The trend of investing in funds with a target-maturity date has regained momentum. With yields heading northward since the start of the year, it's tempting to lock them and just sit back. Further, as rising yields are leading to a drop in the NAVs of mainstream open-end bond funds, AMCs are trying to shift the focus of investors to such funds, wherein interim movements in interest rates and NAVs don't matter much and this ultimately bring predictability to returns.

While AMCs seem to have a renewed interest in relaunching fixed-maturity plans (FMPs) after the debacle in 2019, this time they are also packaging target-maturity funds in the open-end avatar by structuring them as ETFs and index funds. Driven by the hope for predictable returns, decent safety, better liquidity and more tax efficiency, investors are considering these funds as an alternative to fixed-income instruments such as fixed deposits. So, should you also invest in target-maturity funds? Before we talk about that, let's first study their evolution.

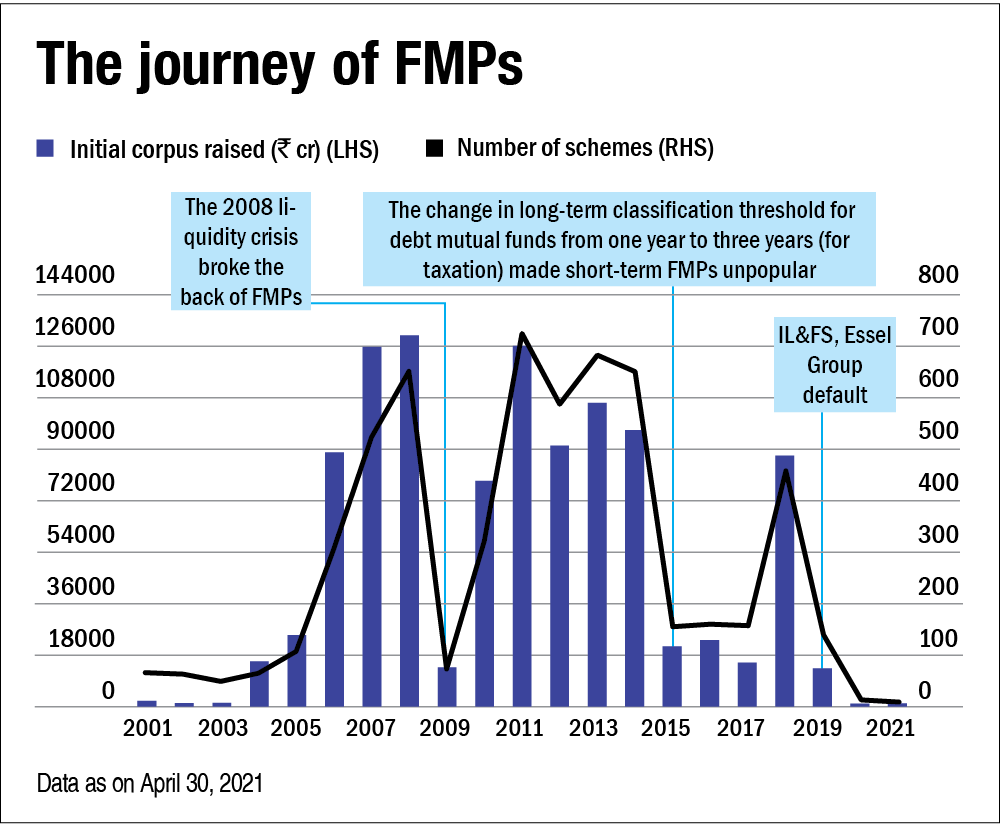

The rise and fall of FMPs

The predecessors of target-maturity funds are fixed-maturity plans (FMPs). FMPs primarily invest in debt securities that will mature in line with their own tenure. As the name suggests, these funds have a fixed maturity that can vary from a few months to a few years. On the due date, investors would get their principal back, along with the gains. By holding investments in such a fund till maturity, investors would get a return equal to the portfolio's yield to maturity (YTM) at the time of investment minus the expense ratio, no matter what happens to the interest rates subsequent to the date of investment. Although these funds are subject to NAV fluctuations in the interim, that may not be a concern as you are locked in till maturity. However, the risk of a default is always there.

FMPs have a closed-end structure. So, investors can buy the units only during the new-fund-offer (NFO) period. Once invested, you cannot redeem your units till maturity. As per the regulations, FMPs are listed on the stock exchange where investors can theoretically sell and buy them without impacting the fund flow for the fund house. But in reality, the low-trading volume of these funds makes them almost illiquid.

Over the years, FMPs gained popularity, as they were positioned as 'similar to FDs' but with better returns and better tax efficiency. However, this positioning suffered big setbacks on two occasions - in the 2008 credit crisis and again in 2019 during the IL&FS fiasco.

The 2008 financial crisis

Back then, FMPs had some structural flaws. They were not actually closed-end, as investors could exit by paying an exit load during the tenure of the fund. Also, the funds were allowed to invest in bonds with the maturity date longer than that of the scheme itself. They used to fund their obligation with the money flowing from the rollover of the scheme. The maturity of one FMP was followed by the issue of another one. There used to be a cycle of series and investors used to roll over their investments.

But this smooth journey was jolted when the entire financial market went haywire in 2008. Investors chose to exit in large numbers, even at a loss, which led to a liquidity crisis. There were no takers for the rolled-over FMP schemes either. Here is an extract from a cover story we did in November 2008, which was basically a transcript of a confidential conversation we had with a fund manager:

"Over the last 12 years, we have seen all kinds of crisis. They were predictable and we were able to gear up for them. This time when the systemic liquidity disappeared, it caught our portfolio managers unawares. We were not prepared for the six-sigma event. The liquidity crisis was genuine. We had three- to five-month maturity portfolios, but our investors could have taken the money out probably on a daily basis. Was this an error? Yes. Could we have predicted this? The answer is no. First it was a crisis of liquidity. Then, it became a crisis of confidence. The latter hurt more than the former. The real loss to investors has been on the FMP side. In a liquid fund, they got away at the NAV, which protected the capital and return. I think the FMPs are the only places where the investors have reacted in panic and taken away their money even at a loss. It is true that we have indicated a return based on certain portfolios, but that return holds only on maturity. It is not there for in-between periods. If the market has moved against us, then in no way I can protect the investors who are redeeming right now."

The 2008 crisis exposed serious cracks in the FMP structure and led SEBI to mend them. Redemptions from FMPs before the completion of the tenure were disallowed. Moreover, AMCs could no longer buy papers having the maturity longer than the fund itself. These important structural reforms made FMPs less susceptible to any external shocks. The category flourished in the subsequent years and the AMCs lined up hundreds of them year after year. But about a decade later, FMPs' reputation suffered a big blow when they hit the next big crisis in 2019.

The 2019 debt fiasco

Since FMPs invest predominantly in high-rated credit instruments, the risk of default is usually low. But in a bid to enhance yields, AMCs violated the principles of prudence and took concentrated exposure to certain issuers, most notably to riskier loans against shares. The crisis broke out when issuers like IL&FS, Essel Group and DHFL defaulted on their debt papers in 2019. While Kotak Mutual Fund repaid the principal and offered to pay returns later, subject to the realisation of debt, HDFC Mutual Fund took investors' permission to extend its maturity date by a year. Those who did not agree were paid less than their original capital. These were not the only AMCs whose FMPs got impacted.

These incidents hit investors like a thunderbolt. Initially, they were made to believe that FMPs were some sort of FDs that yielded better. But in reality, they were without their complete capital, let alone returns. The inherent risk was almost always ignored not just by investors but also by fund houses. These incidents raised questions about such riskier papers in FMPs which were supposed to give stable returns, their due diligence and delays in timely communication with investors. Further, this fiasco brought forth the notion that one should draw the line between guaranteed and indicative returns.

While the 2008 crisis had an element of externalities beyond an AMC's control, the 2019 debacle was largely a result of poor investment-management practices by fund companies. Needless to say, it earned FMPs a bad reputation. Investors with burnt fingers as well as those who saw others' fingers burning started to look away. After 2019, the number of new FMPs and the AUM raised dropped substantially. While the number of new schemes plummeted from 436 in FY2019 to just 50 in FY2020 and five in FY2021, the initial corpus raised fell from around Rs 67,174 crore to Rs 3,992 crore and Rs 1,175 crore, respectively.

But after a hiatus of two years, AMCs seem to be trying to revive the fortunes of target-maturity funds in old as well as new avatars. In Part 2, we would cover what this new avatar is and whether they make any investment case for you.

You can read the next part here.

Ask Value Research ![]()