When a company makes a profit, its management has to decide how to use it. A good capital allocation boils down to this. If the company can invest large amounts of capital at high rates of return, then it should retain a high portion of its profit. If however, the investment opportunities are either small or generate a low return, then the company should not retain a high portion of the profit. It should rather give it back to the shareholders.

When evaluating a company, you need to understand how well has the company allocated capital over the years. And there is a very simple measure that can help you evaluate a management's capital allocation skills. We came across this measure in the book 'Buffettology' by Mary Buffett and David Clark.

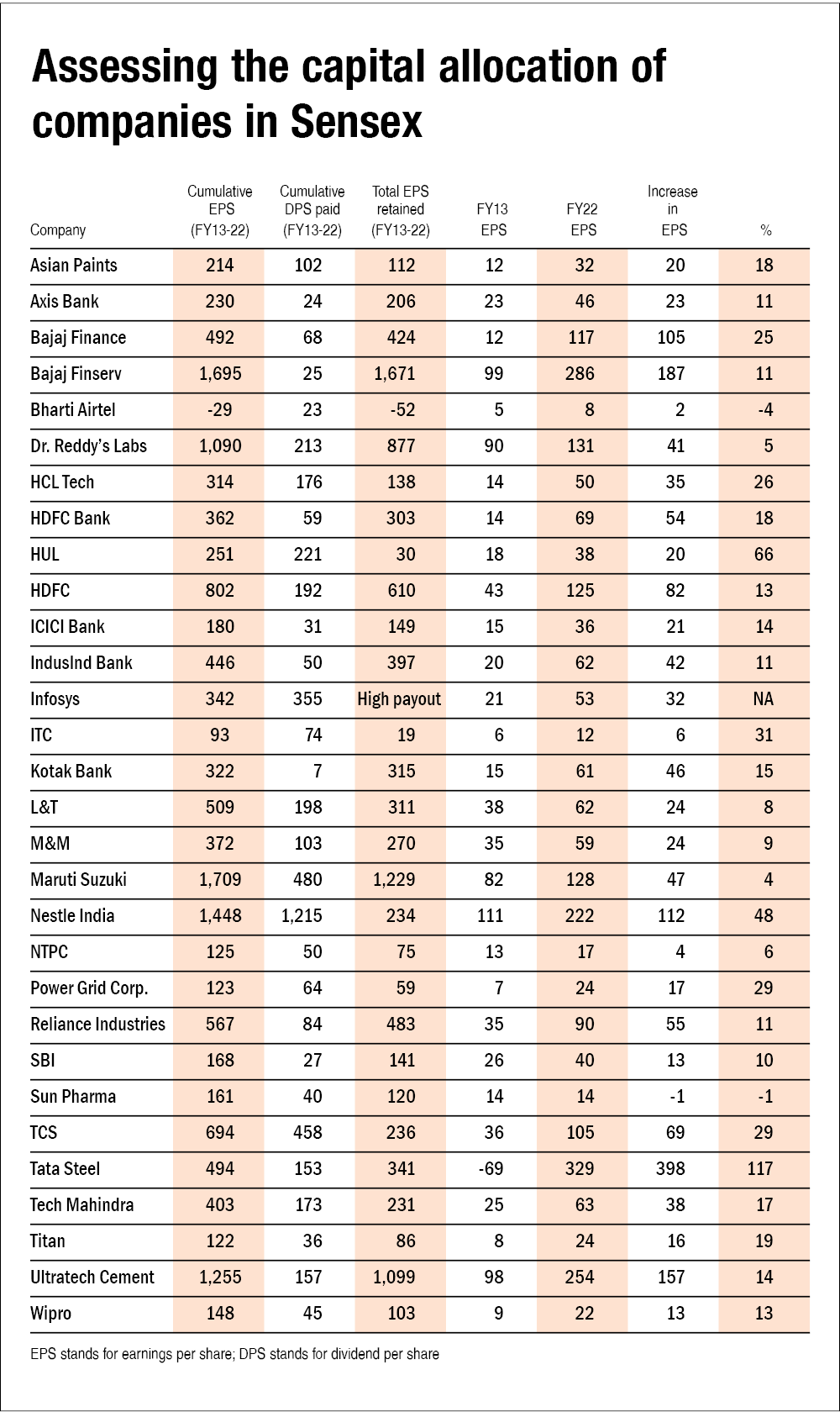

The idea behind this is that as companies retain profit to grow their business, that retained capital should help grow future profits. If a company is not able to do so, then it would have been better to pay out dividends to shareholders. The following table presents this measure for the companies in Sensex.

Let's understand how this works by using Titan's example. Titan earned a cumulative EPS (earnings per share) of Rs 122 over FY13-22. Out of this, it gave Rs 36 as dividends. Thus, its cumulative retained earnings per share was Rs 86. So far, so good.

From FY13 to FY22, its EPS went from Rs 8 to Rs 24, an earnings increase of Rs 16 per share. This means that Rs 86 of retained earnings led to an increase in EPS of Rs 16, translating to a return of 19 per cent.

As you would have guessed by now, a higher return is better. Use a period of 10 years if you are analysing a large company. For smaller companies, a five-year period is ideal. Anything less doesn't make sense. A smaller time period can be used for large companies in case of drastic changes in the business.

Bear in mind that your investment decision should not be based solely on this metric. Use this in conjunction with other measures.

Also, there are some drawbacks of using this measure:

- This measure is not ideal for companies exhibiting wobbly EPS over the years.

- Cyclical companies would report a great return at the peak of the cycle and a poor return at the bottom of a cycle. This is evident with Tata Steel.

- If a company reports a cumulative loss and a fall in EPS, then don't consider this measure, as both negative numerator and denominator would give a positive return figure.

- In the case of companies with a high dividend payout (e.g., Infosys), the cumulative EPS retained would be negative. This measure won't be helpful in such cases.

- Finally, this metric doesn't take share buyback into account.

Suggested read: Six parameters to look for in a company before investing

Ask Value Research ![]()