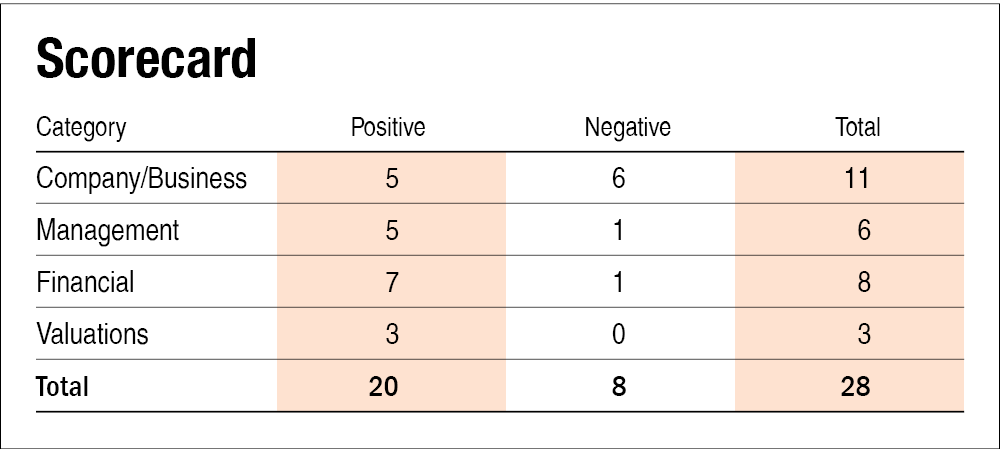

In our previous part of Electronics Mart IPO story, we read about the key details of the IPO. Here we will answer some questions about Electronics Mart and evaluate it on parameters like management, financials, valuations, etc.

IPO questions

The company/business

1) Are the company's earnings before tax more than Rs 50 crore in the last 12 months?

Yes. The company's earnings before tax for FY22 is Rs 140 crore.

2) Will Emart be able to scale up its business?

Yes. The company has been expanding aggressively, and the IPO proceeds will go towards opening new stores.

3) Does Emart have recognisable brands truly valued by its customers?

Yes. The name under which it opens its stores, 'Bajaj Electronics', is a recognisable brand for the locals in Andhra Pradesh and Telangana.

4) Does Emart have high repeat customer usage?

No. Given the nature of consumer durables and product life, there is unlikely high repeat customer usage.

5) Does the company have a credible moat?

No. The company does not have any kind of moat despite being one of the largest consumer durable retailers in India.

6) Is the company sufficiently robust to major regulatory or geopolitical risks?

Yes. The company does not have any revenue from overseas or is present in a highly regulated sector, making it safe from such risks.

7) Is the business of the company immune to easy replication by new players?

No. New players can easily start new stores.

8) Is the company's product able to withstand being easily substituted or outdated?

No. The company faces competition from e-commerce retailers, which can affect the company's footfall in future.

9) Are the customers of Emart devoid of significant bargaining power?

Yes. Since the customers are retailers and the price of products are similar in all stores, they do not have much say in price. But it is to be noted that customers can choose to switch sellers, which is the nature of retail.

10) Are the suppliers of Emart devoid of significant bargaining power?

No. Electronics Mart has to sell at whatever price the brands supply to them and cannot negotiate on the price since they are just retailers and do not add anything to the product.

11) Is the level of competition the company faces relatively low?

No. The company faces high competition in both offline and online areas.

Management

12) Do any of the company's founders still hold at least a 5 per cent stake in the company? Or do promoters hold more than a 25 per cent stake in the company?

Yes. The promoters will hold a 78 per cent stake post IPO.

13) Do the top three managers have more than 15 years of combined leadership at the company?

Yes. The company's Chairman, Pavan Kumar Bajaj, and CEO, Karan Bajaj, have been with the company since its inception.

14) Is the management trustworthy? Is it transparent in its disclosures, which are consistent with SEBI guidelines?

Yes. We have no reason to believe otherwise.

15) Is the company free of litigation in court or with the regulator that casts doubts on the management's intention?

No. The company has a lawsuit from Bajaj Electricals for trademark infringement, which, if lost, would result in losing the name 'Bajaj Electronics' that they use in Andhra and Telangana, which would impact the company drastically.

16) Is the company's accounting policy stable?

Yes. Although we would like to point out that since the company is in retail and mostly operates through leased premises, the introduction of Ind AS 116 from FY20 has increased the amount of depreciation. The financials of FY19 have not been disclosed for comparison.

17) Is the company free of promoter pledging of its shares?

Yes. The promoters have not pledged their shares.

Financials

18) Did the company generate a current and three-year average return on equity of more than 15 per cent and a return on capital employed of more than 18 per cent?

Yes. The company's current ROE and ROCE are 17 and 19 per cent, respectively. Its three-year average ROE and ROCE are 16 and 18 per cent, respectively.

19) Was the company's operating cash flow positive during the last three years?

Yes. The company posted positive operating cash flow in the last three years.

20) Did Emart increase its revenue by 10 per cent CAGR in the last three years?

Yes. Emart's revenue grew by 17 per cent per annum in the last three years.

21) Is the company's net debt-to-equity ratio less than one, or is its interest-coverage ratio more than two?

Yes. The company's net debt-to-equity as of August 2022 is 0.7 times (including lease liabilities), with an interest-coverage ratio of 2.7 times in FY22.

22) Is the company free from reliance on huge working capital for day-to-day affairs?

No. The company requires high working capital due to the nature of the retail industry. Right now, it runs with funds sanctioned by financial institutions.

23) Can the company run its business without relying on external funding in the next three years?

Yes. For expansion purposes, the money raised via IPO is enough, but the same is not the case for working capital.

24) Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

Yes. Its short-term borrowings have decreased by 27 per cent from FY20.

25) Is the company free from meaningful contingent liabilities?

Yes. The company is free from meaningful contingent liabilities.

Stock/Valuations

26) Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

Yes. The company offers an operating-earnings yield of 8.2 per cent based on FY22 operating income upon enterprise value (Market cap plus net debt) as of June 2022.

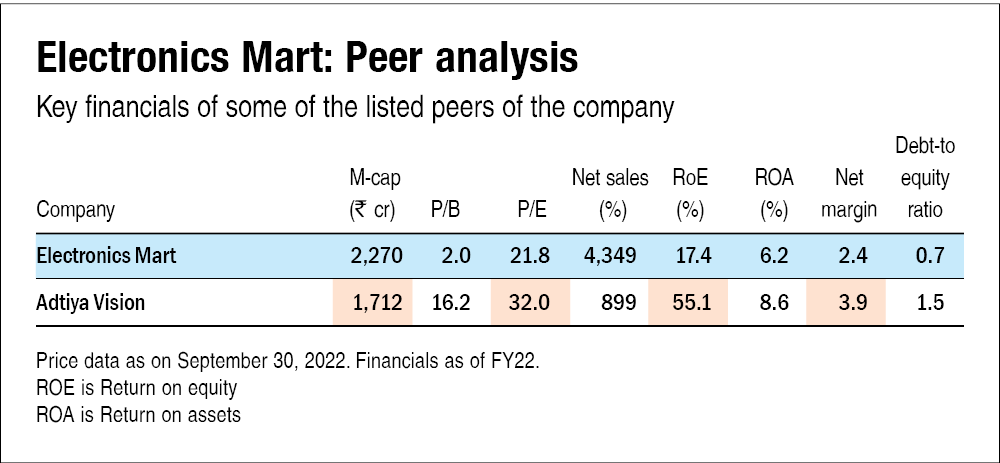

27) Is the stock's price-to-earnings less than its peers' median level?

Yes. The company will trade at a price-to-earnings ratio of 21.8 times which is less than its peer's price-to-earnings ratio of 32 times.

28) Is the stock's price-to-book value less than its peers' average level?

Yes. The stock will trade at a price-to-book value of 2 times compared to its peer's price-to-book value of 16 times.

Also, read our earlier story on Emart IPO to learn about key IPO details and important company information.

Disclaimer: The author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()