In our story, Shriram Properties IPO: Information analysis, we shed light on the critical details of the IPO, along with important information about the company. Here we will answer some questions about Shriram properties and evaluate it on parameters like management, financials, valuations, etc.

IPO questions

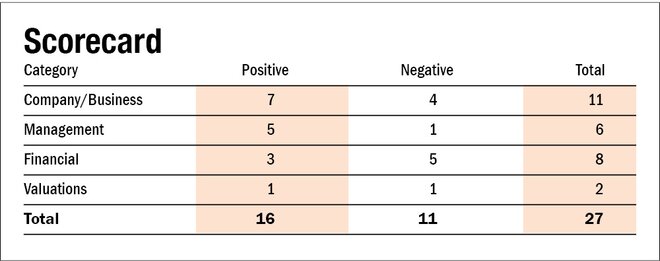

The company/business

1) Are the company's earnings before tax more than Rs 50 crore in the last 12 months?

No. In the last financial year ended March 31, 2021, the company reported a loss of Rs 45 crore before taxes.

2) Will the company be able to scale up its business?

Yes. Housing demand in India is expected to increase, supported by an increase in the overall population and a growing urban population. Apart from this, government reforms and initiatives such as the introduction of real estate reforms RERA, schemes for the promotion of affordable housing, and implementation of GST has increased the demand for housing which provides enough room for the companies in this sector to grow.

3) Does the company have recognisable brands truly valued by its customers?

Yes. The company is part of one of the prominent business groups, the Shriram Group, which has an operating history of four decades in India and has a very strong brand recall.

4) Does the company have high repeat customer usage?

No. The company operates in a housing development business that does not involve frequent purchases, and thus repeat customer usage tends to be low.

5) Does the company have a credible moat?

No. The company is part of the real estate sector which is highly regulated and faces stiff competition from the organised and unorganised players. Though it has a high brand value due to the Shriram Group, it does not have any distinct moat to differentiate itself from its peers.

6) Is the company sufficiently robust to major regulatory or geopolitical risks?

Yes. The company has successfully navigated regulatory hurdles so far, and therefore, we have no reason to believe otherwise.

7) Is the company's business immune from easy replication by new players?

Yes. Real estate development is a high capital-intensive business, and replicating a large company with a high brand value might not be easy.

8) Can the company's product withstand being easily substituted or outdated?

Yes. Demand for housing is a basic necessity that cannot be substituted or outdated.

9) Are the customers of the company devoid of significant bargaining power?

Yes. The company is one of the top five real estate companies in South India, and also, due to the B2C nature of its business, customers do not have significant bargaining power.

10) Are the suppliers of the company devoid of significant bargaining power?

Yes. The company's supplier includes third-party contractors and raw material providers wherein there are many players. Thus its suppliers don't have high bargaining powers.

11) Is the level of competition the company faces relatively low?

No. The real estate industry is highly fragmented, which leads to a high level of competition from unorganised and organised players.

Management

12) Do any of the company's founders still hold at least a 5 per cent stake in the company? Or do promoters hold more than a 25 per cent stake in the company?

Yes. Post-IPO, the promoter and promoter group will hold about a 28 per cent stake in the company.

13) Do the top three managers have more than 15 years of combined leadership at the company?

Yes. Managing director, M Murali, has been associated with the company since 2003.

14) Is the management trustworthy? Is it transparent in its disclosures, which are consistent with SEBI guidelines?

Yes, we have no reason to believe otherwise.

15) Is the company free of litigation in court or with the regulator that casts doubts on the management's intention?

No, there are a lot of pending cases against the company.

16) Is the company's accounting policy stable?

Yes. As per the auditors' report, the accounting policy is stable.

17) Is the company free of promoter pledging of its shares?

Yes. The company's shares are free of any pledging.

Financials

18) Did the company generate a current and three-year average return on equity of more than 15 per cent and return on capital employed of more than 18 per cent?

No, the company's three-year (FY19-21) average return on equity was -1 per cent and a return on capital employed of 7.9 per cent. For FY21, the company generated a return on equity of -4.0 per cent and a return on capital employed of 7.3 per cent.

19) Was the company's operating cash flow positive during the last three years?

No. The company reported negative cash flows from operations in the fiscal year 2019.

20) Did the company increase its revenue by 10 per cent CAGR in the last three years?

No. The company's revenue decreased from Rs 650 crore in FY19 to Rs 431.5 crore in FY21.

21) Is the company's net debt-to-equity ratio less than one, or is its interest-coverage ratio more than two?

Yes. The company's net debt-to-equity ratio stood at 0.85 as on September 30, 2021.

22) Is the company free from reliance on huge working capital for day-to-day affairs?

No. By the nature of their business, real estate companies are reliant on huge amounts of working capital. However, a significant portion of their working capital needs is funded by pre-sales, and it is the high inventory days that increase demand for high working capital.

23) Can the company run its business without relying on external funding in the next three years?

No. Though the company plans to pay a part of its debt obligation from the IPO proceeds, it will still be left with debt on its balance sheet with a low amount of cash and cash equivalents. Thus, the company might have to rely on external funding in the future.

24) Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

Yes. The company's short-term borrowing has remained stable and stands at Rs 646.6 crore as of September 30, 2021.

25) Is the company free from meaningful contingent liabilities?

Yes, the company has contingent liabilities of Rs 37 crore as of September 30, 2021.

Stock/valuations

26) Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

No, the company's stock offers a yield of 2.9 per cent as of September 30, 2021.

27) Is the stock's price-to-earnings less than its peers' median level?

Not applicable. The company has reported a loss for FY20 and FY21.

28) Is the stock's price-to-book value less than its peers' median level?

Yes. The company's P/B of 2.0 is less than the competitors' median of 3.2.

Also read Shriram Properties IPO: Information analysis to learn about key IPO details and important information about the company.

Disclaimer: The author may be an applicant in this Initial Public Offering

Ask Value Research ![]()