Chemplast Sanmar is a speciality chemical manufacturer in India focusing on speciality paste PVC resin and other custom chemicals for pharmaceutical and agro-chemical companies. The company is one of the leading manufacturers of specialty paste PVC resin, which is primarily used in manufacturing leather cloth. This product has no major substitute, which gives the company a cutting edge over the others. CSL is also the third-largest manufacturer of caustic soda and the largest manufacturer of hydrogen peroxide in the South India region. Apart from this, the company also manufactures Chloromethanes and Refrigerant Gas.

It has four manufacturing facilities, three in Tamil Nadu and one in Puducherry. In March 2021, the company acquired 100 per cent equity interest in Chemplast Cuddalore Vinyls Limited (CCVL), which was earlier demerged from the company in FY18. CCVL is the second-largest manufacturer of suspension PVC resin in India and the largest in the South India region, with an installed capacity of 300-kilo tons per annum.

Strengths

- The company is part of the Sanmar Group, which is among the oldest and most prominent corporate groups in the South India region and helps give the company its patronage. 'Fairfax India Holdings,' a well-known international investment firm, has been invested in the group since 2016.

- The India market for speciality paste PVC resin is highly underpenetrated compared to other developing and developed economies. India imports almost half of its demand from global manufacturers. Thus, the company is also planning to add 35-kilo tons capacity for speciality paste PVC resin, which is expected to come onstream in FY24.

- Speciality chemicals have high entry to barriers, especially in custom manufacturing for pharmaceuticals and agro-chemicals.

- The company is vertically integrated. This means it manufactures the raw material used in speciality paste PVC resin, reducing its dependence on external suppliers and controlling costs.

Risks

- As of March 31, 2021, the company had total outstanding borrowings of Rs 2,017 crore, and the lenders have imposed restrictive conditions which limit the flexibility in planning for the business.

- Before the IPO, 26 per cent of the total share capital held by the promoter was pledged, which has been released to facilitate the IPO offer.

- The entire share capital of its subsidiary CCVL is pledged to secure certain financing facilities.

IPO questions

Company/business

1. Are the company's earnings before tax more than Rs 50 cr in the last twelve months?

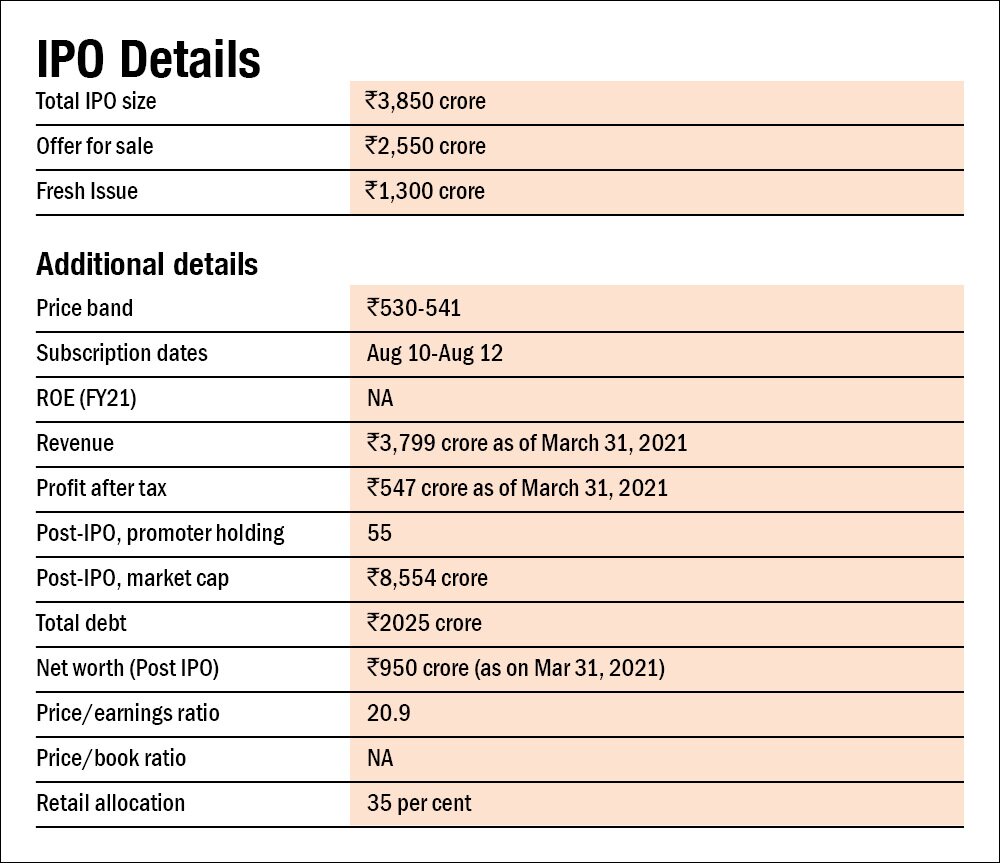

Yes, the company reported earnings before tax of Rs 413 crore in FY21.

2. Will the company be able to scale up its business?

Yes. The domestic speciality chemical industry is expected to grow at a rate of 5-6 per cent between 2015 to 2020, as per a CRISIL report. This will be driven by rising domestic consumption, increasing exports, and government initiatives such as 'Make in India.' The company has also planned to increase its speciality paste PVC resin capacity by another 35-kilo tons, which will be onstream by FY24.

3. Does the company have recognisable brand/s, truly valued by its customers?

No, speciality chemicals are intermediaries used in manufacturing other products. Thus, the presence of highly recognised brands is limited.

4. Does the company have high repeat customer usage?

Yes, the company generated 38 per cent of its revenues from its top 10 customers. However, it does not have a firm commitment in the form of long-term supply agreements with its key customers.

5. Does the company have a credible moat?

Yes, the company manufactures different speciality chemicals and is amongst the leading manufacturers in almost all of them.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No, as the company is engaged in the manufacturing of chemicals which attracts lots of key regulations such as the Indian Boilers Act, Explosives Act, and Drugs and Cosmetics Act, to name a few.

7. Is the business of the company immune from easy replication by new players?

Yes, the manufacturing of speciality chemicals has high entry barriers, especially in speciality paste PVC resin, which will benefit the company in the medium term.

8. Is the company's product able to withstand being easily substituted or outdated?

Yes, speciality chemicals cannot be easily substituted with other alternatives like speciality paste PVC resin.

9. Are the customers of the company devoid of significant bargaining power?

No, the company typically plans and incurs capital expenditure against the orders placed by its customers. However, it does not have any long-term contracts, nor could it negotiate for more favourable terms.

10. Are the suppliers of the company devoid of significant bargaining power?

No, the company depends on foreign suppliers for its raw materials, which constituted more than 94 per cent of its total raw material, attracting a variety of risks and uncertainties.

11. Is the level of competition the company faces relatively low?

No, the Indian chemicals market is fragmented, and the company competes with large Indian companies. However, in some segments, such as speciality paste PVC resin, the company faces relatively low competition.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes, the company's promoter will continue to hold 55 per cent stake in the company post-IPO.

13. Do the top three managers have more than 15 years of combined leadership at the company?

Yes, the Executive Director (Commercial), N Krishnamoorthy, has been associated with the company since 1993.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with Sebi guidelines?

Yes, we have no reasons to believe otherwise.

15. Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

No, there are a couple of criminal litigations involving the company's director, and the matters are currently pending.

16. Is the company's accounting policy stable?

No, the company's statutory auditors have included an emphasis of matter against the consolidated financial statements of FY21 and FY20 for the impact of COVID-19 pandemic on carrying value of assets.

17. Is the company free of promoter pledging of its shares?

Yes. Currently, the promoters' shares are free of pledging, but the promoters have agreed to pledge 25 per cent shares of pre-offer share capital upon the occurrence of certain trigger events.

Financial

18. Did the company generate current and three-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

No, the company had reported negative equity as on March 31, 2021. However, post the acquisition of CCVL, the company has reported 50.6 per cent ROCE in FY21 and a three-year average ROCE of 22.7 per cent.

19. Was the company's operating cash flow positive during the three years?

Yes, the company reported positive cash flows from operating activities in the last three years.

20. Did the company increase its revenue by 10 per cent CAGR in the last three years?

Yes, the company's revenues grew at a CAGR of 74 per cent between FY19 to FY21, but that has come on back of its acquisition of its subsidiary, which is one of the major contributors to its business.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest coverage ratio more than 2?

No, the company has reported negative equity in FY21 and has an interest coverage ratio of 1.9 times.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

No, the manufacturing of chemicals has large working capital requirements. Also, the company has large trade payables out of which Rs 1,650 crore has to be paid in the next one year.

23. Can the company run its business without relying on external funding in the next three years?

Yes, the company plans to pay off its debt using the proceeds from the IPO, which will reduce its finance cost, leading to an increase in profitability. This, along with positive cash flows from operations, will help it tide without relying on external funding in the near future.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15%)?

Yes, the company has reduced its short-term borrowing to Nil from Rs 153 crore in FY19.

25. Is the company free from meaningful contingent liabilities?

No, the company has reported Rs 49 crore of contingent liabilities against negative equity.

The stock/valuation

26. Does the stock offer operating earnings yield of more than 8 per cent on its enterprise value?

No, the company's stock will offer an operating-earnings yield of 2.6 per cent on its enterprise value.

27. Is the stock's price to earnings less than its peers' median level?

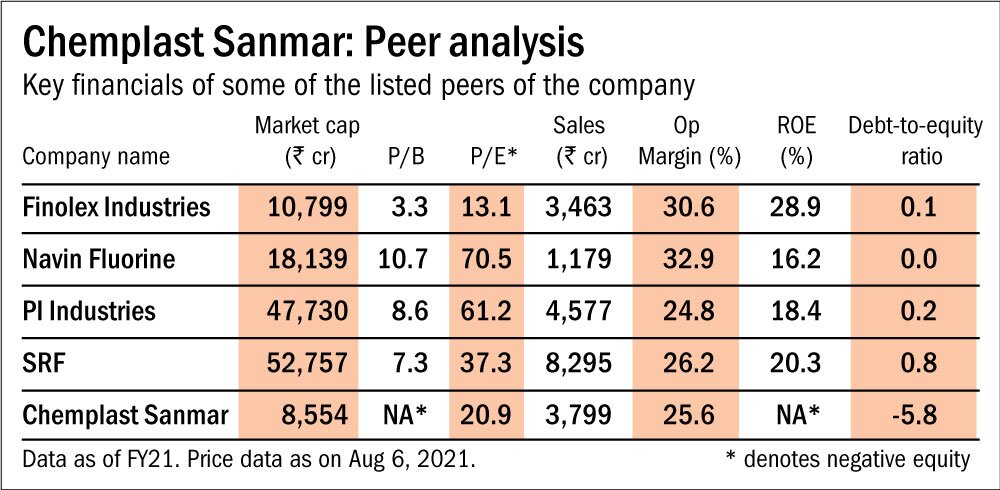

Yes, the stock's price-to-earnings ratio of 20.9 is less than its peers' median level of 37.3.

28. Is the stock's price to book value less than its peers' average level?

NA. The company has a negative book value as on March 31, 2021.

Disclaimer: The authors may be an applicant in this Initial Public Offering.

Disclaimer: This content is for information only and should not be considered investment advice or a recommendation.

For grievances: [email protected]

Ask Value Research ![]()