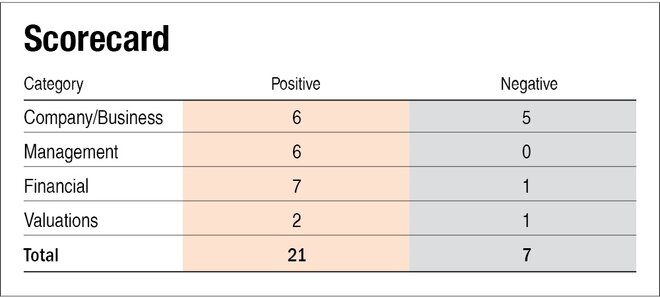

In our previous part of Syrma SGS Technology IPO story, we read about the key details of the IPO. Here we will answer some questions about Syrma SGS and evaluate it on parameters like management, financials, valuations, etc.

IPO questions

The company/business

1) Are the company's earnings before tax more than Rs 50 crore in the last 12 months?

Yes. The company's consolidated earnings before tax for FY22 were Rs 81 crore and Rs 111 crore based on proforma financial statements.

2) Will the company be able to scale up its business?

Yes. The recent acquisitions have already helped the company grow its business and the proceeds from IPO will be used to establish new R&D facilities and expand manufacturing capacities. Thus, Syrma SGS will be able to scale up the business comfortably.

3) Does the company have recognisable brands truly valued by its customers?

No. The company operates in B2B space and also competes with large players who have a bigger presence in the industry.

4) Does the company have high repeat customer usage?

Yes. 16 customers have been associated with the company for more than 10 years.

5) Does the company have a credible moat?

No. Even though the company is involved in precision manufacturing and is a leader in high-mix low-volume production, there are other domestic and international players who offer such services.

6) Is the company sufficiently robust to major regulatory or geopolitical risks?

No. The company imports 61 per cent of its raw materials and 44 per cent of its revenue are derived from exports in FY22. Thus any major geopolitical risks may affect their operations.

7) Is the business of Syrma SGS immune to easy replication by new players?

Yes. While there are few other players, it is extremely difficult for a new player to replicate the business as they not only need capital but also expertise. Taking market share in precision manufacturing segment is tough as clients expect a high level of accuracy.

8) Is the company's product able to withstand being easily substituted or outdated?

Yes. There are no substitutes for the company's products.

9) Are the customers of the company devoid of significant bargaining power?

No. The company's top five customers contribute around 41 per cent of revenue and it has some industry leaders as clients. Thus, the customers may have high bargaining power.

10) Are the suppliers of the company devoid of significant bargaining power?

Yes. While its raw materials are crucial, it sources them from various suppliers such that not one supplier has a significant contribution.

11) Is the level of competition the company faces relatively low?

No. While there aren't too many players in the industry, Syrma SGS competes with companies that generate ten times its revenue.

Management

12) Do any of the company's founders still hold at least a 5 per cent stake in the company? Or do promoters hold more than a 25 per cent stake in the company?

Yes. The promoters will continue to hold a 47 per cent stake post-issue.

13) Do the top three managers have more than 15 years of combined leadership at the company?

Yes. Sandeep Tandon (Executive Director), and Jasbir Singh Gujral (Managing Director) have combined experience of more than 15 years.

14) Is the management trustworthy? Is it transparent in its disclosures, which are consistent with SEBI guidelines?

Yes. We have no reason to believe otherwise.

15) Is the company free of litigation in court or with the regulator that casts doubts on the management's intention?

Yes. The company is free from material litigations.

16) Is the company's accounting policy stable?

Yes. We have no reason to believe otherwise.

17) Is the company free of promoter pledging of its shares?

Yes. The company's shares are free of any pledge.

Financials

18) Did Syrma SGS generate a current and three-year average return on equity of more than 15 per cent and a return on capital employed of more than 18 per cent?

Yes. The company's three-year average ROE is 16.3 per cent and its three-year average ROCE is 21.8 per cent. Its current ROE and ROCE are 13.6 per cent and 19.1 per cent respectively. We would like to mention that these numbers are based on proforma statements since the company had a major acquisition in 2021 and its FY20 numbers are skewed.

19) Was the company's operating cash flow positive during the last three years?

Yes. The company has posted positive operating cash flow in the last three years.

20) Did the company increase its revenue by 10 per cent CAGR in the last three years?

Yes. On a proforma basis, Syrma SGS increased its revenue by 21 per cent and by 28 per cent per annum on a standalone basis.

21) Is the company's net debt-to-equity ratio less than one, or is its interest-coverage ratio more than two?

Yes. The company's net debt to equity ratio was 0.3 times and its interest coverage ratio was 15 times in FY22.

22) Is the company free from reliance on huge working capital for day-to-day affairs?

Yes. The company has 1.3 times current ratio and has positive cash flow and will be able to manage its day-to-day affairs.

23) Can the company run its business without relying on external funding in the next three years?

Yes. The company will use the IPO proceeds for expansion projects so it will not need any external funding.

24) Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

No. Both on a standalone and proforma basis, the company's short-term borrowings have increased by 47 and 53 per cent per annum respectively.

25) Is the company free from meaningful contingent liabilities?

Yes. The company is free from material contingent liabilities.

Stock/valuations

26) Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

No. The company's operating earnings yield is just 2.2 per cent on a consolidated basis and 2.9 per cent on proforma basis.

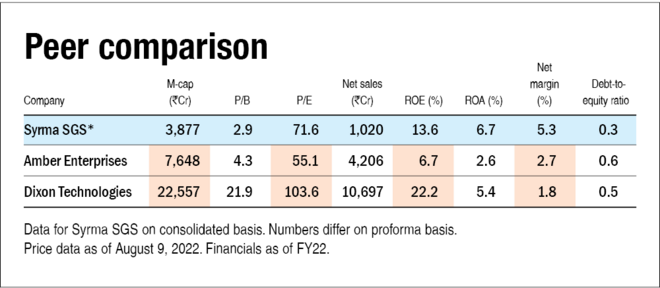

27) Is the stock's price-to-earnings less than its peers' median level?

Yes. The company will trade at a price-to-earnings of 71.6 times on a consolidated basis and 50.7 times on proforma basis against peers' median level of 79.4 times.

28) Is the stock's price-to-book value less than its peers' average level?

Yes. The company will trade at a price-to-book value of 2.9 times against peers' average level of 13.1 times.

Note: The company made some huge acquisitions in 2021 due to which its consolidated numbers jumped. It has disclosed consolidated financials for FY22 and FY21 but only standalone for FY20. And it disclosed proforma financials - how it would have been if the company had made the acquisition three years ago - as this will eliminate any major jumps from standalone to consolidated numbers when looking at three-year history.

Also, read our earlier story on Syrma SGS IPO to learn about key IPO details and important company information.

Disclaimer: The author may be an applicant in this Initial Public Offering.

Ask Value Research ![]()