With fixed deposit (FD) interest rates on the rise, many investors are questioning the efficacy of short-duration funds, a popular investment option.

While it is true that the returns on short-duration debt funds over the past year have been around 4.80 per cent, which is not very high compared to the current fixed deposit rates of around 6.80 per cent, this comparison is not entirely accurate.

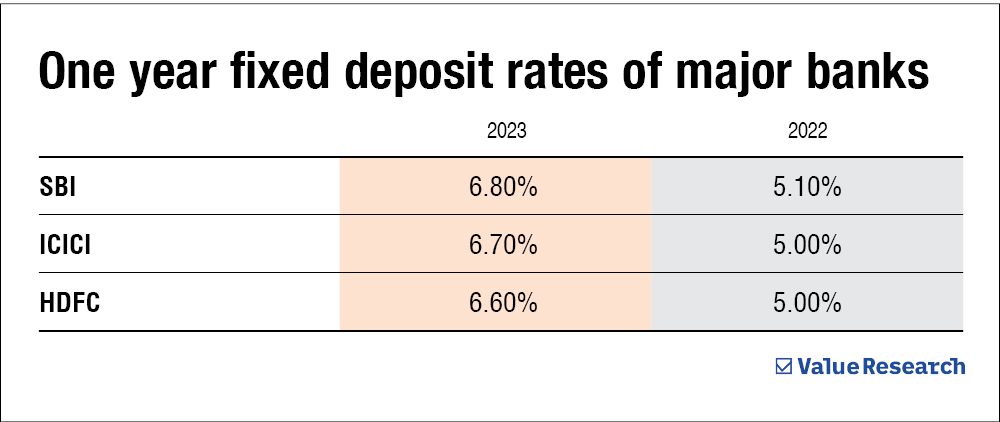

Comparing short-duration funds and fixed deposits

The returns on short-duration debt funds are historical, whereas the fixed deposit rates are forward-looking rates that you will receive in the next year. To make a fair comparison, we need to look at the yield-to-maturity (YTM) of short-duration debt funds.

Simply put, yield-to-maturity is the return you receive when you purchase a bond and hold it until it matures. If a fund portfolio's yield-to-maturity is 8 per cent, and all investors remain constant while the fund manager takes no action, you can reasonably expect your return on the fund to be the yield-to-maturity minus expenses. You can check the YTM of any debt fund by visiting the fundpage on Value Research Online.

The category average YTM of short-duration debt funds is 7.52 per cent, which is higher than the current FD rates, which are at 6.80 per cent. The FD rates in the beginning of 2022 were only 5.10 per cent. That's way lower than the current FD rates and the category average YTM of short-duration debt funds.

Additionally, short-duration debt funds have two advantages over FDs:

- First, they allow you to withdraw your money anytime without any penalty, while FDs require you to commit to a specific time period.

- Second, if you hold a debt fund for more than three years, you will only have to pay a 20 per cent tax on the gains after adjusting for indexation. On the other hand, interest earned on FDs gets added to your income and gets taxed according to the applicable tax slab. This can be especially important for people in the 30 per cent tax bracket.

Conclusion: Short-duration funds for the win

Despite the rise in interest rates for fixed deposits, short-duration debt funds remain a better investment option. They offer slightly higher returns, provide liquidity, and are better in terms of taxation.

Ask Value Research ![]()