It is always recommended to stagger your investment in equities over a period of time. Doing so helps average the purchase cost and reduces the risk of investing at the wrong level. Park the money in a liquid fund and set up a systematic transfer plan (STP) from there to the fund of your choice. Alternatively, you can continue holding the money in your bank account and set up a systematic investment plan (SIP).

As a general principle, a lump sum should be spread over half the period it took you to earn that money. But it should not exceed three years. A market cycle usually completes within that time and one is able to average the cost of purchase.

So if you have received your annual bonus and want to invest in equities, spread it over the next six months. Likewise, if you are investing a huge amount - lifetime savings or say your retirement money, spread it over the next three years.

Equity savings funds invest about one-third in equities, one-third in arbitrage opportunities and the remaining in fixed-income. These funds are suitable for those who cannot withstand too much volatility in the value of their investments and are content with moderate returns which are slightly higher than fixed income options.

Arbitrage is all about capturing the benefit from the mispricing opportunities between the cash and futures market in the equity segment. That is how they earn returns. For example, let's say, there is a stock that trades at Rs 100 in the cash market and at Rs 101 in the future market. So, by spotting this price differential, the fund manager buys the stock in the cash market at Rs 100 and sells it in the futures market at Rs 101, thereby locking this Re 1 differential through these trades.

Investing in arbitrage opportunities is less risky than pure equities and so are the returns. But they are riskier than investing in fixed-income. So while an equity savings fund would be more volatile than a fixed-income fund, it would be less volatile than a pure equity fund.

Watch the video to know if equity savings funds are better than arbitrage funds for an SWP.

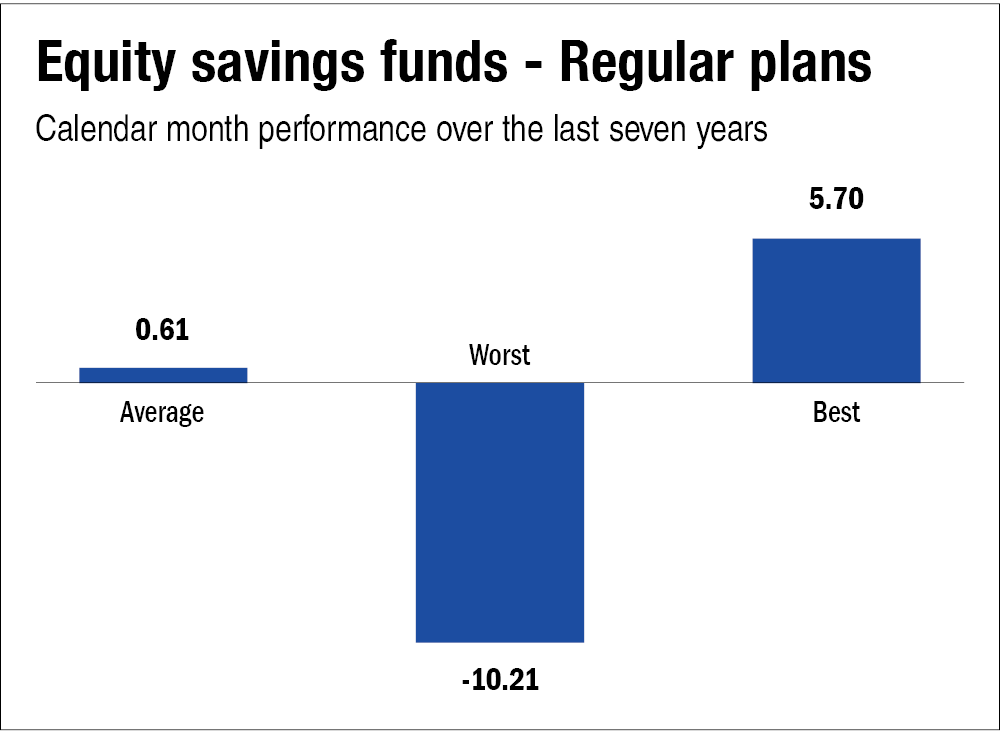

Though the category has returned over 10 per cent in the last one year, do remember that equities are volatile, especially in the short run, and do not offer capital protection like a fixed deposit. And equity savings funds are no different though they fall less than a pure equity fund when the market falls. They have a smaller allocation to equities.

The category's worst fall in a calendar month over the last seven years was in March 2020 when the markets crashed due to COVID. The returns were negative. They had fallen by more than 10 per cent. See the chart below.

Suggested read: Choose the 'best' mutual fund for YOU

This article was originally published on April 15, 2022.

Ask Value Research ![]()