Ishaan, a 38-year-old software engineer, has good experience in equity investments. As of now, he has been able to accumulate about Rs 10 lakh in equity funds. His goals include saving for a comfortable retirement and the higher education of his five year-old daughter. Recently, he has read an article on asset allocation and has understood its importance to some extent. However, he is unsure about the appropriate asset-allocation plan for him. Also, he wants to know when and how he should change it over a period of time. Here is what he needs to know.

What is asset allocation? Why does it matter?

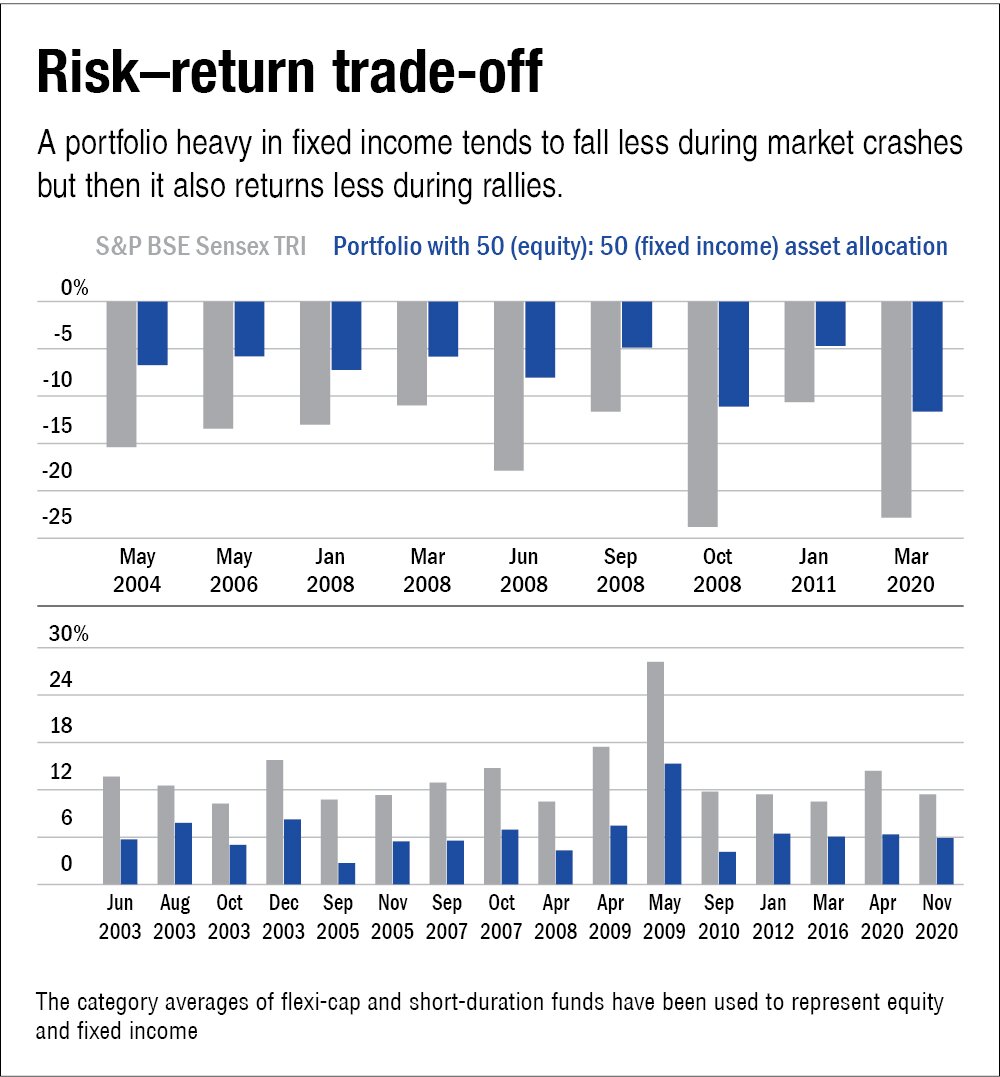

- Asset allocation means dividing your portfolio in a definite ratio across various asset classes, including equity, fixed income, commodities, etc. It helps in optimising the risk-reward ratio of the portfolio based on one's risk tolerance, return expectation and needs. For example, a conservative investor can have a higher allocation towards fixed income to protect the value of his investments during a market crash. But at the same time, he will have to compromise on the return (rewards) when the market rises significantly.

- Over time, your asset allocation may deviate due to several reasons like a change in the value of your investment, new investments, redemptions and so on. Rebalancing your portfolio periodically helps restore the desired asset allocation.

How to decide your asset allocation?

Your desired asset allocation can depend on many factors. Here are the key factors and how they apply to Ishaan's case.

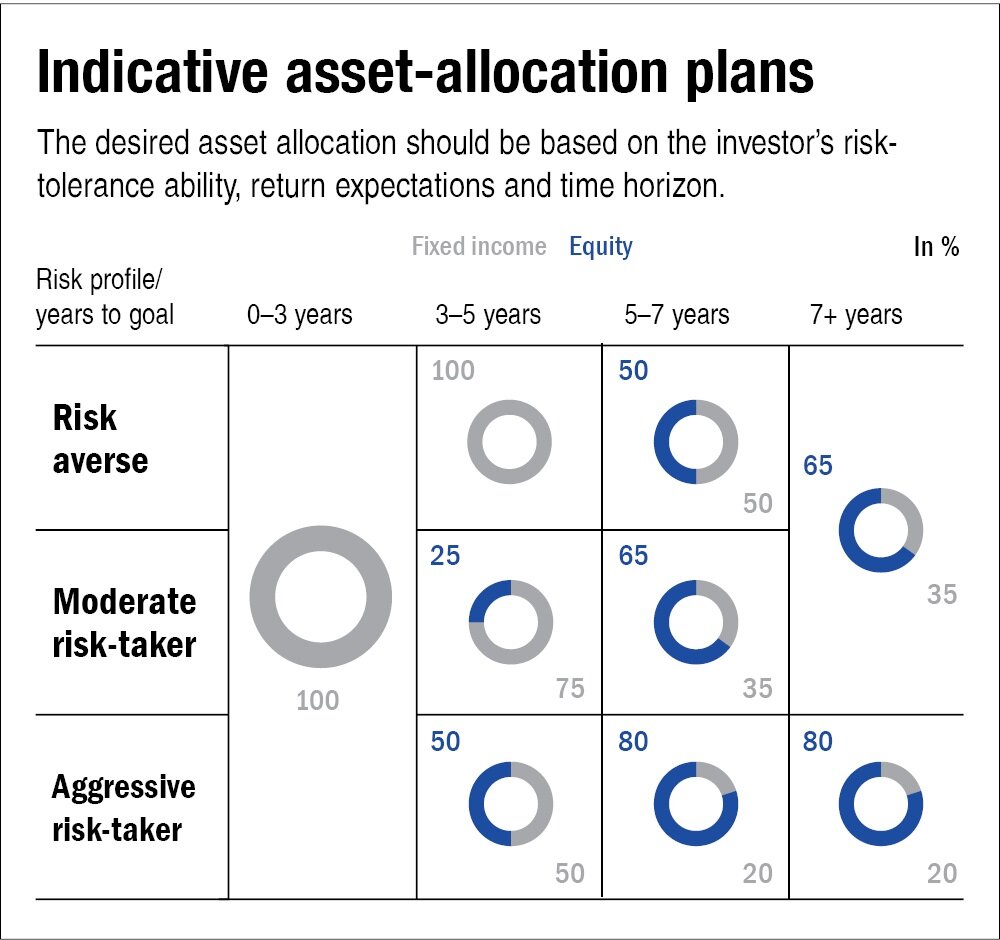

Risk-tolerance ability: Equities are riskier than fixed income. The value of equity investments moves up and down sharply in the short term. If Ishaan gets easily worried by the ups and downs in the value of his investment, then he should have some allocation to fixed income to make his portfolio stable. The higher the allocation, the lower would be the risk (volatility) and vice versa.

Return expectation: Risk and reward go hand in hand. If Ishaan allocates a higher portion of the portfolio to fixed income, then the return would be less. It is fine if the goal is nearby because then, the preservation of the capital is more important than any appreciation in order to achieve the goal on time. But since Ishaan has been investing for the higher education of his daughter and his retirement, which are 13 and 20 years away, respectively, he must allocate a higher portion to equities. Otherwise, he will have to compromise on returns and may not be able to accumulate a sufficient corpus.

Time horizon: Since equities are volatile and it becomes quite risky to depend on them for a near-term goal, the allocation to equities should decrease as you near the goal. So, while Ishaan can continue to have a higher allocation to equities, he should gradually start moving to the fixed income two to three years before he would need the money for his daughter's higher education. Likewise, he should move to a fixed-income-heavy portfolio three to five years before his retirement.

When should one change one's asset allocation?

- Contrary to what many believe, one should never change the asset-allocation plan of one's portfolio on the basis of market conditions. When the market turns volatile, it is natural to start thinking about whether to make any change in the portfolio. But since equities are volatile by nature, you should stick to your asset allocation during that time.

- While you should avoid changing your asset allocation solely due to market vagaries, you should rebalance your portfolio periodically. Rebalancing not just restores your asset allocation, but it also helps you invest more in the undervalued asset. That means investing more in equity when the markets have gone down and vice versa.

- A change in asset allocation should be triggered only when there is a change in any of the abovementioned factors - risk profile, return expectation and time horizon.

Should one add gold and silver to the portfolio?

- Ishaan also wants to know whether he should allocate a portion of his portfolio to commodities. Many investors prefer investing a portion of their portfolios in commodities, including precious metals like silver and gold, to hedge the portfolio. However, fixed-income avenues are always a better alternative and they are also less volatile. Gold and silver are unproductive assets and not good as an investment.

- However, if someone really wants to allocate a portion of the portfolio to precious metals, historically, gold has outperformed silver. When it comes to investing in gold, you can opt for Sovereign Gold Bonds (SGBs). Besides moving in tandem with the price of physical gold, they give a guaranteed interest of 2.5 per cent every year. In addition, capital gains on their maturity are tax-free.

Don't ignore these

- Emergency corpus: Maintain an emergency fund equivalent to your six-month to one-year expenses in a combination of sweep-in deposit and liquid fund.

- Life insurance: Buying a term plan with a cover of at least 10 times your annual income is a must if you have financial dependents.

- Health insurance: With the increasing number of lifestyle diseases and the COVID threat, it is important to have sufficient health cover for all the family members. Maintain a cover independent of the one provided by your employer.

This article was originally published on April 20, 2022.

Ask Value Research ![]()