Glenmark Life Sciences is involved in the development and manufacturing of high-value, non-commoditised active pharmaceutical ingredients (APIs) - raw materials used in making medicines. The company has a portfolio of 120 products that have a market size of $142 billion. These products are used in various therapy areas, such as cardiovascular, central nervous system, diabetes, anti-infective and others. Besides, over the years, the company has scaled up its contract development and manufacturing operations (CDMO), accounting for around 8 per cent of the overall revenue in FY21. Currently, the company has a total capacity of 726.6 kilolitres (kl) across its four facilities located in Gujarat and Maharashtra.

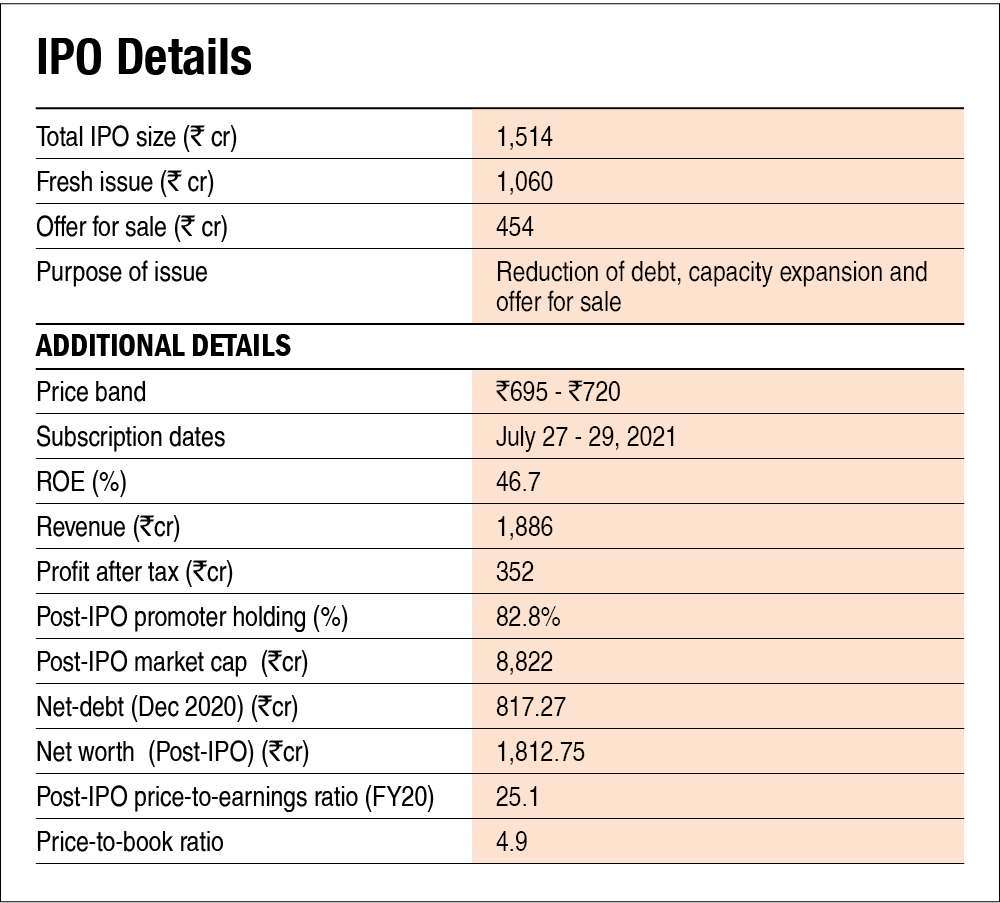

Glenmark Life Sciences is a wholly-owned subsidiary of Glenmark Pharmaceuticals. In 2018, it entered into a business purchase agreement with Glenmark Pharma under which its API business was spun off into the company for Rs 1,162 crore. Through the IPO, the company is raising around Rs 1,514 crore. Out of this, Rs 453 crore is for a fresh issue, Rs 800 crore will be used for paying off the debt against the above-mentioned business purchase agreement and around Rs 150 crore will be utilised for the expansion of its existing plants by 200 kl. Going forward, the management intends to grow its API business by introducing more molecules and expand its CDMO business for which it has planned the capacity expansion of 800 kl by the end of FY23.

The global API market was estimated to be around $181.3 billion in 2020. The US (35.1 per cent) and China (32.4 per cent) dominate the market, while India accounts for 6.1 per cent of it. At present, India imports around 68 per cent of APIs from China. However, to promote local manufacturing and cut this dependence, the government has announced various schemes and financial packages for the sector. The availability of skilled manpower, low operation costs and the government's focus on API manufacturing can act as growth catalysts for the sector.

Strengths

- Although the API business is a high-volume, low-margin business, Glenmark Life Sciences has built capabilities in niche and technically complex molecules, thereby commanding higher margins.

- The company has had long-term relationships with its customers. With its seven largest customers, its association has been for around five to 15 years.

- The company has more than 30 per cent market share in some of its key products, which together contribute around 44 per cent to the total API business.

- The company has a portfolio of 120 molecules with a total market size of $142 billion. Additionally, it has filed 403 Drug Master Files (DMFs) and has 39 patents granted (owned and co-owned).

Risks/weaknesses

- Around 40 per cent of the company's revenue comes from its parent company. So, it is quite dependent on the business of its parent company.

- The company's facilities are subject to time-to-time inspections from various pharma regulators such as the USFDA and others. Any adverse observation/import ban, etc., from these regulators can adversely affect the business.

- The company has a working-capital cycle of more than six months. As of FY21, around 10.2 per cent of its receivables were pending for more than 180 days.

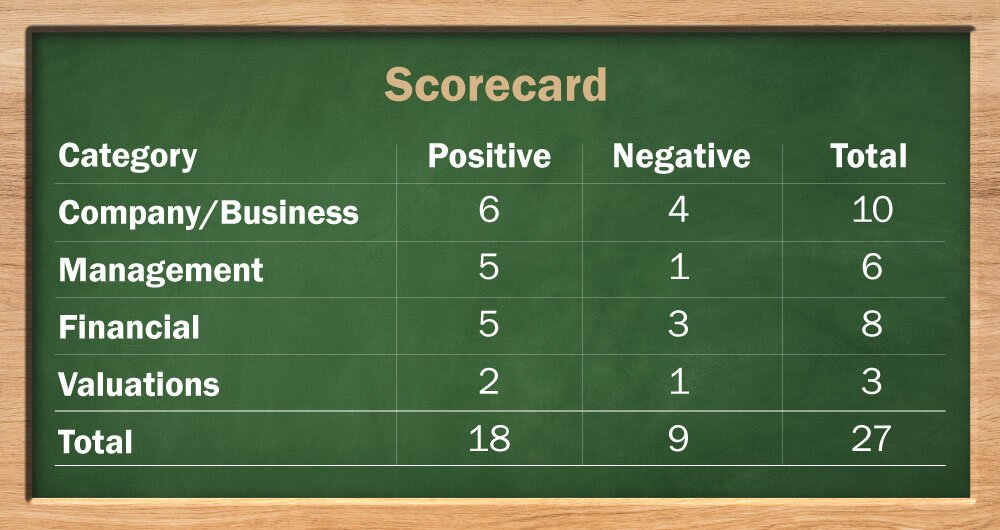

IPO Questions

The company/business

1. Are the company's earnings before tax more than Rs 50 cr in the last twelve months?

Yes, the company's profit before tax in FY20-21 was Rs 470.94 crore.

2. Will the company be able to scale up its business?

Yes. The company is increasing its API manufacturing capacity by 200 kl at its two existing plants. These will be brownfield expansion and should come up in a short period of time, as they won't require lengthy regulatory approvals. Additionally, the government's focus on cutting reliability on China for API imports is giving impetus to domestic manufacturers. Moreover, the company intends to scale up the CDMO business (8.1 per cent of FY21 revenue) by making further greenfield investments slated for FY23. These factors should help the company scale up its business.

3. Does the company have recognisable brand/s, truly valued by its customers?

Not applicable. The company sells active ingredients used as raw materials in medicines to other generic drug manufacturers. Since it's a B2B product, the concept of brand recognition isn't relevant.

4. Does the company have high repeat customer usage?

Yes. For the last three years till FY21, around 69 per cent of the company's customers were repeat customers. Moreover, the company has had long-term relationships of around five to 15 years with the seven largest customers.

5. Does the company have a credible moat?

Yes. The company sells high-value non-commoditised APIs and as of FY21, it had a portfolio of 120 molecules. Its key products, which contribute substantially to its API business, have a market share of more than 30 per cent. Additionally, its facilities are approved by the USFDA and other regulatory bodies and since 2015, it has not received any warning letter or import alerts during 38 inspections. All these factors provide the company with a credible moat.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No. Active ingredients are like raw materials to any medicine and are of a highly critical nature. Therefore, API manufacturers are subject to inspections by various regulatory bodies like the USFDA and others. Additionally, post-COVID, governments around the world are wanting companies to move API manufacturing locally so as to cut reliance on international supply chains.

7. Is the business of the company immune from easy replication by new players?

Yes. Drug approvals are a lengthy and cumbersome process. Following the development of the drug, pharma companies have to file for approval with various regulatory bodies. For example, as of FY21, the company had 403 DMFs across various regulatory bodies. These processes require constant R&D efforts and are time-consuming, making them immune to easy replication by new players.

8. Is the company's product able to withstand being easily substituted or outdated?

Yes. The company produces APIs that are higher up the value chain and are non-commoditised in nature. Although the complexity of drugs produced keeps on increasing year on year, as such APIs are not expected to be substituted or become outdated.

9. Are the customers of the company devoid of significant bargaining power?

No. In FY21, the top five customers of the company accounted for 55.9 per cent of the revenue. Moreover, the promoter company (Glenmark Pharmaceuticals) accounted for 40.9 per cent of the overall sales. Such a high share of revenue concentration provides ample bargaining power to customers.

10. Are the suppliers of the company devoid of significant bargaining power?

No. For FY21, the top three suppliers of the company accounted for 40.3 per cent of the total purchase of the key starting material. Moreover, a significant portion of raw materials (39.6 per cent of the total raw material purchases in FY21) is imported from China. Since the company doesn't enter into any long-term contracts, its suppliers have significant bargaining power.

11. Is the level of competition the company faces relatively low?

No. The API market is a highly fragmented market with around 1,500 API manufacturing plants. As of 2017, the top 14-16 API players comprised just 16-17 per cent of the total market. The presence of several players and the fragmented nature of the sector make it highly competitive.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than a 25 per cent stake in the company?

Yes, the promoters will continue to hold more than 80 per cent stake in the company after the IPO.

13. Do the top three managers have more than 15 years of combined leadership at the company?

No. The current CEO joined the company in 2019, while the current CFO of the company joined in December 2020.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with Sebi guidelines?

Yes, we have no reasons to believe otherwise.

15. Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

Yes, we have no reason to believe otherwise.

16. Is the company's accounting policy stable?

Yes, we have no reasons to believe otherwise.

17. Is the company free of promoter pledging of its shares?

Yes, none of the shares held by the promoters is pledged.

Financials

18. Did the company generate the current and three-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

Yes. The current return on equity is 46.71 per cent and the average return on equity has been 74.6 per cent for the past three years. Similarly, the current return on capital employed has been 32.7 per cent, while the three-year average has been 27.22 per cent.

19. Was the company's operating cash flow positive during the previous three years?

Yes, The company's cash from operations was positive in all the previous three years.

20. Did the company increase its revenue by 10 per cent CAGR in the last three years?

Yes, the company has increased its revenue by more than 10 per cent in the last three years.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest-coverage ratio more than 2?

No. The company's net debt-to-equity ratio was at 1.09 times and its interest-coverage ratio was 6.8 times as on March 31 2021.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

No. The working-capital cycle of more than six months means that the company will need to rely on working-capital needs for day-to-day affairs.

23. Can the company run its business without relying on external funding in the next three years?

No. The company is planning a greenfield investment which will be commissioned by the end of FY23. Currently, the company is raising around Rs 152 crore for a 200 kl brownfield investment. It means that the company would need around Rs 600 crore or more investment for the 800 kl greenfield project, which can lead to rising external debt.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

Yes. The company only has a minuscule proportion of its debt as short-term borrowings.

25. Is the company free from meaningful contingent liabilities?

Yes, the amount of contingent liabilities on the company's book is not meaningful.

The stock/valuations

26. Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

No, the company's stock will offer an operating yield of 6.5 per cent on its enterprise value.

27. Is the stock's price-to-earnings less than its peers' median level?

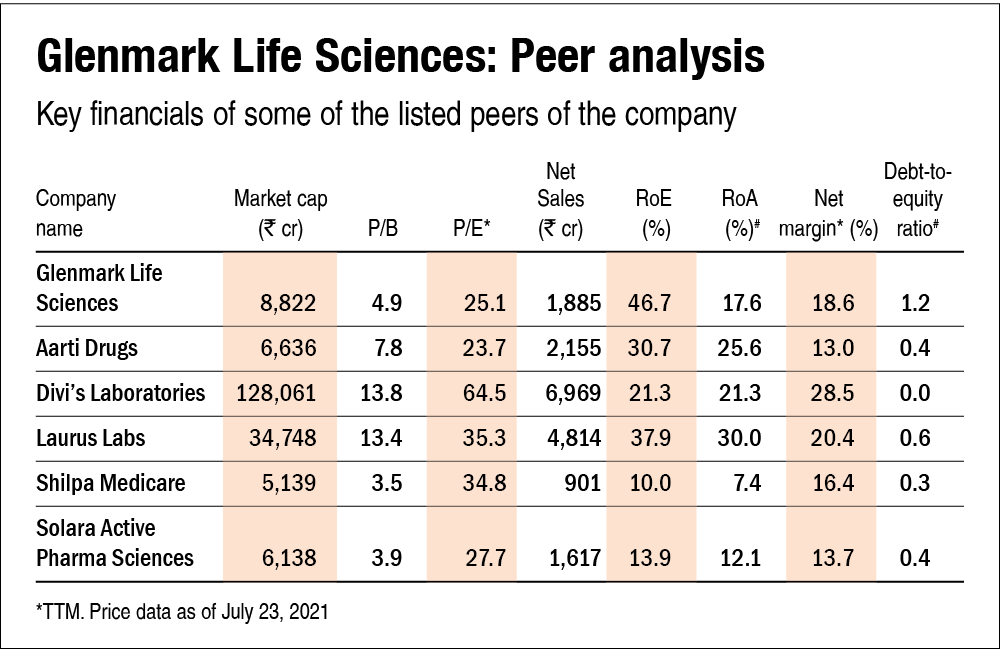

Yes, the company's stock would trade at a P/E of 25.1, which is lower than its peer's median level of 34.8.

28. Is the stock's price-to-book value less than its peers' average level?

Yes, the company's stock would trade at a P/B of 4.9, which is lower than its peer's average level of 8.5.

Disclaimer: The authors may be an applicant in this Initial Public Offering.

Ask Value Research ![]()