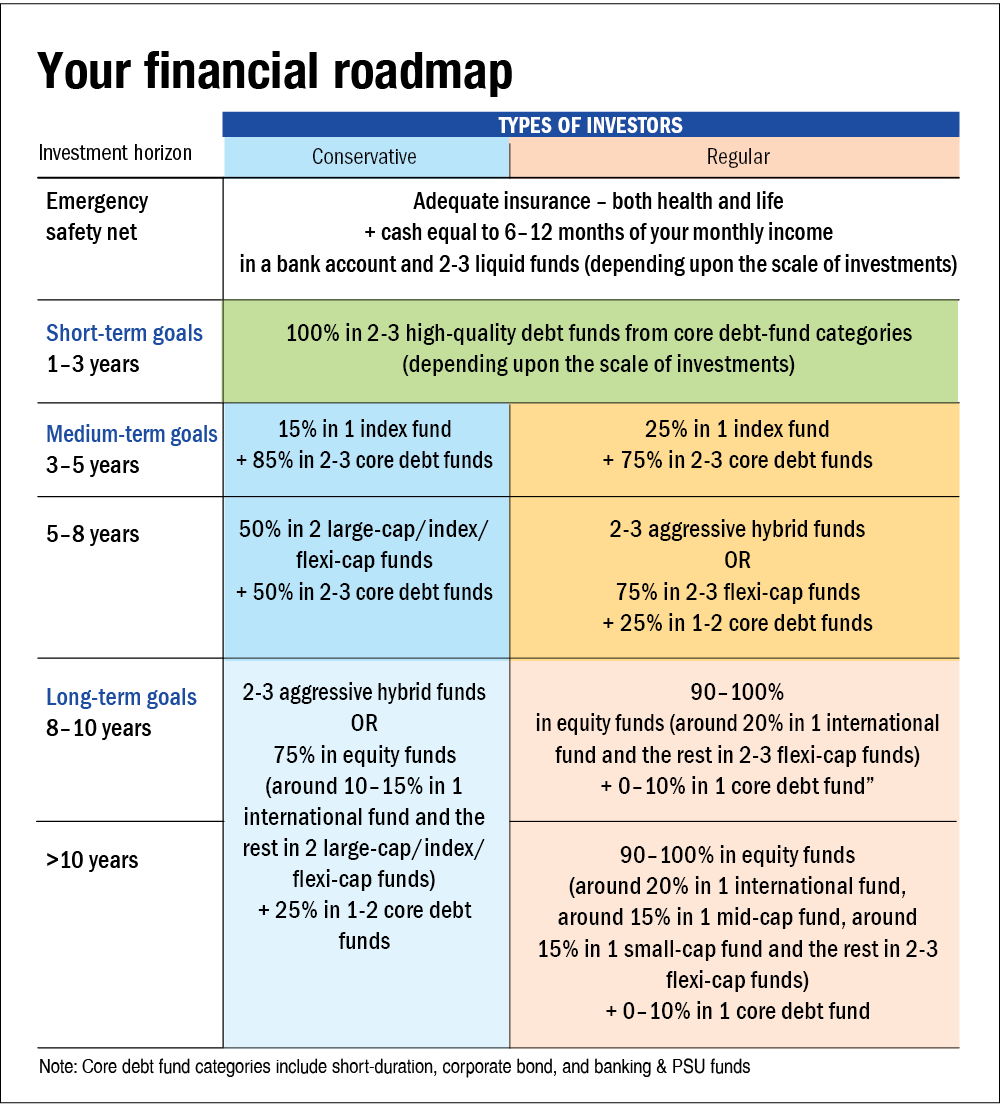

Congratulations! After realising your risk appetite, you are in a pretty good position to plan for your financial goals. In the table 'Your financial road map', we have drawn up guidelines on how to build your portfolio. The table is divided into two parts based on the risk appetite of investors. Thereafter, the goals are categorised based on their individual time horizons.

However, before you start with your goals, you should first have a safety net for any emergency. And when it comes to building a safety net, you need a two-pronged approach - having adequate insurance (health as well as life) and having a sufficient emergency corpus for any unforeseen roadblocks that you may encounter during your journey. Address these two things even before you start your investment journey.

Next comes forming your portfolio. Although the table provides some basic ideas, you should figure out the exact allocation to any asset class based on your risk appetite, comfort and negotiability of your goal (more on this later).

- The shorter the goal horizon, the safer the investment vehicle you should use. Since debt funds are often the least volatile and among the most stable instruments across fund categories, they are the ideal candidates for your goals that are due within one to three years.

- For goals that are due after three years but less than seven years, having a slightly higher allocation to equity makes sense, as it provides an impetus to beat inflation while most of your portfolio is still allocated to debt, providing the much-needed stability.

- For goals with a much longer horizon, equity should unequivocally form an integral part of your portfolio. However, just to reiterate, do not lose sight of the first step - 'know thyself'.

Also in 'How to become an expert mutual fund investor' series:

Part 1: Know thyself

Part 3: Balance is the key

Part 4: Avoid hitting bumps

Part 5: Don't forget the reverse gear

Part 6: Cherry-picking funds

Part 7: Be a sage

This article was originally published on December 23, 2021.

Ask Value Research ![]()