One97 Communications (Paytm) came out with its IPO three months ago. You can find our detailed analysis of the issue. In this update, we will look at Paytm's market performance and business performance post issue.

Our analysis of the IPO

One97 Communications -owned Paytm is one of India's leading digital eco-system for merchants and consumers. Their services include payment services, cloud services, and various other financial services. They cater to 33 crore registered customers and 2 crore registered merchants as of June 30, 2021. Consumers can use the platform for various purposes such as peer-to-peer transactions, in-store payments, bill payments, ticket bookings, and financial products such as insurance, credit card, personal loans and more. The company holds a 49 per cent stake in Paytm Payments Bank, the only profitable venture of Paytm, which provides services such as wallets, FASTags, bank accounts and UPI services. Based on the company's leadership and brand recognition, we gave the company a score of 14 out of 26. Some of the concerns we had were its continuous losses and cash burn.

Our rating of the company was based on the following factors:

- Out of 11 business metrics, the company did well only on five.

- Out of six management-related metrics, the company did well on five.

- Out of eight financial metrics, the company did well on four.

- On the only valuation-related metric, the company failed to perform well.

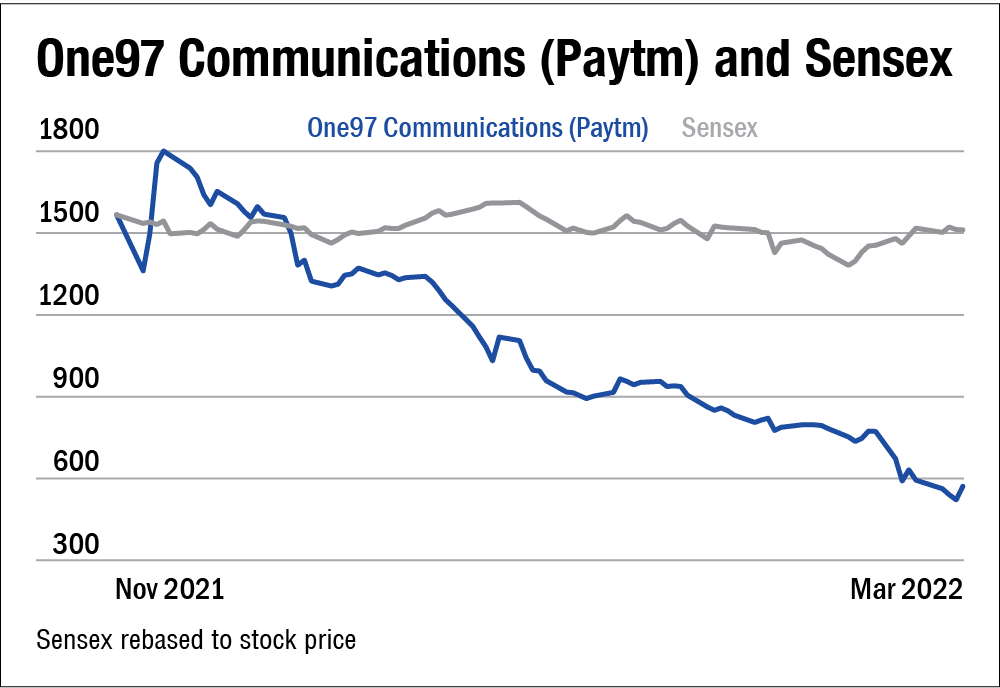

Stock performance since listing

Despite being the largest IPO in India, One97 Communications failed to gather the interest of investors as the issue was only subscribed 1.9 times. The institutional portion was subscribed 2.8 times, the high net worth individuals portion was subscribed 0.2 times, and the retail portion was subscribed 1.7 times.

Paytm had a poor listing as the company listed at Rs 1,955, which is 9.1 per cent less than its issue price. Since listing, the share has been going downhill. The company is currently trading at Rs 574, which is a massive 70.6 per cent down from its list price.

There were various reasons for this poor performance such as expensive valuation combined with continuous losses, the resignation of top management personnel such as Amit Nayyar, Paytm President, Abhishek Arun, COO of Paytm Payments Bank, Rohit Thakur, Chief Human Resources Officer, and many more. Five officials resigned just before the IPO and three resigned right after. Recently, Paytm Payments Bank was barred by the RBI from onboarding new customers which accelerated the fall.

Business performance

Despite performing poorly in the market, the company performed well financially in Q3FY22. The company's revenue increased by 89 per cent YoY and contribution profit increased by a massive 560 per cent. Their business grew on all fronts as payments and financial services grew by 98 per cent YoY, merchant payments GMV (Gross Merchandise Value) grew by 123 per cent YoY, number of loans disbursed increased by 366 per cent YoY, and commerce and cloud services grew by 64 per cent YoY. A number of monthly transacting users also increased by 37 per cent YoY.

Some major reasons for this growth on all fronts were an increase in the processing of merchant payments through MDR-bearing instruments, a recovering economy, and an increased number of loans disbursed. An increase in revenue set off the increase in overall direct expenditure by 43 per cent. An increase in employee benefit expenses by 147 per cent resulted in the widening of loss for the period by 45.4 per cent. Paytm Payments Bank is banned by the RBI from onboarding new customers on the grounds that its servers have been sharing information with Chinese companies which own an indirect stake in the company. This may also make it difficult for it to obtain licenses for small finance bank operations.

What to do now?

One of the reasons why despite high valuations, investors and analysts like this company is because of its firm leadership in an underpenetrated market. The fintech segment still has a long way to go and Paytm has managed to have a market share of 40 per cent in transaction volumes and around 65 per cent in wallet payments transactions.

Although the company is currently trading at a price to book of 1.6 times, which is less than its IPO valuations, its losses still cause wariness among investors. Paytm is not only a loss-making company, but is also reporting negative operating cash flow. Their recent ban on onboarding new customers in payments bank may further hamper their growth for the next few months. Investors who would like to consider investing in the company need to do their due diligence on customer retention rate, the scope of growth, expenditure incurred by the company, employee benefit expenses paid, and valuations.

Disclaimer: This analysis is not intended to serve as a recommendation. Readers must do thorough research before investing in this company. If you are interested in our stock recommendations, please visit Value Research Stock Advisor.

Also read:

One97 Communications (Paytm) IPO: Information analysis

Our other recent IPO updates:

Sigachi Industries - IPO update

FSN E-commerce Ventures (Nykaa) - IPO update

Ask Value Research ![]()