Mr Gupta has recently retired and has already made significant investments in governmentbacked guaranteed return schemes, including Senior Citizen Savings Scheme (SCSS) and Pradhan Mantri Vaya Vandana Yojana (PMVVY). He still has about Rs 30 lakh to invest but is not sure about where to invest the amount.

At present, he is contemplating investing in credit-risk funds, as other categories of debt funds have been giving quite low returns lately. He is also lured by certain debentures, giving returns in the range of 8-9 per cent and wants to know whether he should invest in them.

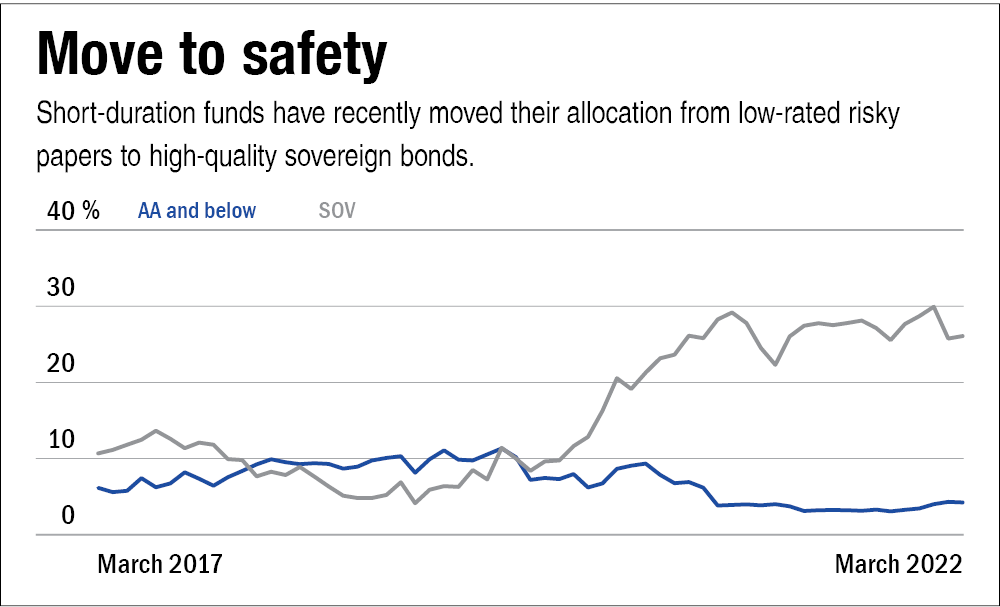

Subdued returns of short-duration funds

- Returns from short-duration funds and other fixed-income categories, barring credit-risk funds, have fallen lately.

- The short-duration category was hit hard in the aftermath of the IL&FS crisis and is currently playing it safe, with most of the funds avoiding credit calls and investing in top-rated assets. Given the risk aversion that we have been seeing since the pandemic began, funds under the category have shifted to quality papers. So, these funds have raised their sovereign exposure, while their exposure to lower-rated papers has been comparatively muted.

- Besides the category's shift to a low-risk strategy, the recent rate-hike by RBI has also impacted its returns. And more rate-hikes are expected in the near future.

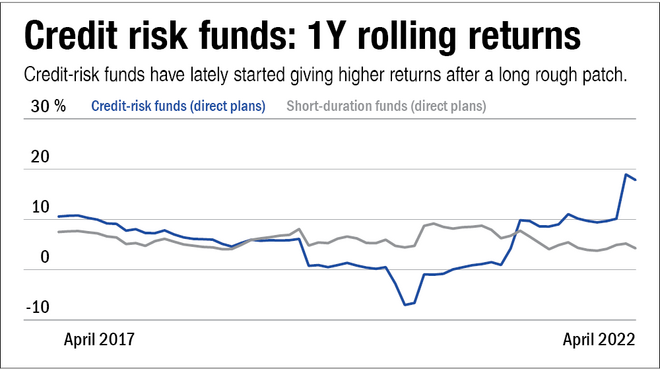

Credit-risk funds are, well, risky

- While these funds faced redemption pressure in 2020, they have now stabilised and started getting some traction from investors. Probably, this is because they are giving much higher returns these days than any other debt-fund category.

- Higher returns ultimately translate into higher risks. These funds are mandated to invest at least 65 per cent of their portfolio in less than top-rated papers.

- Such instruments have a higher credit risk in terms of a default by the company while repaying the principal or the interest payment. Credit-risk funds have suffered over the past couple of years because of such defaults.

- Sovereign debt instruments are issued by the government and carry the least risk, followed by the debt instruments with AAA, A1 and AA+ ratings, which are generally considered top-rated debt papers.

- The credit quality break-up of any fund can be accessed in the 'Portfolio' section of the fund page on Value Research Online.

- Mr Gupta should understand the risky nature of credit risk funds and should ideally avoid them. Further, he should accept the reality of low market yields.

- These bonds were launched last year in replacement of RBI's taxable bonds that offered a fixed rate of interest. While these bonds are currently fetching 7.15 per cent per annum, the interest rate is set to revise every six months - in January and June. By design, it would be kept 35 basis points higher than the prevailing returns offered by the National Savings certificate. Interest is paid out semi-annually.

- As they are issued by the Government of India, the risk is negligible and can be a good alternative for Mr Gupta or any other fixed-income investor.

- While the interest income from RBI bonds is added to the income for the taxation purpose, Mr Gupta's collective income from his investments in SCSS, PMVVY and RBI bonds is likely to remain below Rs 5 lakh and hence, he does not need to worry about taxation. Senior citizens are also eligible to claim a deduction of up to Rs 50,000 on the interest income from deposits and savings account under Section 80TTB of the Income Tax Act.

- However, Mr Gupta must note that these bonds score less on liquidity. These bonds have a tenure of seven years and premature withdrawals are allowed only after the stipulated lock-in period, which is decided based on the age of the subscriber - six years for the age group of 60-70 years; five years for the age group of 70-80 years; and four years for the age group of 80 years and above. Also, these bonds are not traded in the secondary market.

Consider target-maturity funds

- To supplement the returns of high-quality short-duration funds, one can also look for alternatives like target maturity funds, which aim to capture the yields on specific maturity segments.

- These are high-quality funds that follow a roll-down maturity style. So, the fund manager sets a maturity target at the outset and the maturity rolls down over a period. Therefore, the interest-rate risk reduces. So, these funds can be useful amid a rising-rate scenario. Further, the visibility of returns is a big plus here.

Don't shun equities

- While the current interest income may suffice Mr Gupta's income requirement, it may not be the case after five or 10 years because of the rising inflation.

- Investing in equity is the only way to get inflation-beating returns and therefore, Mr Gupta must allocate at least one third of his corpus to equities. However, it should not be invested at one go but over a period of time, say, the next 18 to 24 months.

- Further, it is recommended that Mr Gupta should not make an annual withdrawal of more than 4-6 per cent of the total retirement corpus.

Don't ignore these

- Emergency fund: Keep money equivalent to at least six months of expenses in a sweep-in deposit or a good liquid fund.

- Insurance: Buy an adequate health cover. You don't need life insurance in the absence of financial dependents or if you have sufficient net worth.

This article was originally published on September 03, 2021.

Ask Value Research ![]()