Incorporated in 1995, Dodla Dairy is an integrated dairy company based primarily in south India. The company is the third largest in terms of milk procurement per day, with an average procurement of more than 1.03 million litres of raw milk per day. It is also the second largest in terms of market presence, with operations expanding to the states of Andhra Pradesh, Telangana, Karnataka, Tamil Nadu and Maharashtra. The company is engaged in the business of selling fresh milk, which accounts for more than 75 per cent of its revenue and the rest comes from other dairy-based value-added products such as curd, ghee, butter, flavoured milk and ice cream amongst others.

The company's operations are carried out in 13 processing plants which have an aggregate installed capacity of 1.70 million litres per day. Dodla dairy procures its milk from more than 1 lakh farmers through 6,771 village level collection centres, 232 dairy and third-party suppliers. The company products are mainly marketed under the brand name of 'Dodla', 'Dodla Dairy' and 'KC+'

Strengths

- The company generates majority of its revenues from selling processed milk, which helps it generate high return of capital employed (ROCE), as compared to value-added products. Value-added products require high capital investment, thus generating lower ROCE However, these products generally have higher margins as compared to milk. Milk, on the other hand, has low shelf life, which allows quick realisation for its sales.

- Dodla Dairy has a strong distribution and marketing channel. Its products are distributed through 40 sales offices, 3,285 distribution agents, 861 milk distributors and 544 milk product distributors. The company also operates franchise-model based 'Dodla Retail Parlours' for selling its products.

- The company has delivered strong financial performance, increasing its topline at a rate of 14.1 per cent annually from FY17 to FY20.

- The company focuses on long-term relationships with its farmers through various initiatives. It provides in-house manufactured cattle feed to its farmers.

Risks

- India is the largest producer of milk in the world with a very large and fragmented market. The company faces stiff competition from unorganised players, other private players and co-operative societies. These co-operative societies are provided with government grants and subsidies, which pose a major threat to the company's procurement as these societies can offer higher procurement prices.

IPO Questions

Company / Business

1. Are the company's earnings before tax more than Rs 50 cr in the last twelve months?

Yes, although the TTM (trailing twelve months) numbers are not available, the company has reported earnings before tax of Rs 162 crore in nine-month period ending December 31, 2020.

2. Will the company be able to scale up its business?

Yes, the Indian dairy industry has grown at a CAGR of 10 per cent between FY15 to FY21 and is expected to grow at a similar rate of 10-11 per cent CAGR over FY21 to FY25. This is due to various factors such as rising preference for processed, hygienic and packed milk, rising importance of dairy products as a prominent source of proteins for the vegetarian population and continued government initiatives towards this sector.

3. Does the company have recognisable brand/s, truly valued by its customers?

Yes, the company sells and markets its products under the brand 'Dodla Dairy', 'Dodla', and 'KC+' in India.

4. Does the company have high repeat customer usage?

Yes, when it comes to staple foods, consumers tend to stick with brands rather than switching on a regular basis.

5. Does the company have a credible moat?

No, the company is into milk and dairy products, operating in a very fragmented and competitive market. It does not have a credible moat to protect its business.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

No, the company has to comply with various regulations such as the Food Safety and Standards Act and various state-based agriculture laws.

7. Is the business of the company immune from easy replication by new players?

Yes, the company has a vast milk procurement and distribution channel, which won't be easy to replicate for a new player.

8. Is the company's product able to withstand being easily substituted or outdated?

No, the company faces stiff competition from other private and listed players offering similar products.

9. Are the customers of the company devoid of significant bargaining power?

No, the dairy industry is highly competitive in India and consumers have a lot of other options to choose from.

10. Are the suppliers of the company devoid of significant bargaining power?

No, the suppliers of the company mostly include farmers who can choose to sell to other competitors as the company does not have any formal contracts for their supplies.

11. Is the level of competition the company faces relatively low?

No, the company operates in a highly fragmented industry and faces stiff competition from other private players and co-operative players.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes, the promoters of the company will continue to hold 64.17 per cent stake in the company on post-IPO basis.

13. Do the top three managers have more than 15 years of combined leadership at the company?

Yes, the CEO of the company, Mr Venkat Krishna Reddy, has been associated with the company for more than 23 years.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with Sebi guidelines?

Yes, we have no reasons to believe otherwise.

15. Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

No, there are several proceedings against the promoters of the company for violations under the Minimum Wages Act.

16. Is the company's accounting policy stable?

No, the statutory auditors of the company have made certain qualifications on the financial statements of the company for the last three fiscal years and nine-month period ending in December 2020. These pertained to irregular deposits of professional tax and breach of financial covenants (ratios) required to be maintained in terms and conditions of using debt facilities.

17. Is the company free of promoter pledging of its shares?

Yes, the promoter's stake is free of pledge.

Financial

18. Did the company generate current and three-year average return on equity of more than 15 per cent and return on capital of more than 18 per cent?

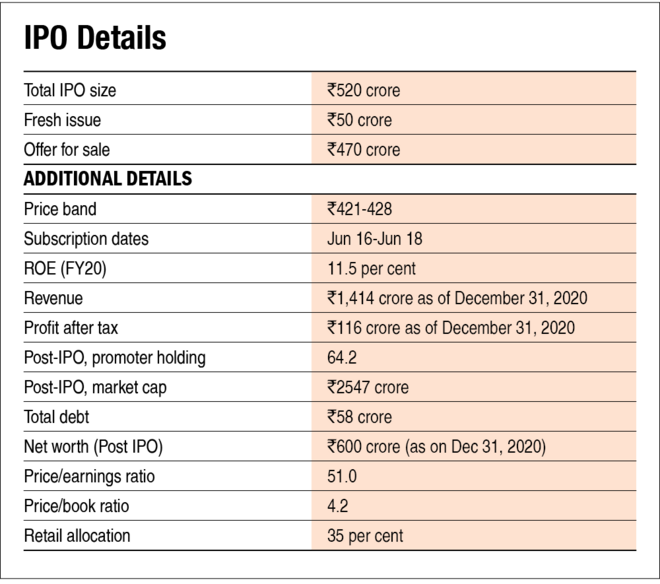

No, the current ROE and ROCE stood at 11.5 per cent and 17 per cent in FY20, respectively.

19. Was the company's operating cash flow-positive during the three years?

Yes, the company has reported positive cash flows in the last three years.

20. Did the company increase its revenue by 10 per cent CAGR in the last three years?

Yes, the company's revenue grew at a rate of 14.1 per cent compounded annually in the last three years from FY17 to FY20.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest coverage ratio more than 2?

Yes, the company is net-debt free.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

Yes, the company generates a majority of its revenues from distribution and marketing of milk, which has a very small shelf life. This helps the company to quickly convert its sales in cash which leads to a lower working capital cycle, which stood at 7.6 days.

23. Can the company run its business without relying on external funding in the next three years?

Yes, the company's capacity utilisation stood at around 60 per cent. Also, the company intends to use some of the proceeds from fresh issue towards repayment of debt, which will further strengthen its balance sheet and reduce finance costs in the future.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15%)?

Yes, the company reduced its short term borrowing from Rs 94 crore to zero as on December 31, 2020.

25. Is the company free from meaningful contingent liabilities?

Yes, the company reported contingent liabilities of over Rs 16 crore, which is around 2.7 per cent of its equity.

The Stock/Valuation

26. Does the stock offer operating earnings yield of more than 8 per cent on its enterprise value?

No, the company's stock offers an operating yield of 3.7 per cent as on FY20 numbers.

27. Is the stock's price to earnings less than its peers' median level?

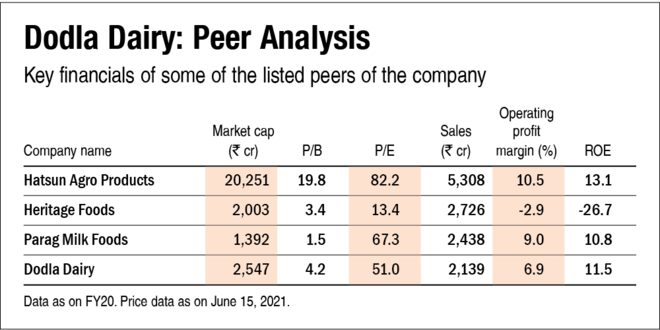

Yes.. Post IPO, the company's stock will trade at a P/E of around 51, which is less than its peers' median P/E of 67.

28. Is the stock's price to book value less than its peers' average level?

No. Post IPO, the company's stock will trade at a P/B of 4.2, which is more than its peers' median P/B of 3.4.

Disclaimer: The author may be an applicant in the IPO.

Ask Value Research ![]()