Incorporated in December 1995, G R Infra is an integrated road engineering, procurement, and construction (EPC) company with experience in designing and constructing various road/highway projects across 15 states in India. It has also recently diversified into projects in the railway sector. The company's principal business operations are broadly divided into three categories:

- Civil construction activities under EPC model

- Development of roads and highways under BOT (build, operate, and transfer) and HAM (Hybrid Annuity Model)

- Manufacturing bitumen, road-marking paints, electric poles, road signage, and fabricating and galvanising metal crash barriers.

Since 2006, the company has executed over 100 road construction projects and currently has six operational projects, four under construction and five yet to be commissioned. As of March 31, the company had a robust order book of Rs 19,025 crore.

Strengths

- Established track record of timely execution: The company has over 25 years of experience executing EPC projects in road construction. In the last three fiscal years, the company has completed more than 50 per cent of its projects well before the scheduled completion date.

- In-house integrated model: Its in-house resources include a highly skilled design and engineering team, manufacturing facilities for processing bitumen, thermoplastic road-marking signage, construction equipment, and transportation vehicles. As of March 31, their equipment base comprised over 7,000 construction equipment and vehicles.

- Experienced promoters and strong management team: The promoters have more than 25 years of experience in the construction industry and benefit from industry knowledge, expertise, and vision.

- Well-diversified order book: The company's order book stands at a book-to-bill ratio of 2.6 times which is in line with other listed road construction companies. It has orders from states across India, enabling the company to transform from a regional player to a pan-India presence.

Risks

- Out of the total bids submitted by the company during FY21, FY20, and FY19, they were awarded the projects in respect of 5.2 per cent, 6.1 per cent and 15.5 per cent of such bids respectively.

- Their business requires significant working capital to finance large projects to purchase or manufacture materials, mobilise resources, and work on projects before payment is received from the clients.

- The company's future growth plans include venturing into other sectors apart from their road infrastructure, which they are primarily engaged in.

IPO Questions

The company/business

1. Are the company's earnings before tax more than Rs 50 cr in the last twelve months?

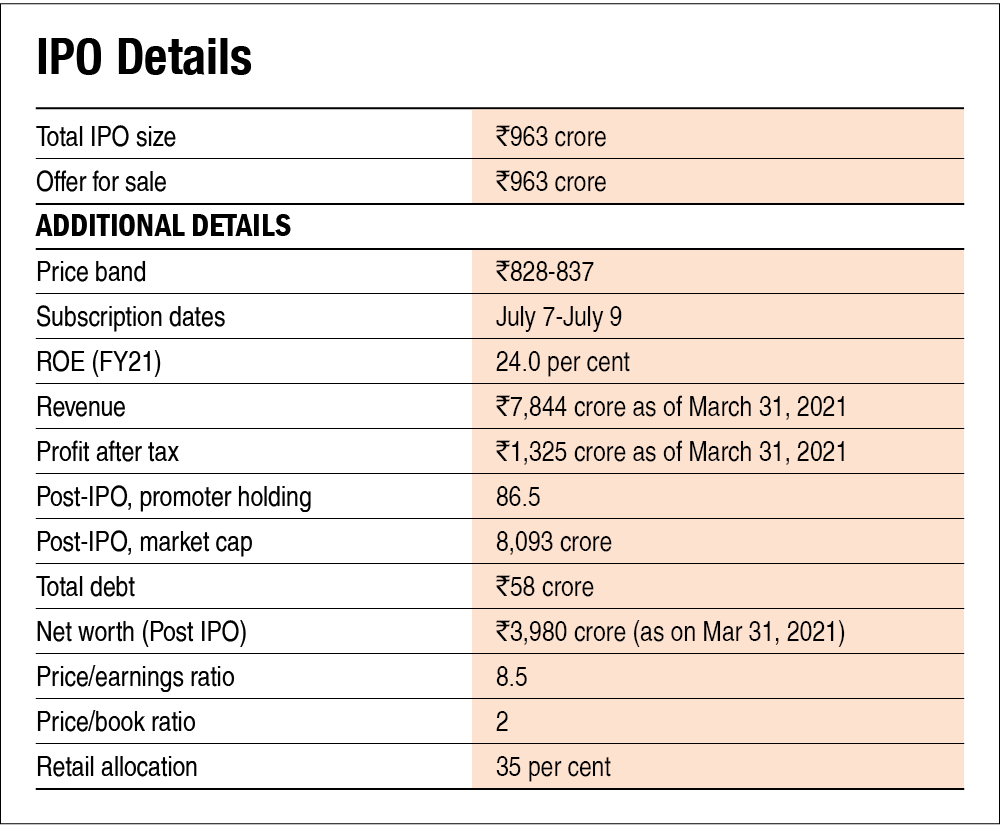

Yes, the company reported earnings before tax of Rs 1,325 crore in FY21.

2. Will the company be able to scale up its business?

Yes. The government's increased focus on the development of road infrastructure and record budget allocation towards infrastructure will allow the company to expand its business in India. As of March 31, 99.6 per cent of the company's order book was attributable to contracts awarded by government authorities.

3. Does the company have recognizable brand/s, truly valued by its customers?

NA, the company operates in the road construction business and does not have a recognised brand, and its customers include various government entities such as Central and State governments.

4. Does the company have high repeat customer usage?

Yes, the company derives a majority of its revenues from contracts from NHAI (National Highway Authority of India) and MoRTH (Ministry of Road Transport and Highways), which represent a large part of its order book.

5. Does the company have a credible moat?

No, the company operates in a highly competitive industry, and some of its competitors might have greater industry experience, substantial financial and technical expertise.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No, the company has to comply with various regulations such as the National Highways Act, National Highways Authority of India Act, and National Highways Fee Rules, to name a few.

7. Is the business of the company immune from easy replication by new players?

Yes. Operating in road infrastructure requires expertise and a large capital outlay which might restrict new players.

8. Is the company's product able to withstand being easily substituted or outdated?

No, the company's primary business activity includes road construction which cannot be differentiated.

9. Are the customers of the company devoid of significant bargaining power?

No, the company is awarded projects based on a bidding system. Thus, the customers of the company have significant bargaining power.

10. Are the suppliers of the company devoid of significant bargaining power?

No, the company's suppliers mostly include construction equipment and construction materials providers and have a large market to cater to.

11. Is the level of competition the company faces relatively low?

No, the company operates in a highly fragmented industry and faces stiff competition from other private players.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes, the company's promoters will continue to hold 86.5 per cent stake in the company post IPO.

13. Do the top three managers have more than 15 years of combined leadership at the company?

Yes, both the CFO and the President of the company have been associated with it since 2011.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with Sebi guidelines?

Yes, we have no reasons to believe otherwise.

15. Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

No, there is litigation against the company and its promoter to facilitate unlawful activities. The matter is currently pending.

16. Is the company's accounting policy stable?

Yes, we have no reasons to believe otherwise.

17. Is the company free of promoter pledging of its shares?

Yes, the promoter's stake is free of a pledge.

Financials

18. Did the company generate current and three-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

Yes. The last three-year average ROE and ROCE till FY21 stood at around 25 per cent and 31.5 per cent, respectively.

19. Was the company's operating cash flow positive during the three years?

No. The cash flow from operations has been negative in each of the past three years till FY21.

20. Did the company increase its revenue by 10 per cent CAGR in the last three years?

Yes. Revenues for the company increased by 21.8 per cent during FY19-21.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest coverage ratio more than 2?

Yes. As of March 2021, the net debt-to-equity ratio stood at 0.9, while the interest coverage ratio stood at 5.3.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

No. Company's operating cash flows have been negative for each of the past three years. Additionally, debtor days can be a huge pain for EPC players due to delayed payments. With net working capital days at around 64 days, the company will rely on working capital for running smooth day-to-day operations.

23. Can the company run its business without relying on external funding in the next three years?

No, the company's operations require raising funds for projects awarded; thus it will need to rely on external funding.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

Yes. Short-term borrowings for the company have been volatile, but during FY19-21, it increased by 6.5 per cent yearly.

25. Is the company free from meaningful contingent liabilities?

No. As per cent of equity as of FY21, contingent liabilities formed around 37 per cent, which is substantial.

The stock/valuations

26. Does the stock offer operating earnings yield of more than 8 per cent on its enterprise value?

Yes, the company gave an operating earnings yield of around 16 per cent based on its post-issue EV.

27. Is the stock's price to earnings less than its peers' median level?

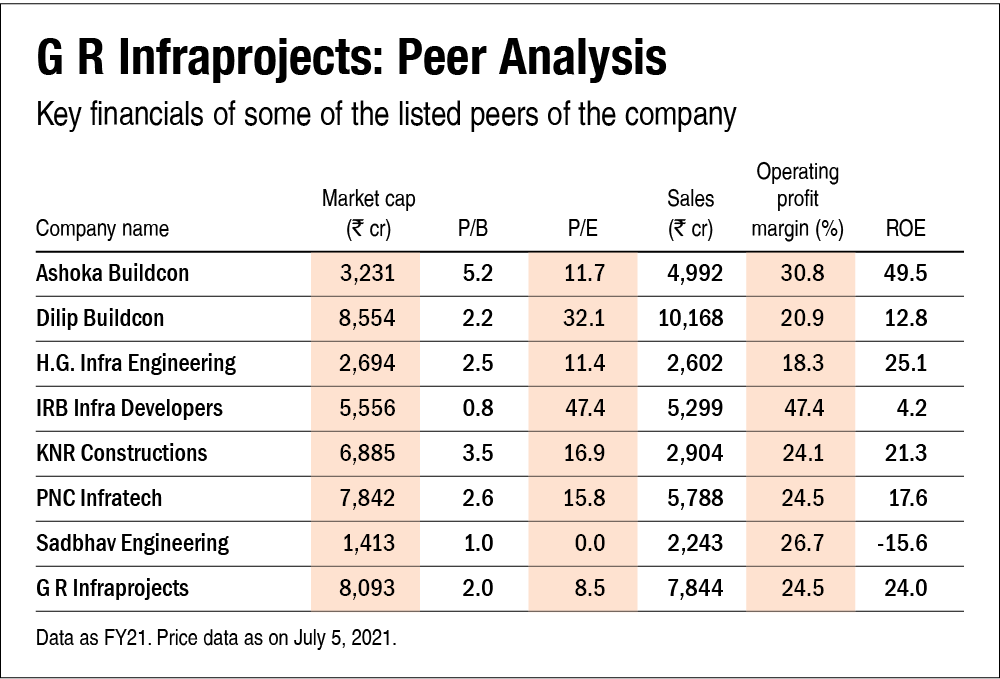

Yes, the company's stock would trade at a P/E of 8.5 which is lower than its peer's median level of 15.8.

28. Is the stock's price to book value less than its peers' average level?

Yes, the company's stock would trade at a P/B of 2, which is lower than its peers' median level of 2.5.

Disclaimer: The author may be an applicant in the IPO.

Ask Value Research ![]()