A bank fixed deposit is also known as a term deposit, which earns better interest as compared to the interest that the account balance earns in a savings bank account. This is a type of financial instrument in which, a certain sum of money is placed with the bank for a specified time period at a fixed interest rate.

The interest rates offered by banks on such deposits depend on the number of days, weeks or months, for which the deposit is maintained. There is great flexibility in the maturity period, which ranges from seven days to 10 years. The interest is higher in the case of a longer maturity period and can be compounded quarterly, half-yearly or annually. However, it varies across banks. The main draw for such deposits is the guaranteed interest that deposits earn.

Features of bank fixed deposits

1) Eligibility

- You need to be a resident Indian with a savings bank account.

2) Entry age

- You need to be over 18 years.

- Minors can open a deposit with the natural guardian operating it.

3) Investments

- Minimum: Rs 1,000

- Maximum: No limit

4) Interest

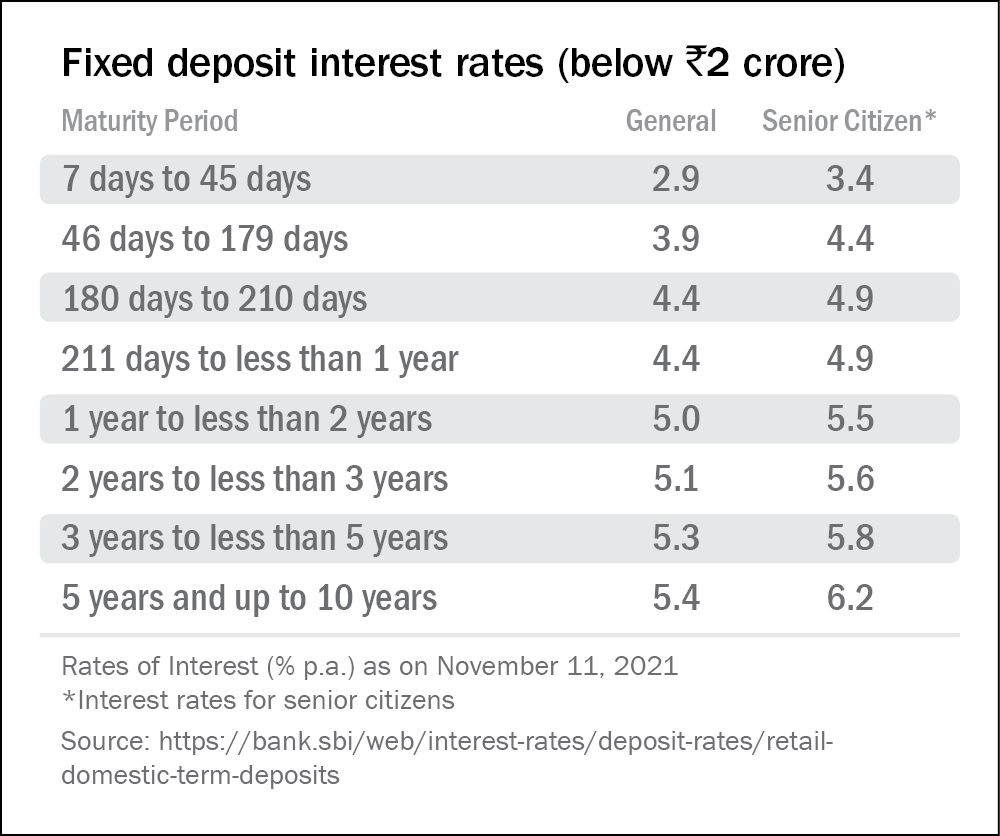

- Depends on the tenure of the deposit (See table for current rates).

- Currently goes from 2.90 per cent to 5.40 per cent per annum.

5) Tenure

- Currently offered up to 10 years

6) Account holding categories

- Individual

- Joint

- Hindu Undivided Families (HUF) not engaged in any trading or business activity.

- Companies or associations or trust.

- Minor through the guardian.

7) Nomination

- Facility is available.

8) Exit option

- Early closure of a deposit is permitted with a penalty.

Investment objective and risks

- The prime objective of the bank deposit is to earn a better interest on savings as compared to what an ordinary savings-bank account offers. Such deposits are preferred by risk-averse investors, who find the guaranteed fixed returns extremely reassuring to invest in.

- Risks: Interest-rate changes pose risks to existing deposit holders. For instance, you may have locked in your money in a deposit at a lower interest rate. However, owing to economic factors, the bank starts to offer a higher rate on deposits later.

- If the bank where you have the deposit does not have deposit-insurance-and-credit guarantee, you run the risk of losing the capital and interest.

Suitability and alternatives

- Suitable for conservative investors seeking assured returns from a lump-sum investment for goals up to five years away.

- Not suitable for: (i) long-term wealth creation, given their inability to provide any meaningful returns above the rate of inflation; (ii) investors looking to invest small amounts regularly.

- Alternatives can be: (i) National Savings Certificate (ii) Post office time deposit (iii) Company deposits (iv) Debt mutual funds can offer better, though not guaranteed returns.

Aspects of bank fixed deposits

1) Capital and inflation protection

The capital in a bank is fully protected up to Rs 5 lakh by the Deposit Insurance and Credit Guarantee Scheme of India.

The deposit is not inflation protected, which means whenever inflation is above the deposit interest rate, the deposit earns no real returns. However, when the interest rate is higher than the inflation rate, it does manage a positive real rate of return.

2) Guarantees

The interest rate is fixed and guaranteed for the duration of the deposit at the commencement of the deposit.

3) Liquidity

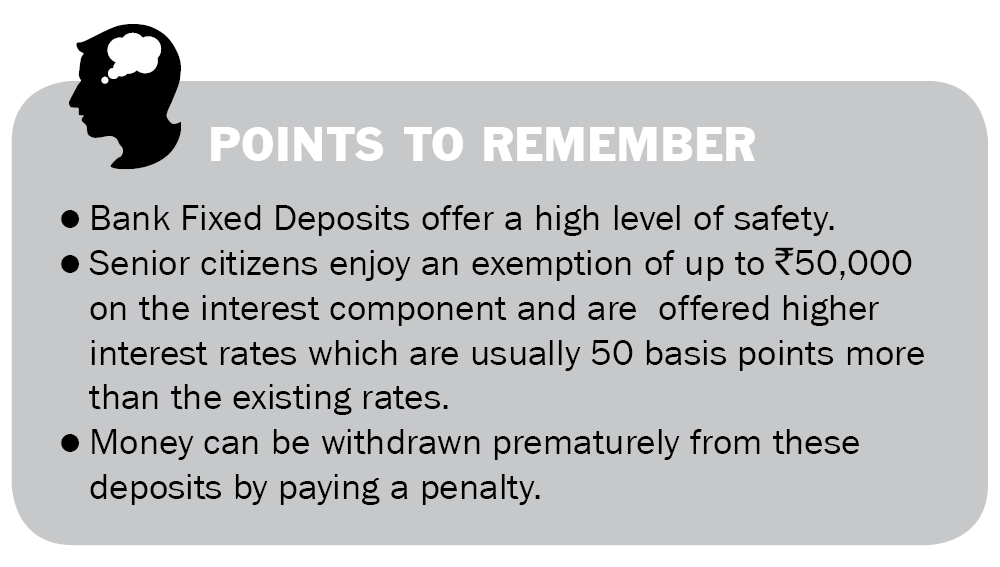

The fixed deposit has a lock-in period but allows withdrawals on the payment of a penalty.

4) Tax implications

A special type of deposit with a maturity period of five years in a scheduled bank is eligible for tax deduction under Section 80C. However, the interest earned on all types of fixed deposits is considered as an income from other sources when computing income tax except for senior citizens who are eligible to take a deduction of interest earned from bank deposits for maximum Rs 50,000. Effective from FY 2019-20, tax is deducted at the source on the interest income of above Rs 40,000 at a rate of 10 per cent. For senior citizens, TDS is applicable on the interest income of above Rs 50,000.

Various types of bank fixed deposits

1) Fixed deposit

In this type of deposit, both the tenure and the interest rate for the tenure are fixed.

2) Tax-saver fixed deposit

These deposits with a five-year lock-in period are tax deductible under Section 80C.

Where to open a deposit

You can open a deposit at any nationalised, private sector or foreign bank.

How to open a deposit

- Select the bank branch.

- Choose a nominee.

- Your existing bank account counts as being KYC compliant if you open the FD at the same bank.

How to operate a deposit

- You can issue a cheque to the bank through your existing savings bank account to start a deposit.

- A deposit receipt or certificate is issued with deposit details.

To view the current rates on the schemes, go to vro.in/s34211

This article was originally published on November 02, 2021.

Ask Value Research ![]()