The automobile sector is a classic example of a cyclical industry. Both the passenger vehicle (PV) and commercial vehicle (CV) sub-segments are largely influenced by changes in economic growth. While the cyclicality of the PV segment is primarily driven by the discretionary nature of expenses (consumers can generally choose to use public transport systems, purchase used cars or use their existing vehicle), the variability of the CV segment is directly linked to the quantity of goods transported (which is a measure of economic activity). Besides, auto sales are very sensitive to changes in interest rates because of high unit costs and the resulting need for financing.

Historical perspective

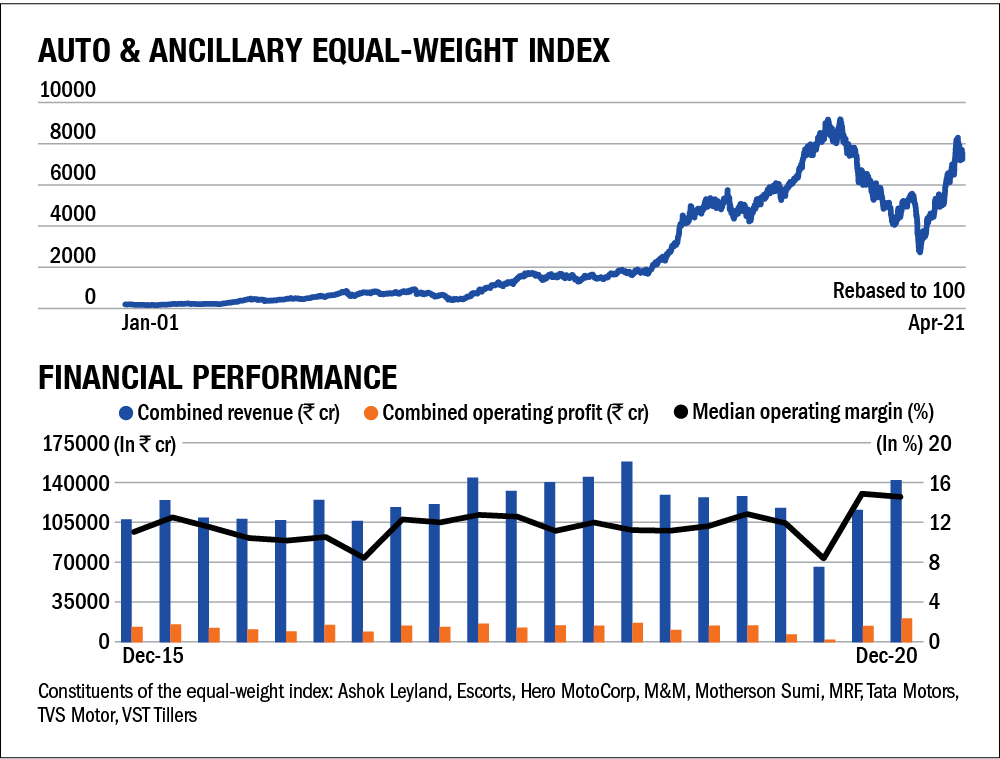

When compared to the Sensex, stocks belonging to the automobile industry are very volatile. The latest rally in the auto sector began in late 2013 and continued for close to five years. Thereafter, the industry started facing several headwinds, including the transition to BS-VI, the mandatory purchase of long-term insurance, liquidity crisis after the IL&FS episode and new axle-load norms. Adding to woes, the pandemic-led lockdown cast a dark shadow over the sector.

Outlook

Following the easing of the lockdown, sales rebounded on the back of pent-up demand, festive season and growing consumer preference for personal transport (due to heightened hygiene requirements). Besides, factors like better highways, the availability of cheaper fuel (natural gas) and high sales potential because of low per-capita vehicle ownership rates relative to developed countries are some positives.

Although the rise of electric vehicles (EV) could pose a significant threat to the industry, the EV segment is still at a very nascent stage and there are several challenges, such as low range compared to conventional vehicles, long charging duration and the lack of charging stations. Many leading players have already launched electric vehicles (EV), especially in the two-wheeler segment. However, it remains to be seen whether their adoption rate in India will mirror that of western countries.

Despite the 2nd wave of the pandemic depressing industry sales volumes, this phase is expected to be temporary. Overall, the industry outlook is a mixed bag. Although there is always a need to travel, the advent of technology has decreased the need to some extent. The growing use of video-conferencing facilities, greater adoption of e-commerce and the likelihood that WFH will stay relevant even after the lockdown are some possible long-term headwinds.

Methodology

Equal-weight index: Sectoral cycles are a long-term phenomenon and to observe them we require a long-term index. Since the available stock indices generally don't have such a history and homogeneity, we had to create our own index. To do so, we considered companies that had a 20-year history.

Within a sector, there could be multiple industries, so we tried to make the index as inclusive as possible. We then assigned all the components equal weights. This gave us our 'equal-weight' index.

Financial performance: In order to see whether the various sectors are on the road to recovery, we assessed the combined five-year revenues, profits and median margins of the companies constituting the equal-weight index. An upcycle often results in an uptick in these three. Do note that the idea here is not to assess the quantum of revenues or profits but to assess the trend.

Ask Value Research ![]()