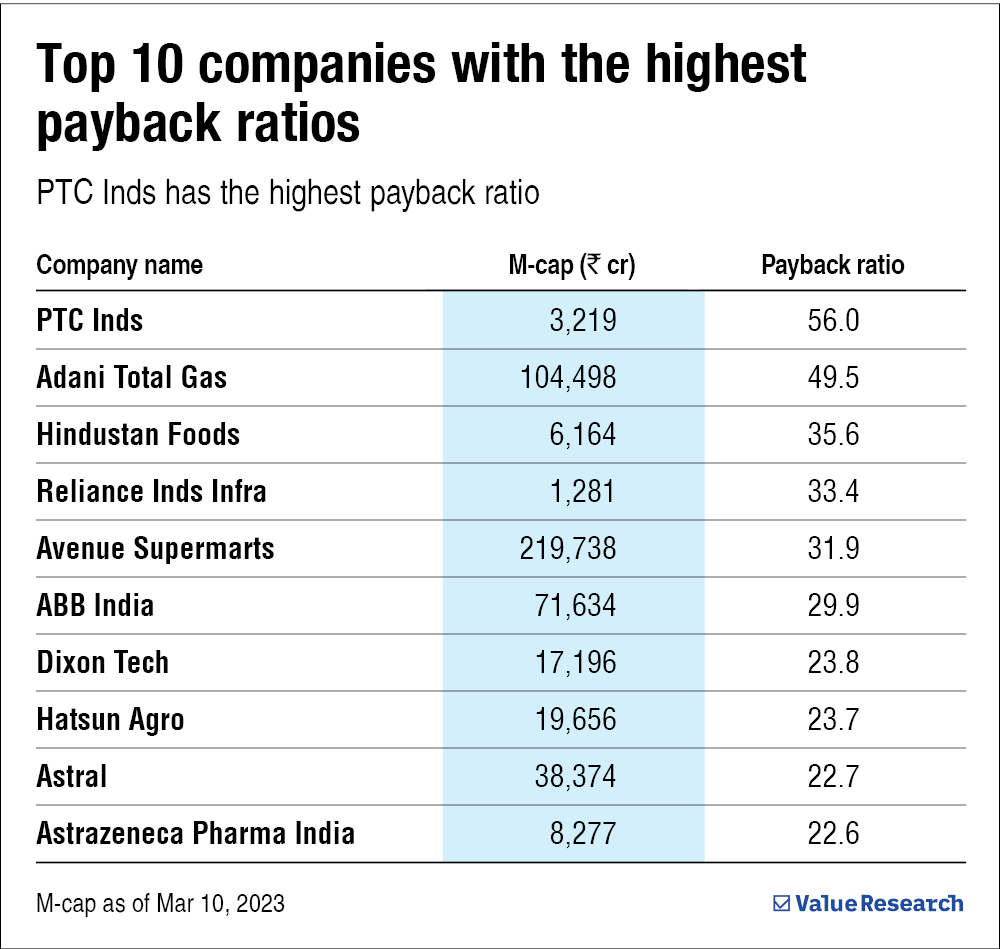

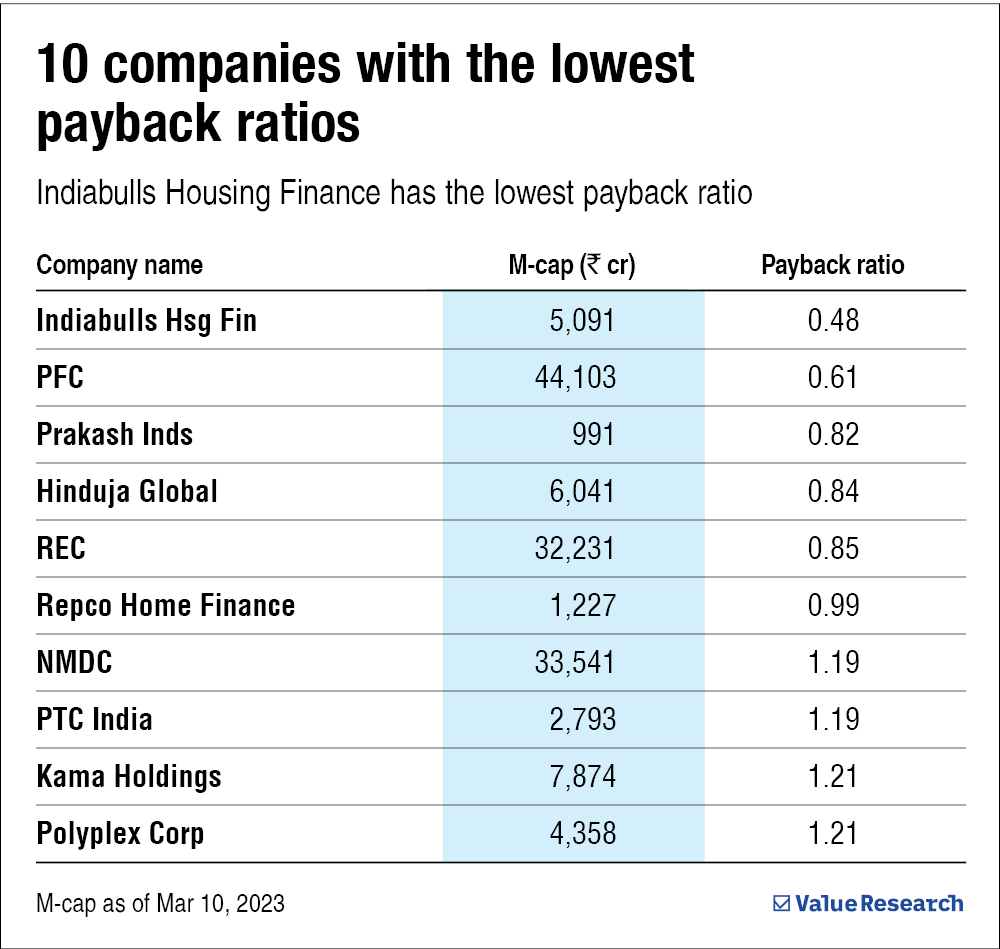

Here are the top ten companies with the highest and lowest payback ratio.

Are companies with high payback ratios bad investments?

No. While a high payback ratio calls for scrutiny, it does not mean they are bad investments.

The companies with high payback ratios are often large companies with hefty valuations. Thus, even if they are fundamentally strong and profitable companies, they might take decades to break even their enormous market cap.

On the other hand, while a low payback ratio is indeed attractive, companies with low payback ratios are often smaller companies. And it might just be that their low payback ratio has more to do with their low market cap and less with their ability to generate profits.

Thus, the payback ratio should be viewed in combination with other factors, such as growth prospects and fundamentals. If a company has a low payback ratio as well as huge growth potential, it indeed deserves your attention.

Suggested read:

What are price multiples?

What is diluted EPS?

This article was originally published on March 21, 2023.

Ask Value Research ![]()