A bank account is a financial account with a banking institution, recording the financial transactions between you (the account holder) and the bank. The purpose of a bank account is to encourage savings and bring financial transactions to the banking network. There are several types of bank accounts that you can opt for, depending on your needs. For instance, a businessman will prefer a current account, while a salaried individual will opt for a savings bank account.

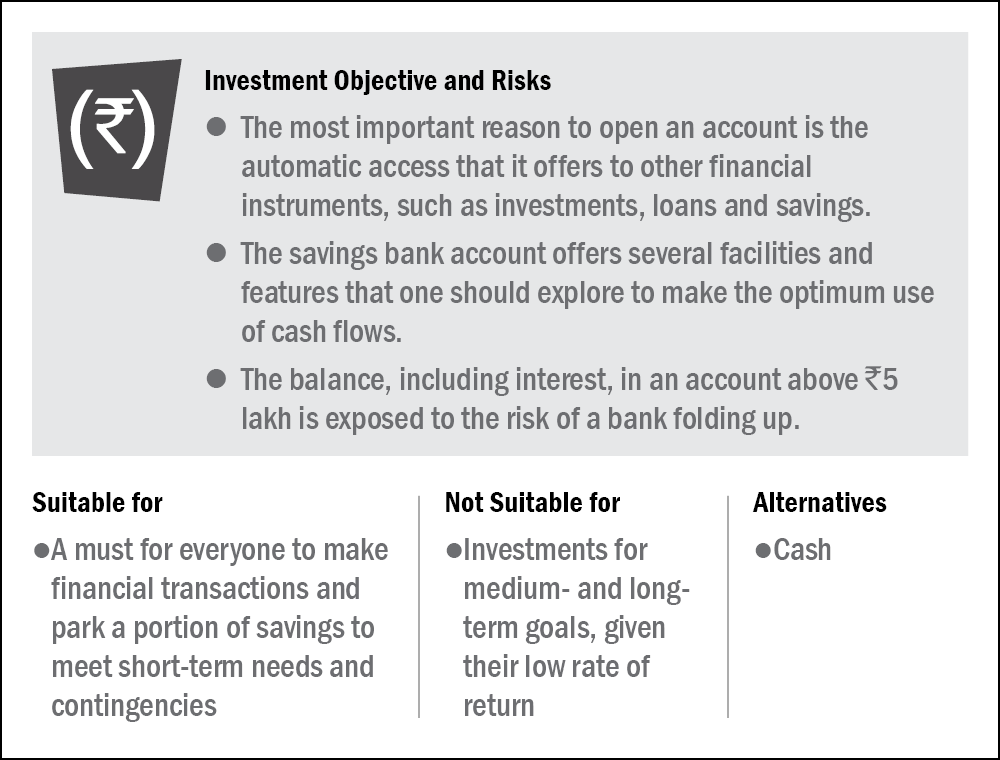

Savings bank accounts are meant to promote the habit of saving among people while allowing them to use their funds when required. Main advantages of a savings bank account are its high liquidity, safety and a moderate interest on the

savings. The savings bank account is the traditional home for cash savings. Today, a savings bank account is a necessity and an essential component of an individual's finances.

Savings account: Advantages and disadvantages

Capital & inflation protection

The capital in a savings bank account is not completely safe. The balance in the account, including the interest earned, is insured up to a maximum of Rs 5 lakh. This sum is insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC) for all commercial banks, branches of foreign banks functioning in India, small finance banks, co-operative banks, local area banks, regional rural banks and payment banks. It is advisable to check whether your bank is covered under the DICGC because if a bank has not been paying the premium for the insurance scheme for three consecutive half-year periods, it ceases to be insured. To view the list of banks insured by DICGC, go to, https://www.dicgc.org.in/FD_ListOfInsuredBanks.html. This insurance cover includes all accounts of one

depositor held with different branches of the same bank. However, deposit insurance coverage limit is applied separately to the deposits in different banks.

A savings bank account does not provide protection against inflation. This means that whenever inflation is above the rate that a savings bank account earns, the account earns no real returns.

Guarantees

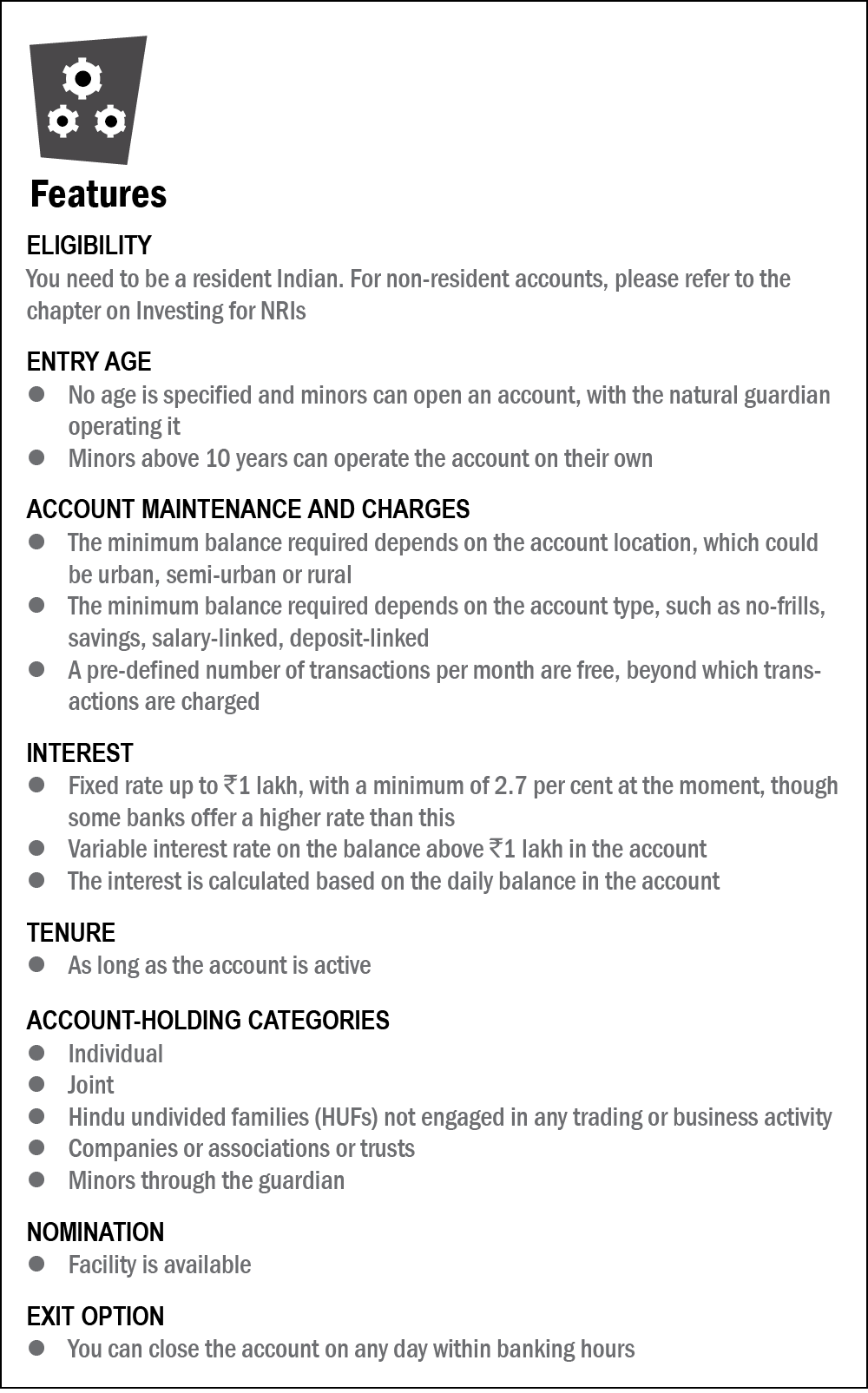

The interest rate in a savings bank is guaranteed up to the first Rs 5 lakh balance in the account. This rate varies across banks, since the Reserve Bank of India deregulated the savings bank deposit interest rate on October 25, 2011. Banks are now free to determine the interest on the balance in a savings-bank account, which has to be uniform for all types of accounts up to Rs 1 lakh but varies for the accounts with a higher balance.

Liquidity

The savings bank account is highly liquid and one can withdraw cash from one's account through a bank branch during banking hours. Today, automated teller machine (ATM) access is offered by most banks to savings-bank account holders. The ATM allows 24- hour withdrawals within limits on a single day. Various banks have declared that there will be charges on cash transactions and ATM withdrawals above a certain limit. This varies from bank to bank, hence needs to be checked with your bank. Apart from this, one can also transfer funds electronically through National Electronic Fund Transfer (NEFT), Real Time Gross Settlement (RTGS), Unified Payment Interface (UPI) and Immediate Payment Service (IMPS). While earlier NEFT and RTGS were available only during banking hours, both are now available round-the-clock on all days like IMPS, with effect from December 2019 and December 2020, respectively. This was a further step taken by the Reserve Bank of India (RBI) to boost digital payments after it waived off processing charges and time-varying charges levied on banks for transactions processed in RTGS and NEFT systems in July 2019.

For RTGS, the minimum amount that can be transferred is Rs 2 lakh. However, there is no such limit for NEFT and IMPS. There's no upper capping for both RTGS and NEFT transfer, while the same is Rs 2 lakh per transaction in the case of IMPS. Though NEFT and RTGS seem to be similar in the case of limits, they are different in terms of their processing. RTGS is faster and therefore generally used for high-value transactions.

Tax implications

Interest earned on the savings bank account up to Rs 10,000 per annum is exempt from tax under Section 80TTA. This section allows an income-tax deduction to an individual (up to 59 years of age) or a HUF for the interest earned on a savings bank account held with a bank, post office or a co-operative society. Interest amounts above this limit are treated as income and taxed accordingly. However, no Tax Deducted at Source (TDS) is taken from the same. The interest earned is taxable under the head 'income from other sources'. Similar tax benefits are available to senior citizens under Section 80TTB which offers some additional perks. This section gives respite from income-tax on interest earned on all types of deposits (including fixed deposits) up to Rs 50,000 per annum.

Banking on the move

The advent of mobile telephone has touched our lives like never before. Today, banks are making it easier than ever before for account holders to access account information on their mobile devices. Some banks are offering new services or improving existing ones that allow people to access their accounts while on the go.

You can access your bank account through your registered mobile phone number with your bank. The features offered in mobile banking are of two types: one where your bank sends you mobile updates and the second, where you send a request, such as a money transfer, which the bank acknowledges.

With evolving technology and improving mobile handsets, banks are creating software for the mobile-banking interface, opening yet another window to banking. Now you can download the application (app) of your bank and do all sorts of transactions on your mobile or tablet.

This article was originally published on December 07, 2021.

Ask Value Research ![]()