Macrotech Developers Limited, which commenced its operations in 1995 with Mangal Lodha at the helm, is a large realty player focussed on constructing residential apartments in the Mumbai Metropolitan Region (MMR). The company, formerly known as Lodha Developers Limited (until 2019), primarily focuses on the affordable and mid-income housing segment, which accounted for nearly 55 per cent of its sales in FY21. Premium and luxury residences segment is also a crucial segment for the company, accounting for nearly 40 per cent of the sales. Development of commercial real estate, and logistics and industrial parks accounted for the rest.

The company currently has 36 ongoing projects covering around 29 million square feet (msf) of developable area and 18 planned projects spanning over 45 msf. The company also has a land bank of 3803 acre in MMR which can potentially develop 322 msf overall. This is the company's third attempt to come out with an IPO after two failed attempts in 2010 and 2018. During the financial year 2019-20, it reported a profit of roughly Rs 720 crore on sales of Rs 12,561 crore.

Strengths

Leading position in MMR region: The company has a strong presence in the MMR region which is considered to be the most attractive market in the country with the highest base selling price. The company stands amongst the top five developers in most micro-markets of the MMR region.

High entry barriers: The realty segment is capital intensive in nature. Additional factors unique to the MMR region such as limited land availability, high prices of land and the requirement of many approvals before developing a project result in high entry barriers for any new player in the industry.

Favourable regulatory climate: Promoting housing has always been a high priority for governments across the board and there are many incentives for home buyers. Maharashtra's reduction in stamp duty and construction premium, along with the additional incentives given in the Budget are recent examples.

Risks and weaknesses

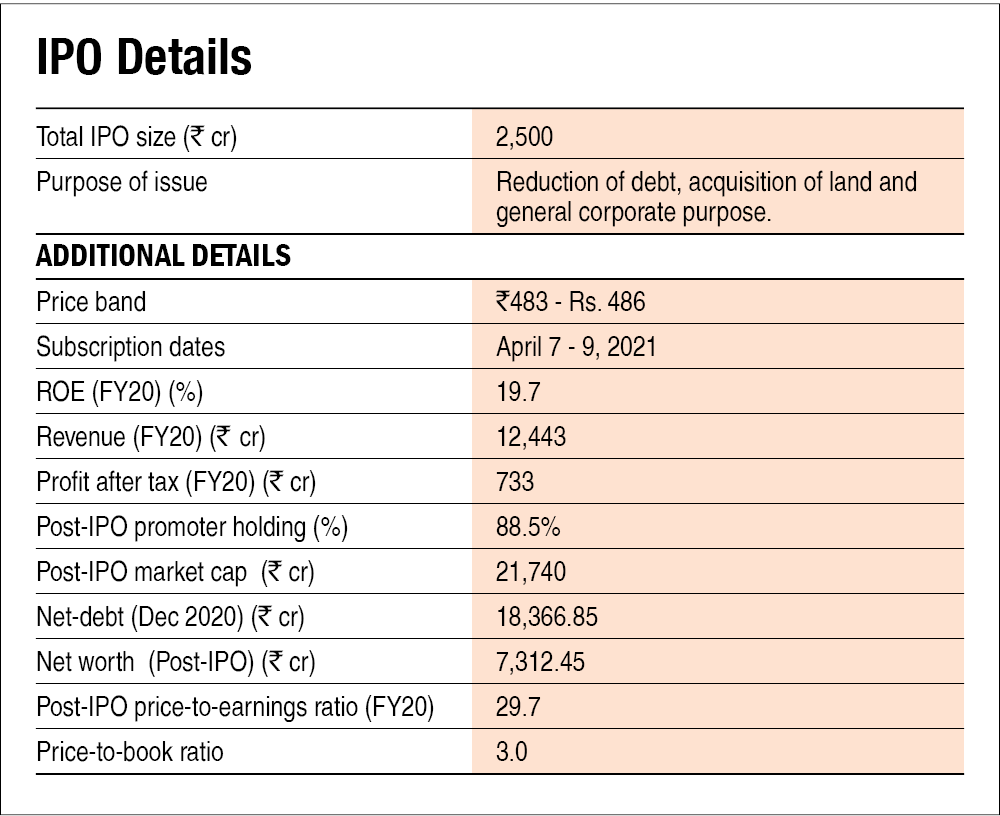

Weak balance sheet: The company is neck deep in debt. On a consolidated level, the company's total liabilities were at Rs 35,782 crore on an equity base of Rs 4,812 crore (7.4 times). Its net debt stood at Rs 18,367 crore as of December 31, 2020. A majority of the debt will be maturing in the coming twelve months and the company's credit rating had recently been downgraded.

Geographical concentration: Apart from a couple of projects in the United Kingdom and one in Pune, the company principally operates in the MMR region. Therefore, the company would be adversely affected in case of any weakness in this market.

Litigation: The company has disclosed that there are 12 criminal cases and 271 civil cases against it, involving an amount of Rs 7,752 crore. Any adverse orders can substantially affect the company.

Impact of COVID: Real estate companies were hit hard during the pandemic and this has reflected in the company's financial results. The company incurred a loss of Rs 264 crore in the first nine months of FY21. It remains to be seen how quickly the company can bounce back.

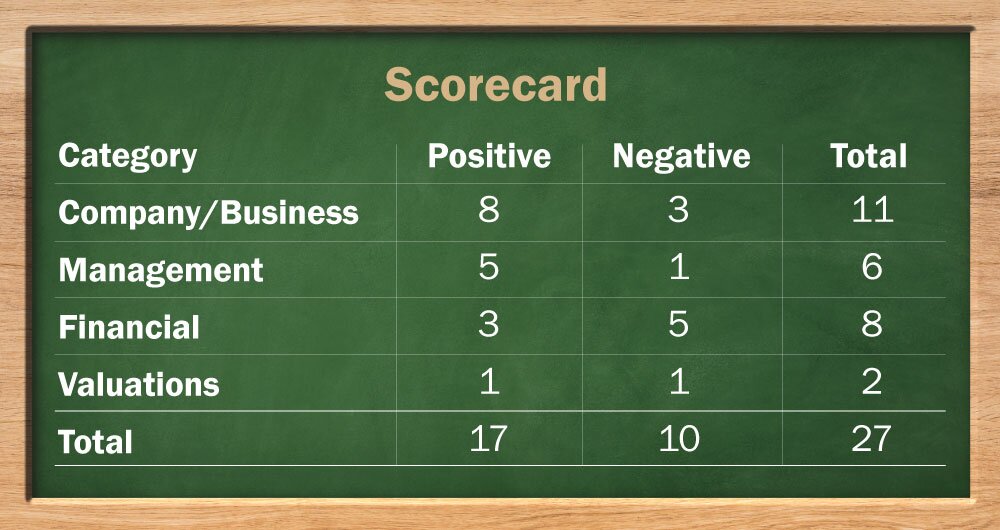

IPO Questions

Company/Business

1. Are the company's earnings before tax more than Rs 50 crore in the last twelve months?

No. In the trailing twelve months as of December 2020, the company incurred a loss of Rs 466 crore.

2. Will the company be able to scale up its business?

Yes, the company is primarily present in only one city as of today which means it could theoretically expand to other cities. However, it is not an easy task and involves a significant amount of execution risk.

3. Does the company have recognisable brand/s, truly valued by its customers?

Yes, the company's "LODHA" brand is well recognised in the Mumbai Metropolitan region (MMR).

4. Does the company have high repeat customer usage?

No. But that is more attributable to the nature of the industry and not to the company.

5. Does the company have a credible moat?

Yes. The real estate business is capital intensive and requires deep knowledge of the local environment. Also, the limited availability of land makes it difficult for new entrants to compete.

6. Is the company sufficiently robust to major regulatory or geopolitical risks?

Yes. The company has successfully navigated regulatory hurdles so far and therefore, we have no reason to believe otherwise.

7. Is the business of the company immune from easy replication by new players?

Yes. Replicating a large construction business is not an easy task and is therefore, not easily replicable.

8. Is the company's product able to withstand being easily substituted or outdated?

Yes. A house is a very basic necessity which cannot be substituted or outdated.

9. Are the customers of the company devoid of significant bargaining power?

Yes. There are only a handful of quality developers in the Mumbai Metropolitan region and due to the B2C nature of the business, customers do not have significant bargaining power.

10. Are the suppliers of the company devoid of significant bargaining power?

Yes. The company has multiple suppliers and therefore, does not have to worry about the suppliers' bargaining power.

11. Is the level of competition the company faces relatively low?

No. There are many players and the industry is highly fragmented and competitive.

Management

12. Do any of the founders of the company still hold at least a 5 per cent stake in the company? Or do promoters totally hold more than 25 per cent stake in the company?

Yes. The promoters will hold approximately 88 per cent stake in the company after the IPO.

13. Do the top three managers have more than 15 years of combined leadership experience at the company?

Yes. The managing director and the whole-time director have more than 15 years of combined experience.

14. Is the management trustworthy? Is it transparent in its disclosures, which are consistent with the SEBI guidelines?

Yes, we have no reason to believe otherwise.

15. Is the company free of litigation in court or with the regulator that casts doubts on the intention of the management?

No. There are a lot of cases pending against the company.

16. Is the company's accounting policy stable?

Yes, we have no reason to believe otherwise.

17. Is the company free of promoter-pledging of its shares?

Yes. The promoters have not pledged their shares.

Financials

18. Did the company generate current and five-year average return on equity of more than 15 per cent and return on capital employed of more than 18 per cent?

No. Since the company has made losses in the current financial year, its current return on equity is negative. However, its five-year average return on equity and return on capital employed turn out as 22.7 per cent and 9.4 per cent respectively.

19. Was the company's operating cash flow positive during the previous year and at least four out of the last five years?

Yes. The company's cash flow from operations was always positive except in FY19.

20. Did the company increase its revenue by 10 per cent CAGR in the last three years?

No. The company's revenue has declined from Rs 13,726 crore in FY18 to Rs 12,560 crore in FY20. Its revenue for the first nine months of FY21 stood at Rs 3,160 crore.

21. Is the company's net debt-to-equity ratio less than 1 or is its interest-coverage ratio more than 2?

Yes. Though the company's net debt-to-equity ratio was more than 3 times, its interest coverage ratio for FY20 was 2.36.

22. Is the company free from reliance on huge working capital for day-to-day affairs?

No. Real estate companies, by the nature of their business, are reliant on huge amounts of working capital. However, a significant portion of their working capital needs is funded by pre-sales.

23. Can the company run its business without relying on external funding in the next three years?

No. Due to the sharp fall in sales this year and the leveraged state of the balance sheet, it seems likely that the company will need external funding in the next three years.

24. Have the company's short-term borrowings remained stable or declined (not increased by greater than 15 per cent)?

Yes. The company's current borrowings have decreased from Rs 20,107 crore in FY18 to Rs 16,145 crore as of December 31, 2020.

25. Is the company free from meaningful contingent liabilities?

No. As per the company's management, it has contingent liabilities worth Rs 1600 crore approximately.

Stock/Valuation

26. Does the stock offer an operating-earnings yield of more than 8 per cent on its enterprise value?

Yes. The yield as of March 2020 was 9.5 per cent.

27. Is the stock's price-to-earnings less than its peers' median level?

Not applicable. The company has made losses during the last twelve months.

28. Is the stock's price-to-book value less than its peers' average level?

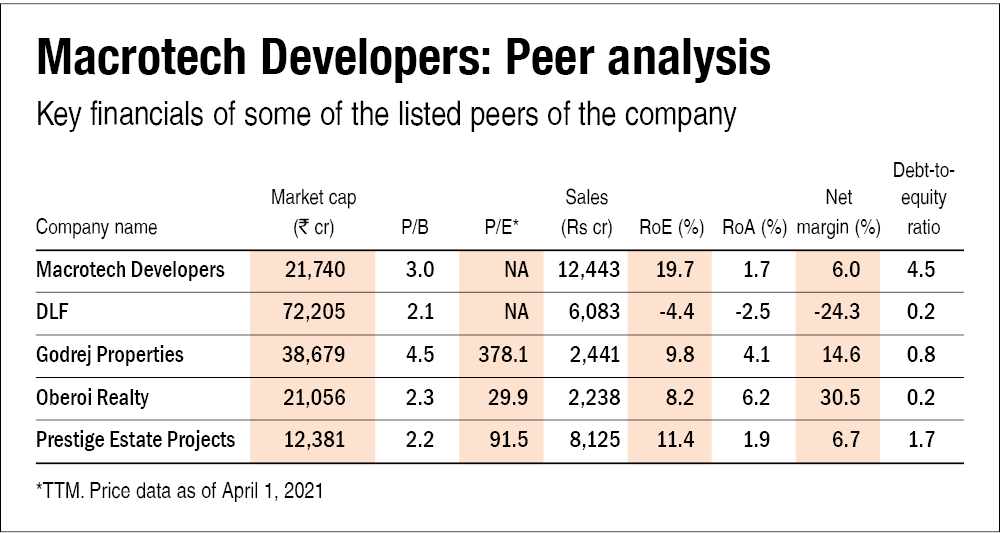

No. The company's P/B of 3.0 is more than the competitors' average of 2.8.

Ask Value Research ![]()