In the first part of this article, we saw the historical background of target-maturity funds and how they became unpopular owing to some major setbacks in the past. Here is how fund houses seem to be repackaging target-maturity funds in old as well as new avatars, how do they differ and should you invest in them.

The resurgence of target-maturity funds

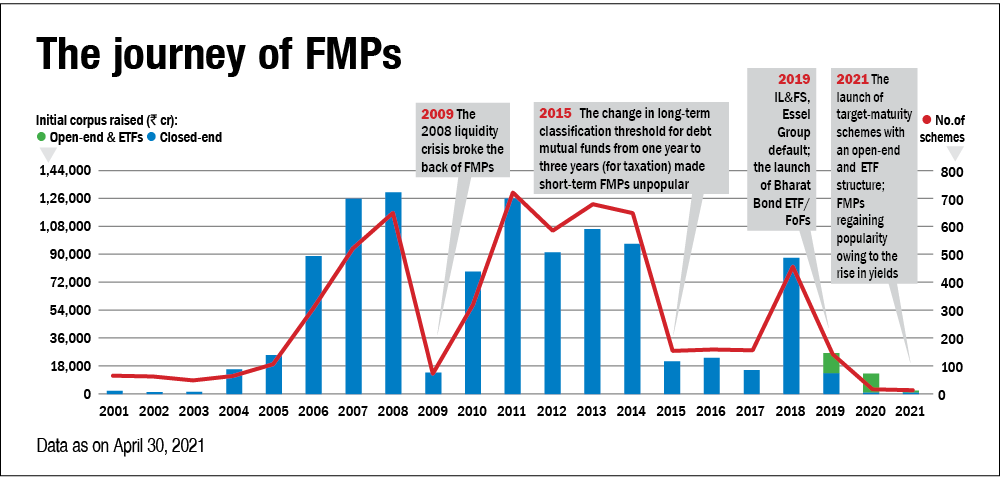

With a rise in bond yields in recent months, AMCs have lined up their FMPs for SEBI's approval. While eight such schemes have already been launched in CY2021, at least 19 others from seven AMCs are awaiting approval, as per the offer documents filed on SEBI's website, and more fund houses may follow suit. Besides, AMCs are restructuring target-maturity funds as ETFs/index funds.

These new avatars are passively managed and invest in similar-maturity securities that the fund's benchmark index contains. Thus, a 2026 fund holds bonds with the maturity lying somewhere around 2025-2026. On the due date, investors will get their principal back, along with the gains just like their earlier version. Currently, the maturity periods of these bonds are ranging between five to seven years. Most of the recently launched target-maturity funds invest in government securities, PSU bonds and state development loans (SDLs) with a pre-defined maturity period. Some invest in corporate bonds, too. They are available in both open-end and ETF structures to give liquidity to investors.

It is pertinent to note that this is not the first time such bond schemes are available to investors. In December 2019, the Government of India had launched Bharat Bond ETF, which is managed by Edelweiss Mutual Fund. It isalso a passively managed debt fund which invests in AAA PSU bonds with the maturity aligned with the scheme's term. To cater to non-demat account holders, it is also available in the form of fundof funds (FoF). And its success in raising a big sum of money from investors has perhaps inspired fund houses to come up with similar schemes.

Should you invest in them?

Target-maturity funds appeal to those investors who want to invest for a fixed tenure that matches with that of a fund and who want slightly higher returns than a bank FD with some degree of predictability. Their superior taxation as against a fixed deposit further enhances their post-tax returns. Moreover, the current crop of target-maturity funds is mandated to invest predominantly in government securities, SDLs and PSU bonds, which ranks them fairly low on the possibility of any defaults. But their big selling point lies in their ability to take the interest-rate worries out of the equation as they follow a roll-down strategy.

So, should they have a place in a fixed-income investor's portfolio? Well, these funds make most sense when interest rates are at or near their peak. That allows investors to lock in a high yield through a target-maturity fund and then sit back through the tenure of the fund. But in the current scenario, that is not the case. In fact, the interest rates on short-term debt instruments have been at their historic lows, as the RBI has cut the rates substantially in response to the pandemic over the last year. The rates slightly higher up the yield curve (in the five-six-year bracket or thereabouts) look attractive relative to shorter-term rates and that's why many recently launched funds have chosen that maturity range as their target. But we are nowhere close to the peak. The interest rates have bottomed out. While nobody can say when we start seeing a reversal, the only way from here on is up. And as and when the RBI starts hiking them, there will be an opportunity loss for those who lock themselves into target-maturity funds for the next several years at the current levels.

Moreover, remember that core fixed-income products, such as short-duration funds and corporate-bond funds, should still be at the heart of your fixed-income allocation. These funds benefit from a rising interest-rate scenario on two counts. First, because of the shorter maturity profile, the adverse impact of the rise in interest rates on their returns is lower. Secondly, because of their short-maturity profile, the portfolio comes up for re-investment sooner and gets redeployed at better yields in a rising interest-rate scenario. For example, let's say your short-duration fund holds a bond maturing in a year's time. Now one year down the line, if the interest rates increase; the maturity proceeds from this bond will get re-invested at higher rates, thereby benefiting investors.

Short-duration funds are low on risk and have delivered pretty decent returns over entire interest-rate cycles. Besides, given the kind of yields that the recently launched target-maturity funds are likely to deliver (in the 6-6.5 per cent range), we think that short-duration funds can be reasonably expected to deliver similar or better returns over the entire tenure of such funds. Therefore, while target-maturity funds have some appeal from the perspective of predictability for those investors looking for a fixed-investment tenure, we believe that categories like short-duration funds and corporate-bonds funds should still be at the core of a fixed-income investor's portfolio.

FMP or target maturity ETF/index fund - which one's better?

Both FMPs and target-maturity ETFs/index funds are conceptually similar as they build a portfolio based on a target-maturity period and roll down the maturity to zero as the target date approaches. Both have a finite life, at the end of which they cease to exist and money is returned to investors. However, the advantage of the ETF/index variant is that since it is mandated to invest in the stated index, the portfolio constituents are known upfront to investors.

Despite that, we believe that FMPs are structurally superior. That's because they are truly closed-end, a key ingredient for the predictability of returns. In the case of index funds/ETFs, their liquidity is often seen as an advantage but in a target-maturity strategy, that can adversely impact the predictability of returns. That's because the interim inflows and outflows would be invested at the then prevailing yields and this could dilute the dependability of the expected return.

The ETF structure addresses this to an extent, as the buying and selling of units on the stock exchange take place between investors and there are no inflows and outflows from the fund. But even in an ETF, units can be created or redeemed in pre-defined lot sizes and this can result in fresh money coming in or going out of the scheme. In extreme situations, the liquidity itself can lead to a crisis, as happened to FMPs in 2008, when they used to offer interim redemptions. So technically, FMPs are much better on this front, as their closed-end structure ensures money remains invested throughout the tenure and that adds to the predictability of returns. Of course, they suffered owing to poor investment decisions in the recent past but hopefully, the lessons have been learnt.

Ask Value Research ![]()