In the previous two articles of the series, we talked about the importance of setting your asset allocation back on track and the need to prune the mid and small cap allocations in your portfolio. Now comes the third step that investors usually defer but should not - switch to direct plans.

Go direct

We have said this repeatedly but perhaps, in the current market scenario, when the returns of debt funds have been falling, it has become even more imperative for a debt-fund investor to switch to the direct plan.

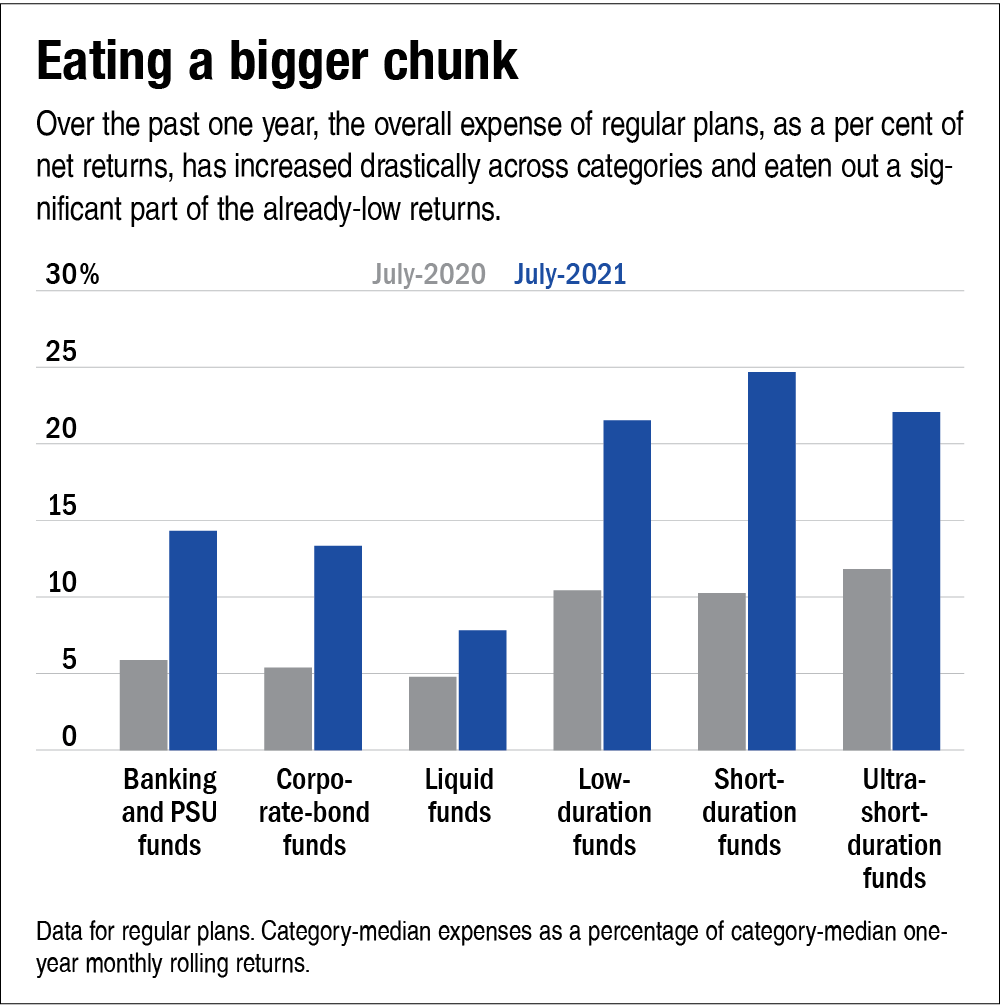

Returns of fixed-income funds have nosedived, owing to falling interest rates, even though expense ratios have remained flat over the last year. As a result, expenses have started consuming a more significant chunk of the returns of these funds. The problem is acute in regular plans where expense ratios now account for as much as 20 per cent of the returns in some debt categories.

The graph titled 'Eating a bigger chunk' sheds light on this issue. Undoubtedly, it is not a pretty sight for any fixed-income investor.

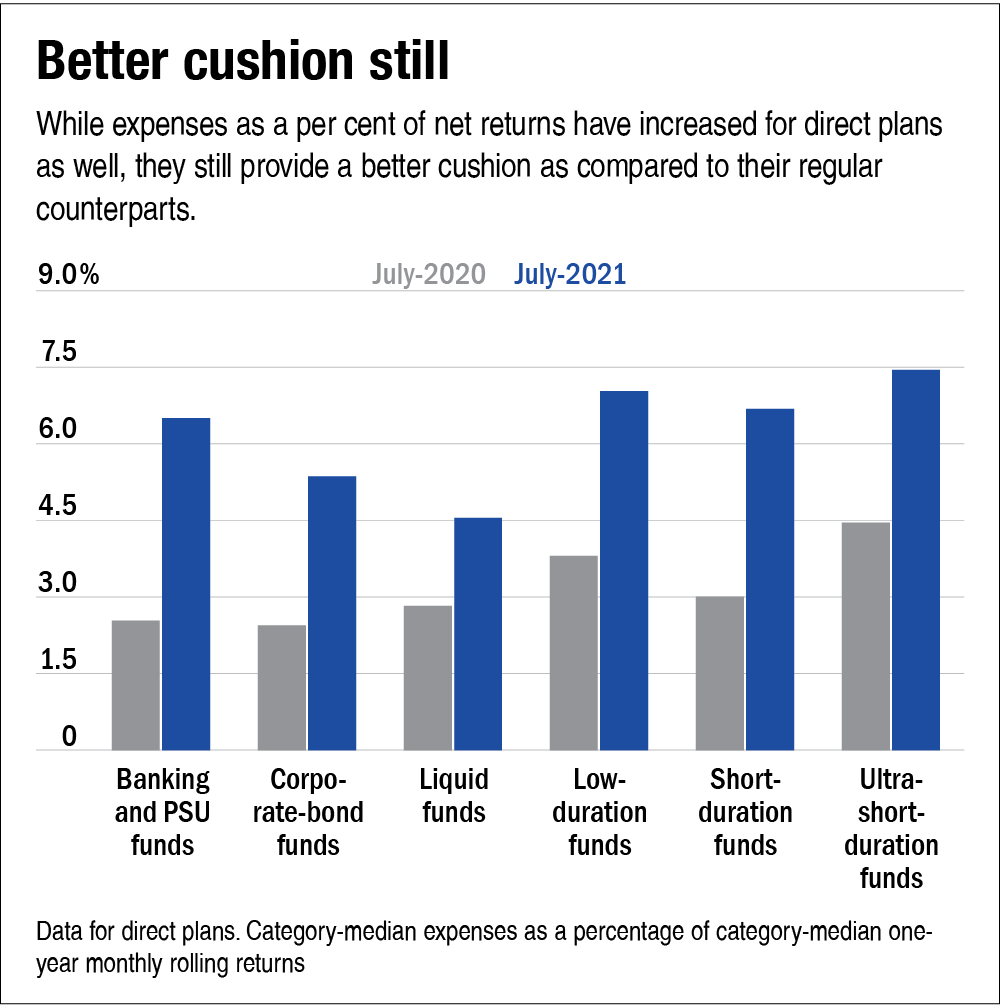

Although direct plans have also been facing the brunt, the impact has been less severe, providing more comfort to investors (see graph 'Better cushion still').

These expenses hurt a lot at a time when your fund can barely generate 5 per cent. While you can't do much about returns, you can lower expenses (which improves your returns by 10-15 per cent or more) by switching to direct plans. We believe it is a very sensible move for any investor who can transact online and the time has come now.

What about the tax incidence?

Some investors are reluctant to make changes to their portfolios, as it can evoke a tax liability. While taxes are an important consideration and you should not saddle yourself with them unnecessarily, don't let it be a deterrent to setting your house in order. The rewards of a disciplined investing approach and periodic rebalancing will outweigh the costs in terms of taxes.

Moreover, by not acting, you are, at best, deferring taxes but you cannot wish them away. At some point in time, you will need to sell your investments and pay your taxes. Thus, it is better to pay your taxes and keep your portfolio aligned with your investing needs rather than deferring this, thereby assuming a higher risk.

In fact, while switching from regular to direct plans, you may incur a one-time tax but you will end up saving recurring costs, which can add up to much more over a long holding period. So, don't let taxes be an impediment to fine-tuning your investments.

Ask Value Research ![]()